We’ve seen a strong performance from the Gold Miners Index (GDX) since the beginning of Q1, with the ETF up more than 22% in Q2, easily outperforming the S&P-500 (SPY). This change in character is quite positive for the index as it’s now finally gaining ground on the S&P-500, and the best performance for the GDX comes when it’s not only trending higher above its 200-day moving average but when it’s also outperforming the S&P-500. Some investors might think that they’ve missed the move with the GDX up 25% off its lows, but while some names are fairly priced, several others are still trading at very reasonable valuations. Let’s take a look at a few names below:

(Source: TC2000.com)

Click here to check out our Gold and Silver Industry Report for 2021

Gold Fields (GFI), New Gold (NGD), and Newmont Corporation (NEM) all have very different production profiles and cost profiles within the GDX. NGD is a mid-tier producer in Canada, GFI is a senior producer with most of its production from Africa & Australia, and NEM is the largest gold producer globally.

While all three have solid stories and different catalysts for upside, they’re all still very reasonably priced, with GFI and NGD trading at less than 10x FY2022 annual EPS estimates and NEM trading at barely 18x FY2022 annual EPS forecasts. For companies set to increase annual EPS by double and triple-digit growth rates between FY2020 and FY2022, these are compelling valuations. We’ll investigate the investment case for NGD below first:

New Gold just came off a soft quarter in Q1, with the production of just ~96,000 gold-equivalent ounces, a 7% decrease from the year-ago period. However, the lower production was partially due to a mudslide in Q1, which affected operations at its New Afton Mine. The good news was that the company’s copper production, which was previously a drag on performance with low copper prices and rising gold prices, is now a major tailwind. During Q1, NGD’s average realized copper price came in at $3.83/pound, up from $2.56/pound in the year-ago period.

Assuming copper prices retain their strength, we could see an average realized copper price above $4.00/lb in FY2021 which would be a nice boost to NGD’s revenue. Given that there are very few gold producers with a significant copper component out there, NGD offers both diversification and exposure to a metal that could see a major supply crunch with the trend towards electrification.

(Source: YCharts.com, Author’s Chart)

