Feeder cattle prices (GFK26) have climbed about 6% over the past month, and front-month live cattle (LEM26) are up roughly 8% in early 2026. These moves are already feeding into packers’ margins and retail prices, raising the stakes for anything that threatens throughput. That is exactly what a weeks-long giant meatpacking strike at a key JBS (JBS) beef plant has done.

The strike has turned a single facility dispute into a focal point for the broader beef supply story even as the company has worked to shift production elsewhere. The walkout is creating headlines and pressure on the ground, but it is also highlighting how much pricing power, scale, and flexibility matter when the system is stressed.

Bank of America is leaning into this news rather than backing away. Sticking with a bullish stance, the firm expects JBS stock’s post-earnings rally in 2026 to continue as tighter cattle supplies support beef margins.

Can JBS’ momentum really outlast the strike disrupting its U.S. operations? Or does BofA's optimism run ahead of reality? Let’s take a closer look.

JBS' Financial Momentum

Operating in Brazil, JBS is a global meat processor that produces beef, pork, poultry, and value-added food products for customers worldwide. The company carries a market capitalization of around $13.8 billion.

JBS stock sits near the $18 level as of this writing, up 26% year-to-date (YTD) and 23% over the last six months. JBS was first approved for trading on the New York Stock Exchange (NYSE) in May 2025.

The forward price-to-earnings (P/E) multiple stands at 9.8 times versus a sector median of 14.8 times. Meawhile, the P/E-to-growth (PEG) ratio of 0.99 times screens well below the group’s multiple of 2.1 times, reinforcing a discounted entry point.

The most recently reported quarter for the period ending in December 2025 delivered EPS of $0.39, which fell short of the $0.42 consensus estimate. That result translated into a -7% surprise that briefly tested sentiment around JBS stock.

This miss came even as the company generated sales of $23.06 billion for December 2025, representing 2% year-over-year (YOY) growth. Meanwhile, net income of $415.1 million declined more than 28% YOY as higher costs and pricing pressures filtered through the income statement.

Notably, operating cash flow for December 2025 surged to $2.93 billion, a jump of 6,894%, highlighting strong cash conversion even in a softer earnings quarter. The net cash flow position remained negative at -$1.05 billion but improved by 66%, signaling ongoing balance sheet repair.

A Strategic Advantage in the Greeley Disruption

JBS has made it clear that the Greeley beef plant strike has not brought its operations to a standstill. The company says the facility is running at limited capacity, and that beef production has been shifted to other plants to keep customers supplied, which helps explain why the bull case remains intact even as talks with workers drag on. This operational flexibility matters because the industry has been weighed down by excess slaughter capacity, which has kept profit margins tight for years.

Now the dynamic is changing. The Greeley strike, combined with other capacity reductions, is tightening supply and allowing packers to capture better margins. Thousands of workers are still on the picket lines at one of the largest meatpacking plants in the country, yet the shifting capacity is actually supporting profitability rather than breaking the bull thesis.

Analyst Confidence for JBS

JBS’ next checkpoint is scheduled for May, with the current quarter carrying an average earnings estimate of $0.32 per share, even though there is no prior-year figure available for a clean YOY comparison.

In October 2025, BMO Capital published a call on JBS stock, with analyst Andrew Strelzik reiterating a “Buy” rating and setting a price target of $17. That target has already been met and slightly exceeded.

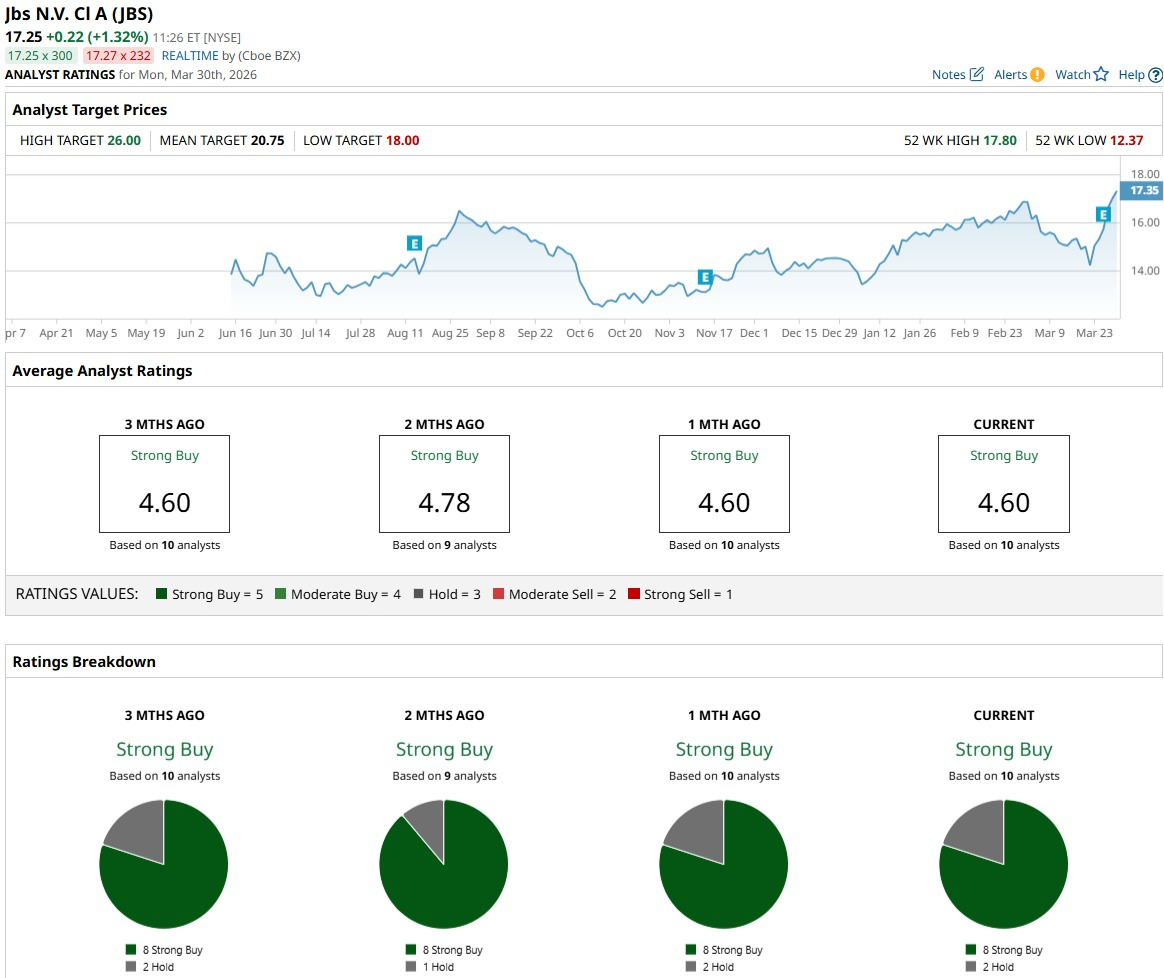

There is a strong bullish skew among analysts, as a group of 10 covering analysts have a Strong Buy" consensus rating for JBS stock. The average price target clocks in at $20.85, implying potential upside of roughly 15% from current levels. This gap between where shares trade today and where analysts think they can go next aligns neatly with Bank of America’s view that the post‑earnings rally still has room to run.

The Bottom Line

The strike is reshaping the narrative around JBS stock, but it is not breaking the investment case that Bank of America continues to back. That conviction rests on a mix of discounted valuation, solid cash generation, and a healthier beef margin setup that still gives the stock room to work, especially as efficiencies scale. This is exactly why Bank of America’s call for the post‑earnings rally to continue lines up with the consensus and favors price targets comfortably above today’s levels.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend Stock Has Been Steady Amid the Iran War: Is It Still a Buy?

- Boeing Jumps on New Pentagon Deal. Should You Buy BA Stock Here?

- This Tech Stock May Be About to Short Circuit Near 52-Week Highs

- A Giant Meatpacking Strike Isn’t Enough to Dent the Bull Case for JBS Stock, According to Bank of America