Two Tech Stocks To Buy On Dips

It’s been an impressive start to the year thus far for the Nasdaq-100 Index (QQQ), with the ETF up more than 28% year-to-date, lapping an incredible 47% return in 2020. This has left many tech stocks trading at exorbitant valuations, with more than fifty names trading above 35x sales.

However, some names are still trading at very reasonable valuations, and some that have been out of favor over the past couple of months are now heading towards buy-zones. With an increased probability of a correction over the next couple of months, this is the perfect time to build a shopping list to prepare ahead of time.

In this update, we’ll look at names that look like solid buy-the-dip candidates and their ideal buy zones.

(Source: TC2000.com)

Olo Inc (OLO) and Avalara (AVLR) have little in common, except the fact that both companies have gone public in the past four years, and both are leaders in their respective industries. In Olo’s case, which stands for online ordering, the company develops digital ordering and delivery programs through their SaaS platform for restaurants.

At a time when the industry has struggled due to the pandemic, Olo has given its partners a competitive advantage, raising average tickets for Five Guys Burgers & Fries and helping Wingstop (WING) to grow its digital footprint rapidly.

Moving to Avalara (AVLR), the company is the leader for automated tax compliance, and its AvaTax helps business owners to calculate rates across multiple jurisdictions, as well as product-specific tax rates, to allow businesses to stay in compliance with up-to-date data. Let’s take a closer look at both companies below:

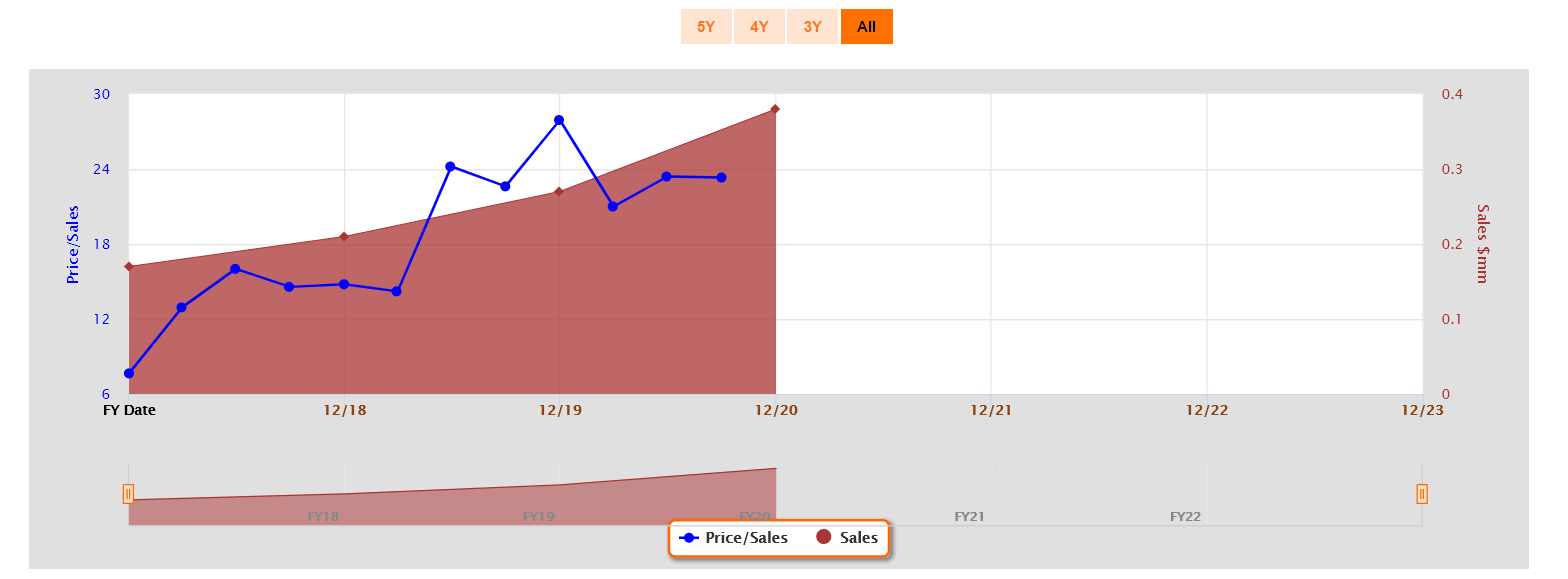

Beginning with Avalara, the company has seen tremendous growth, increasing its sales from $70MM in Q3 2018 to $181.2MM in the most recent quarter.

This represents an incredible 37% compound annual revenue growth rate, and it was another record quarter for revenue. The strong results were driven by 38% growth in Subscription & Returns revenue, and 95% growth in Professional services.

The company added another 800 customers in the quarter, ending the quarter with 17,400 core customers, up 22% year-over-year.

(Source: YCharts.com, Author’s Chart)

As the chart above shows, Avalara is not expected to generate positive annual earnings per share [EPS] in 2021, but it will be in the near future, with FY2023 annual EPS estimates sitting at $0.12 and FY2024 annual EPS estimates sitting at $1.46.

This would represent an 87% compound annual EPS growth rate relative to FY2020. Unfortunately, while AVLRA had a decent Q3 performance, its Q4 guidance was a little lighter than the market hoped for, guiding for just $184MM in revenue, representing its lowest sequential growth rate in years.

Over the past three years, AVLR has been growing revenue by more than 5% sequentially, and Q4’s guidance would represent a ~2% increase. Having said that, with AVLR now nearly 20% off its highs, the valuation is beginning to improve.

(Source: FASTGraphs.com)

As shown in the chart above, AVLR is now trading at closer to 19x price to sales, which is a very reasonable valuation for a high-growth software name that’s a leader in its space.

Looking ahead to FY2023 revenue estimates, AVLR is trading at an even more reasonable 12x sales, with estimates sitting at $1.07BB and AVLR trading at a market cap of ~$12.9BB.

Given the company’s tendency to under-promise and over-deliver on guidance, the $1.07BB in estimates looks conservative, especially with recent acquisitions that should help the company continue to gain market share.

If we look at the technical picture, AVLR’s correction has left the stock just 12% above a major support zone, with support coming in between $122.00 and $130.00. This is based on a horizontal support area where the stock saw significant accumulation and a multi-year uptrend line which comes in near $130.00. So, if this correction continues, a very low-risk buying opportunity could arise into what’s expected to be a softer Q4 earnings report. In summary, I believe AVLR is a name to keep a very close eye on heading into the holiday season, and I would view pullbacks below $126.00 as low-risk buying opportunities. At these levels, AVLR would trade at a market cap of just $11BB and just over 10x FY2023 revenue estimates.

(Source: TC2000.com)

The next name on the list, Olo Inc., is a newer name, and this presents an opportunity. This is because the best performers are typically those that have gone public in the past ten years, given that they have much higher growth rates than their more mature peers. In Olo’s case, the company has been growing rapidly and reported $37.4MM in revenue in its most recent quarter, translating to 36% growth year-over-year. As noted earlier, the company helps restaurants to improve their digital footprint with its fully customizable technology stack.

The platform also assists restaurants when it comes to dealing with industry-wide labor challenges, with the Olo Switchboard module and the Olo Expo module. Switchboard helps restaurant brands manage phone ordering, while Expo is a tablet-based software to enhance front-of-house workflow. Obviously, Olo cannot cure the biggest problem for restaurants, commodity cost inflation, but higher productivity through the use of technology and a larger digital loyalty footprint are doing wonders for Olo partners, helping with sales leverage.

(Source: YCharts.com, Author’s Chart)

If we look at Olo’s projected growth, we can see that the company is set to grow annual revenue by more than 50% year-over-year, with FY2021 revenue estimates of $149.5MM. If we look ahead to FY2022, revenue is expected to grow another 30% to $194.6MM before hitting the quarter-billion mark in FY2023, based on estimates. This is exceptional growth, translating to a 39% compound annual EPS growth rate vs. FY2020 levels. Understandably, some investors are unwilling to pay more than 16x FY2023 revenue estimates, with OLO trading at a market cap of $4.2BB.

I would argue that this is a steep valuation, even if this growth comes to fruition. Having said that, if the stock’s decline continues and it dips below 15x FY2023 sales, I believe this would represent a low-risk buying opportunity. This is because the FY2023 forecasts look conservative, and OLO is a truly transformative solution for the industry at a time when the industry desperately needs help with technology to drive productivity gains and boost sales, especially for those brands that are losing market share. In summary, OLO is worth keeping at the top of one’s watchlist.

(Source: TC2000.com)

If we look at OLO’s chart, we can see that the stock has strong support near $25.70, where we have seen accumulation in two prior instances over the past nine months. Assuming OLO were to dip below $24.20 and break down from this support zone, it would likely shake out some investors. This would create a low-risk buy point, given that we’d likely have technical selling, and the stock would hit oversold levels. Obviously, there’s no guarantee that the stock dips another 13% to the $24.20 level, but this would present a low-risk area to start a position in this exciting new growth story.

With the market continuing to remain overbought, chasing stocks here makes little sense, and especially not high-growth names extended from their recent bases. However, if we do see a correction in the general market, or the correction in AVLR and OLO continues, this could set up low-risk buying opportunities for these two names, hence why I think they’re worth keeping at the top of one’s watchlist. In summary, I would be watching the $126.00 level on AVLR and $24.20 level on OLO for low-risk buying opportunities, given that both stocks would trade at very reasonable valuations and hit oversold levels if they find themselves at these levels before year-end

Disclosure: I have no positions in any stocks mentioned

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

AVLR shares were unchanged in after-hours trading Thursday. Year-to-date, AVLR has declined -8.62%, versus a 26.87% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 2 Growth Stocks to Buy on the Dip appeared first on StockNews.com