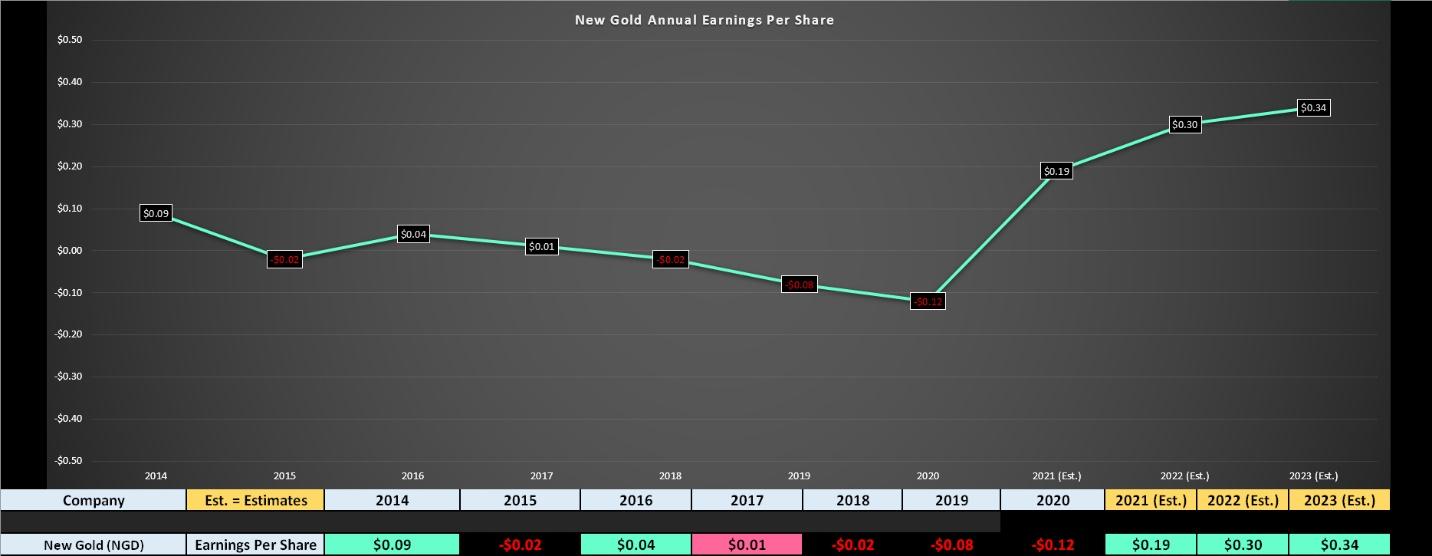

If we look at NGD’s earnings trend, we can see that the company is expected to generate $0.19 in annual EPS in FY2021, translating to an earnings breakout year for the stock. If we look ahead to FY2022, annual EPS is projected to increase by more than 50% to $0.30, a very bullish development following the expected earnings breakout this year.

Even if we assume what I believe to be a very conservative earnings multiple of 11 for New Gold, given that it’s a higher cost producer, this translates to a fair value for the stock of $3.30. Compared to the current share price of $2.20, this means there’s more than 40% upside in the stock, even after the recent rally. Therefore, any dips should provide low-risk buying opportunities.

Moving over to Gold Fields, the company also had a slow start to FY2021 with lower production sequentially at the company’s massive South Deep Mine and its St. Ives Mine in Australia. Despite the slow start to the year, GFI remains on track to meet its guidance of ~2.32 million gold-equivalent ounces [GEOs] in FY2021, with ~541,000 GEOs produced in its first quarter.

While some investors might not be that impressed with GFI given that it has significant exposure to Africa and it’s a high-cost producer, there is a major catalyst on the horizon that should boost the stock’s attractiveness beginning in FY2023.

This catalyst is the construction of the company’s Salares Norte Project in Chile, which is expected to increase production by more than 20% at significantly lower costs. Based on the forecasted mine plan, Salares Norte will produce more than ~500,000 gold-equivalent ounces per year at all-in sustaining costs below $600/oz.

This compares quite favorably to GFI’s current cost profile of $1,050/oz, making Salares Norte a rare project that will not only boost production but be very accretive for margins. This should translate to a massive boost in annual EPS estimates starting in FY2023, with annual EPS expected to come in at above $1.40.

(Source: YCharts.com, Author’s Chart)

