The case of Oracle (ORCL) has been a curious one. After making itself suddenly relevant in the AI race by becoming part of the $500 billion “Stargate Project,” and after inking a blockbuster $300 billion deal with OpenAI, Oracle was in the cloud infrastructure big leagues with the likes of Amazon (AMZN), Microsoft (MSFT), and Alphabet (GOOGL).

However, although this helped propel Oracle Chief Technology Officer Larry Ellison to become the richest person in the world for a brief moment, it all came crashing down after reports emerged about whether the company had the wherewithal to fund this infrastructure buildout. Credit default spreads on Oracle's swaps reached levels not seen since the global financial crisis as market participants grew wary of its burgeoning debt levels.

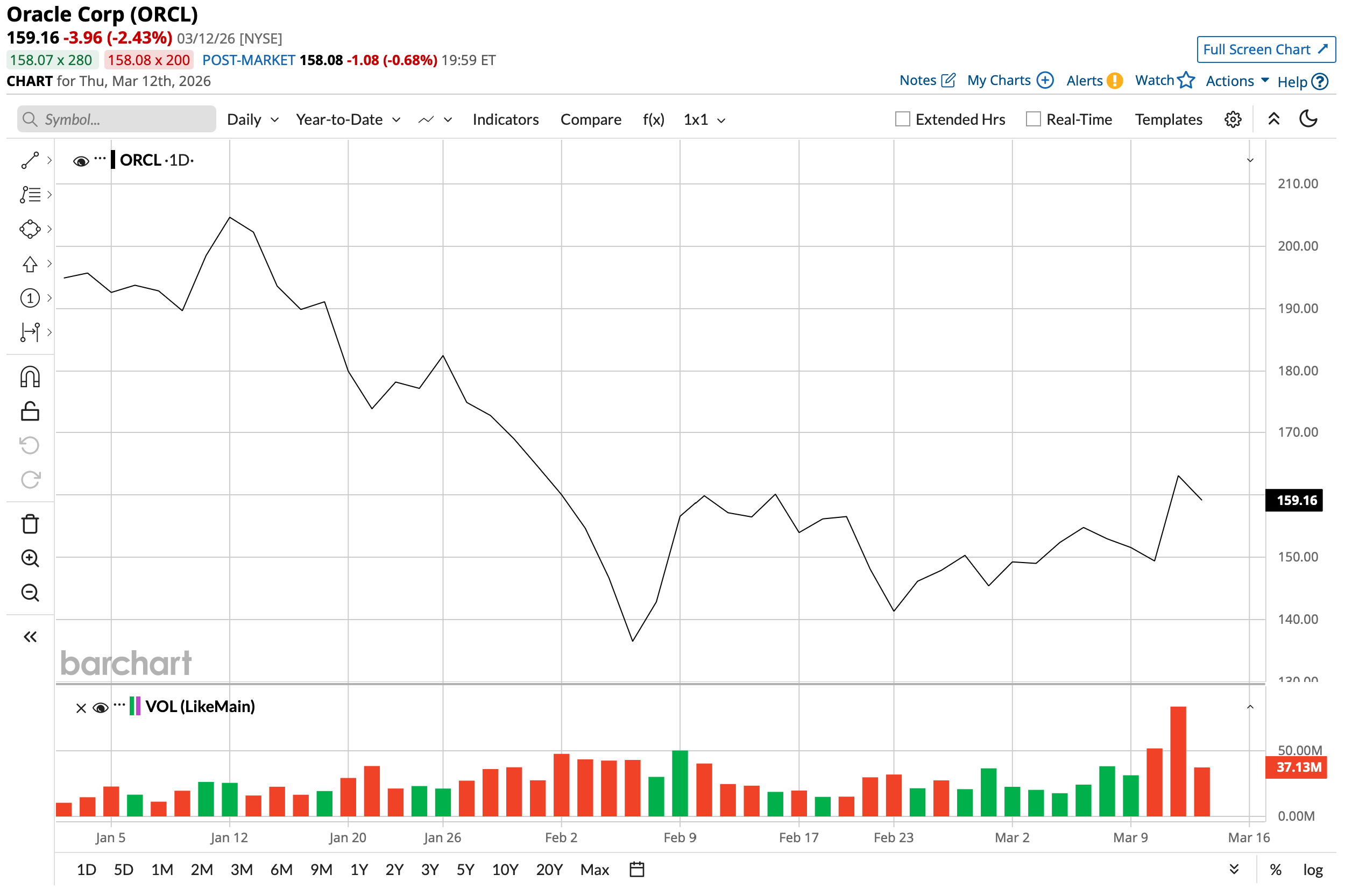

Still, Oracle doesn't seem to care. In a recent filing with the U.S. Securities and Exchange Commission (SEC), the enterprise software giant revealed that it will now spend $2.1 billion on restructuring costs in fiscal 2026, up from $1.6 billion announced in December 2025. Shares did not respond kindly to the news, though, falling by more than 2% on March 12.