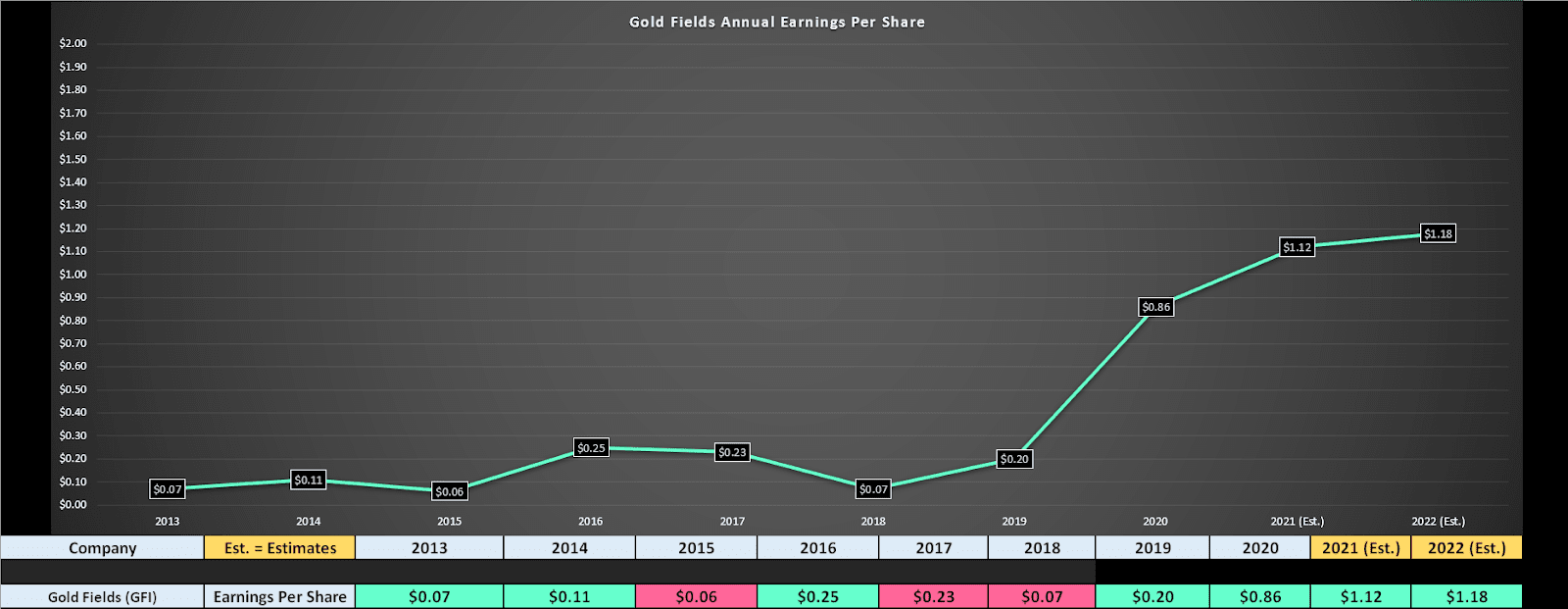

If we look at GFI’s earnings trend above, we can see that FY2020 annual EPS increased by more than 300% year-over-year to $0.86 and is expected to jump another 30% in FY2021 to $1.12. These are incredible growth rates, yet GFI trades at just over 10x FY2021 annual EPS estimates and barely 10x FY2022 annual EPS estimates.

The pessimism might be related to GFI having a higher-cost year ahead and having more African (Tier-3 jurisdiction) exposure than its peers. However, even if we use an ultra-conservative earnings multiple of 14 given GFI’s organic growth, this translates to a fair value of $16.52 for FY2022 and $19.60 in FY2023 while Salares Norte ramps up. Given this significant upside, I would expect any dips below $11.00 to provide low-risk buying opportunities. Entries below $11.00 would represent 45% upside to fair value ($16.52), placing the stock on a Strong Buy rating if it does pull back.

(Source: YCharts.com, Author’s Chart)

The final name on the list needs no introduction and is the largest gold producer globally. NEM also had a softer start to FY2021, with COVID-19 related headwinds weighing on some operations. However, NEM has maintained guidance, is paying one of the most competitive yields in the sector at $2.20 per share, and is set to see higher margins beginning next year.

This should translate NEM from a ~7.5 million GEO per year producer at costs of $950/oz in FY2021 to a ~7.7 million GEO per year producer at costs below $900/oz. This should provide a massive boost to the company’s free cash flow and annual EPS, and the higher gold price we’re seeing could lead to higher dividends going forward.

Based on NEM’s dividend framework of a dividend between $2.20 to $2.80 at a six-month average gold price of $1,800/oz, we could see the dividend raised this year to $2.55 if the gold price stays above $1,900/oz and we see fewer COVID-19 related headwinds. While NEM did have a $1,800/oz average gold price in Q4, which triggered a dividend increase, the company elected to stay at the low end of the $2.20 - $2.80 range ($2.20) because of COVID-19.

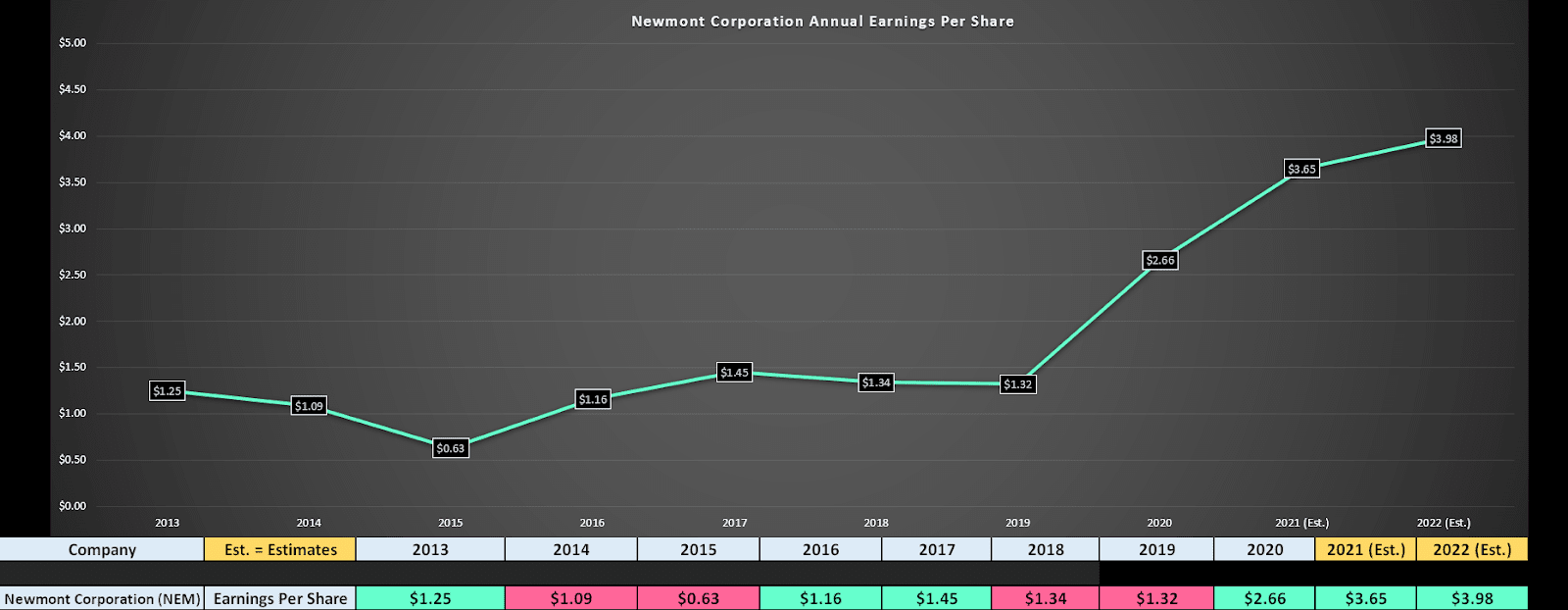

Assuming the company moves to the middle of this range, the dividend would increase to $2.55 per share, translating to a 3.5% yield at current levels. This makes NEM an excellent combination of growth and value, with annual EPS set to grow by 50% between FY2020 and FY2022 ($3.98 vs. $2.66). Most importantly, NEM trades at just 18x earnings despite this solid growth rate and has just broken out of a massive 30-year base. The price target for this breakout is over $100.00 per share, suggesting solid upside ahead. Given the strong technical picture and improving cost profile, I would view any dips below $60.00 on NEM as low-risk buying opportunities.

(Source: TC2000.com)

Many investors might assume that the gold producers are expensive after doubling from 2019 levels. However, the GDX continues to be one of the cheapest sectors out there, with most producers trading below 15x FY2021 earnings and the average million-ounce producer paying a dividend yield of 2.30%.

This is a much better value proposition than the general market, with a P/E ratio above 30 and a dividend yield below 1.40%, suggesting that the GDX is the best spot to go bottom-fishing, not the S&P-500. While it’s possible we could see a pullback over the coming weeks, I would view this as a buying opportunity, and I see NEM, NGD, and GFI as three of the better ways to play the sector. For now, I remain long NGD and NEM, and I may look to buy GFI on weakness.

Disclosure: I am long GLD, NEM, NGD

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

Disclosure: I am long GLD, NEM, NGD

NEM shares were trading at $72.72 per share on Wednesday afternoon, down $1.23 (-1.66%). Year-to-date, NEM has gained 22.61%, versus a 12.76% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 3 Gold Miners To Buy On Dips appeared first on StockNews.com