About Oracle

Founded in 1977 as a database company, Oracle has gone on to become one of the largest enterprise software and cloud infrastructure companies in the world. Its latest value driver, Oracle Cloud Infrastructure (OCI), provides computing, storage, networking, and AI infrastructure services, while its enterprise segment sells business software for ERP, HR systems, supply-chain management, and customer relationship management.

Valued at a market capitalization of $446 billion, ORCL stock is down 20% on a year-to-date (YTD) basis. Notably, the stock also offers a dividend yield of 1.29%, which is higher than the sector median. Further, Orcale has been raising dividends consecutively over the past 12 years.

With that all said, amid all the noise, let's try to make sense of whether Oracle stock is a buy or not.

Oracle Has Outstanding Financials Despite the Debt

Oracle's track record of growth over the past decade has been patchy. Over the past 10 years, revenue and earnings have grown at compound annual growth rates (CAGRs) of just 5.6% and 6.25%, respectively. Notwithstanding that, while looking at Oracle, analysts remain convinced that it will report above-average growth in the coming periods, with forward revenue and earnings growth pegged at 18% and 20% — higher than sector medians of roughly 10% and 15%, respectively.

Moreover, the company's latest third-quarter results pleasantly surprised the Street, leading to a 9% rise in ORCL stock. Oracle reported beats on both revenue and earnings.

Revenue for fiscal Q3 rose 22% year-over-year (YOY) to $17.2 billion. Cloud, now the biggest revenue segment for the company, accelerated 44% YOY to $8.9 billion as the company's AI infrastructure mandate gains pace.

Earnings grew 21% in the same period, coming in at $1.79 per share. This was higher than the consensus EPS estimate of $1.70, marking another quarterly earnings beat from the company.

Remaining performance obligations, a barometer of demand, witnessed another quarter of ballistic growth. At $553 billion, the metric grew 325% YOY. Oracle attributed the growth to “large scale AI contracts.”

Net cash from operations for the nine months ended Feb. 28 was $17.4 billion, up from $14.7 billion in the year-ago period. The company closed the quarter with a cash balance of $38.5 billion, well ahead of its short-term debt levels of $9.9 billion. However, long-term debt levels remained at a substantial $124.7 billion.

Meanwhile, in terms of valuation, the recent share price decline has helped bring ORCL stock down to more reasonable levels. A forward price-to-earnings (P/E) ratio of 25.8 times is somewhat comparable to the sector median of 21.7 times. Meanwhile, the forward price-to-cash flow ratio of 23.1 times and the forward price-to-sales (P/S) ratio of 7.7 times are higher than the respective sector medians.

Should You Give Oracle a Chance?

Oracle's large debt pile doesn't help things. Moreover, the whole circus around David Ellison's now apparently successful bid for Warner Bros. (WBD) also exacerbated matters for the software giant after Larry Ellison guaranteed $40 billion to help sail Paramount Skydance's (PSKY) offer.

Instead, Oracle should direct its focus toward what it's doing right and get back on track to successfully deliver on its AI mandate while also looking to reduce its dependence on OpenAI, just like it did by diversifying from Nvidia (NVDA) with AMD (AMD).

A notable step in the right direction was Oracle's introduction of the Bring Your Own Cloud (BYOC) model. Under this approach, enterprise customers either provide their own GPU clusters or commit capital upfront to fund Oracle's procurement of the necessary hardware. This structure keeps the heavy capital burden off Oracle's balance sheet while still enabling the company to deliver the required compute capacity.

The shift is also expected to enhance operating leverage. Notably, Oracle has accelerated rack deployment timelines by expanding to three times the previous number of manufacturing sites and quadrupling rack output over the past year. Consequently, faster time from hardware delivery to revenue generation should improve returns on invested capital as utilization ramps.

Finally, Oracle's longstanding presence in enterprise software, combined with its growing cloud capabilities, creates a differentiated position. The company's multi-cloud infrastructure, built around OCI and integrated with its AI Data Platform, Fusion ERP, and industry-specific suites, gives it a meaningful advantage over more application-centric competitors.

This integrated ecosystem allows Oracle to rapidly deploy AI tools and agentic capabilities for customers, streamline implementation, and perhaps critically keep clients anchored to the platform for the long term.

Considering this, Oracle just needs to put its head down, look for efficiencies of scale, and continue to deliver in order to dispel fears in the market about its debt levels and huge capital expenditure.

What Do Analysts Think of ORCL Stock?

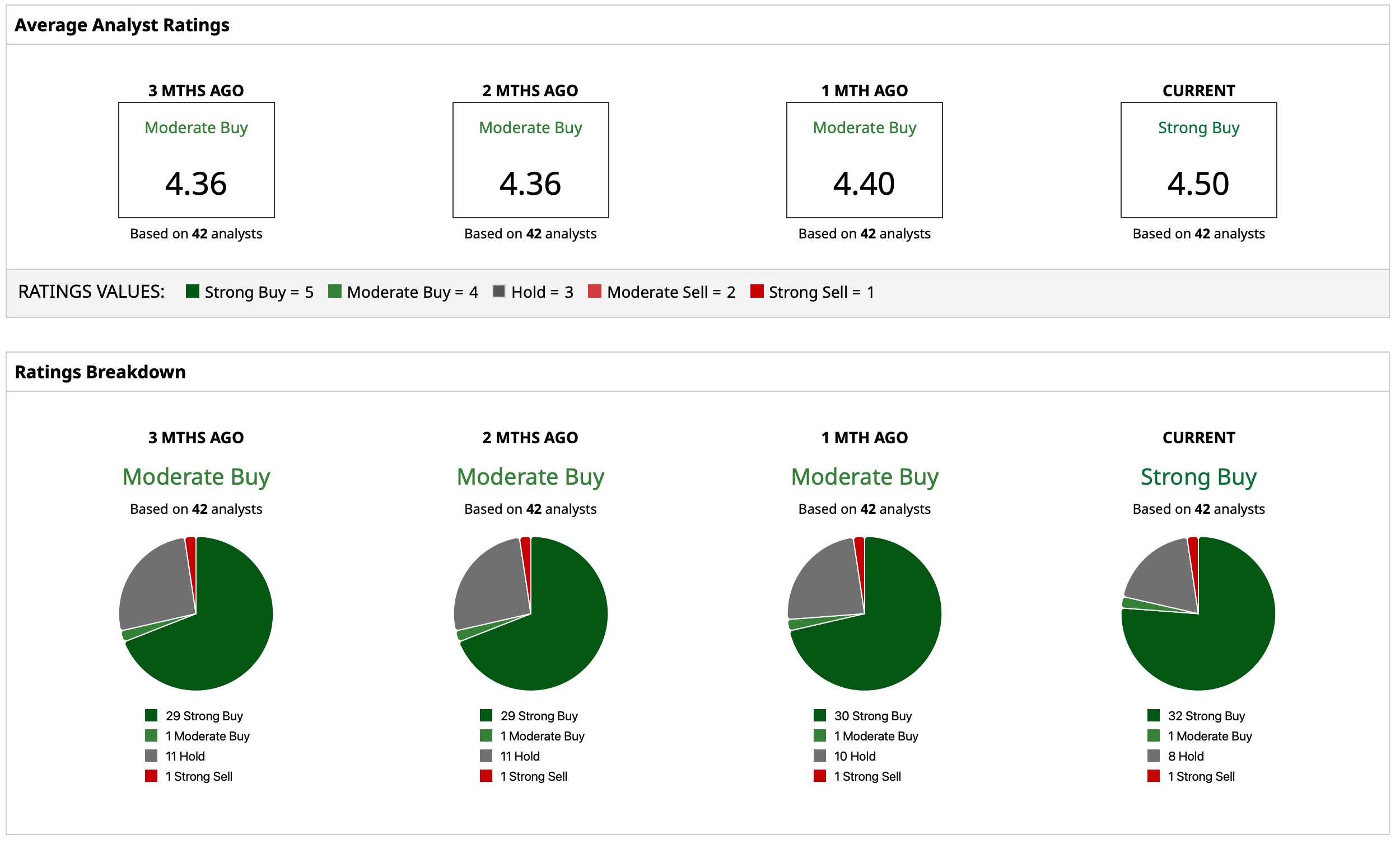

Analysts give ORCL stock a “Strong Buy” consensus rating. The mean target price of $264.44 indicates potential upside of about 70% from current levels. Out of 42 analysts covering the stock, 32 have a “Strong Buy” rating, one has a “Moderate Buy,” eight analysts have a “Hold” rating, and one has a “Strong Sell.”

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart