The race to dominate artificial intelligence (AI) is no longer just about models; it's increasingly about the infrastructure that powers them. Thus, Intel Corporation (INTC) and Alphabet (GOOGL) have unveiled a deeper, multi-year partnership aimed at advancing next-generation cloud and AI infrastructure, signaling a strategic shift toward vertically integrated, large-scale compute ecosystems.

Under the expanded collaboration, Google will continue deploying Intel’s Xeon processors across its global cloud footprint while jointly developing custom infrastructure processing units (IPUs) designed to optimize networking, storage, and AI workloads. This co-engineered approach reflects a broader industry transition toward heterogeneous computing architectures, where CPUs, accelerators, and custom silicon work in tandem to improve efficiency and performance at hyperscale.

In addition, the partnership reinforces Intel’s relevance in the AI era, particularly within inference and data center orchestration, while strengthening Google’s control over its rapidly expanding AI infrastructure stack. As hyperscalers are expected to collectively pour hundreds of billions into AI data centers, strategic alliances like this will play a critical role in determining which companies capture the most value across the semiconductor and cloud value chain.

Against this backdrop, is the investment case in favor of Intel’s turnaround story, or does it further entrench Alphabet’s dominance in AI-driven cloud computing?

Tech Stock #1: Intel Corporation

Intel Corporation is a leading technology company specializing in the design, development, manufacture, and marketing of semiconductor products, including microprocessors, chipsets, GPUs, memory and related hardware for consumer, enterprise, and industrial markets. Headquartered in Santa Clara, California, Intel remains a key player in data center, PC and emerging AI and networking segments. Intel’s market cap is $325.6 billion, reflecting its valuation among the world’s largest semiconductor companies.

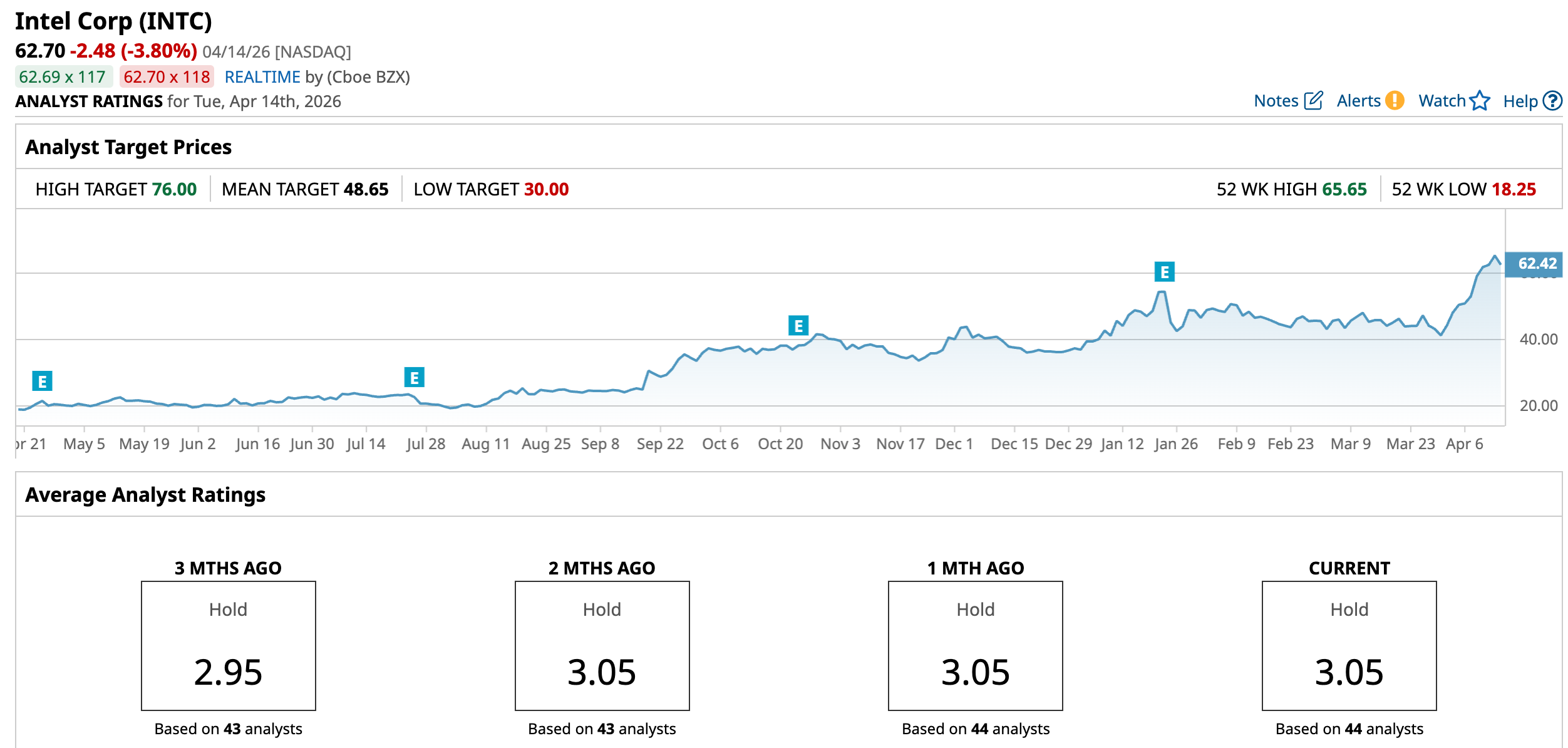

Intel has delivered a dramatic turn in the past year, with the stock emerging as one of the strongest performers in the semiconductor space. Over the past 52 weeks, Intel shares have surged 209.53%, reflecting a sharp recovery from cyclical lows and renewed investor confidence in its AI and foundry strategy.

Year-to-date (YTD), the stock is up 70.37%, building on that recovery and continuing to outperform the broader market as sentiment around AI infrastructure and Intel’s turnaround has improved.

More notable, however, is the exceptional near-term momentum. Intel has staged one of the strongest rallies in decades, including a record multi-day winning streak that drove gains of 18.8% in just over the past five days and 37.35% over the past month alone, pushing the stock to a five-year high of $65.65 on Apr. 13.

This surge has been fueled by a combination of AI-driven enthusiasm, high-profile partnerships such as its collaboration with Google, improving demand for CPUs, and growing credibility in its foundry ambitions.

In terms of valuation, the stock trades at 1,093.26 times forward earnings, which is a significant premium to the sector median.

Coming to its financials, Intel reported its fourth-quarter and full-year 2025 earnings on Jan. 22, after the market close. For the quarter ended Dec. 27, Intel posted net revenue of $13.7 billion, which represents a year-over-year (YOY) decline of about 4% compared with Q4 2024. On profitability, Intel reported non-GAAP earnings per share (EPS) of $0.15, which was up from around $0.13 a year earlier and well above analysts’ estimates.

The Data Center and AI (DCAI) segment delivered one of the strongest performances with approximately $4.7 billion in revenue, up about 9% YOY, highlighting healthy demand. By contrast, the Client Computing Group (CCG) generated about $8.2 billion in revenue, down roughly 7% YOY.

Overall, Total Intel Products revenue was down slightly (about 1% YOY). Intel’s foundry unit reported roughly $4.5 billion in revenue, up around 4% YOY, reflecting the continued ramp of advanced process technologies, while the “All Other” category declined sharply.

For the full year 2025, Intel reported about $52.9 billion in revenue, which was essentially flat compared with 2024, while non-GAAP EPS came in at $0.42, significantly higher than the prior year and marked a return to profitability.

Intel provided guidance for the first quarter of 2026, forecasting revenue between $11.7 billion and $12.7 billion. It also projected a non-GAAP EPS of $0.00, implying a continued lag in supply and margin expansion before anticipated improvements later in the year.

Analysts predict EPS to be around $0.06 for fiscal 2026, an improvement of 150% YOY, and again rise substantially to $0.52 in fiscal 2027.

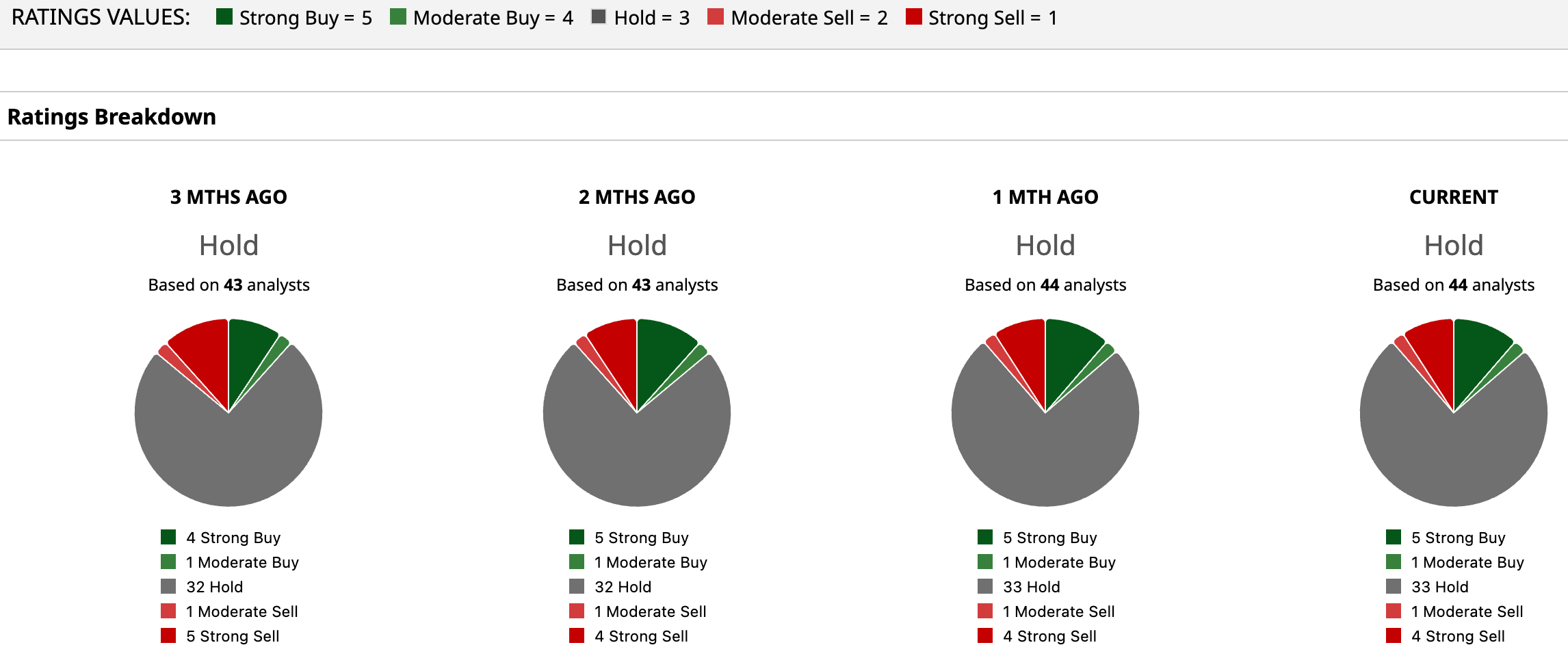

Despite the recent positive price action and developments, INTC has a consensus “Hold” rating, indicating a cautious stance. Of the 44 analysts covering the stock, five advise a “Strong Buy,” one recommends a “Moderate Buy,” 33 analysts are on the sidelines, giving it a “Hold” rating, one suggests a “Moderate Sell,” and four propose a “Strong Sell.”

INTC has already surged past the average analyst price target of $48.65, while the Street-high target price of $76 suggests that the stock could still rally 21.2%.

Tech Stock #2: Alphabet

Headquartered in Mountain View, California, Alphabet has transformed the tech landscape through its wide-ranging businesses, including Google Services, Google Cloud, and forward-looking initiatives like Waymo and Verily. Its strategic focus on artificial intelligence and cloud computing continues to be a major growth engine, reinforcing its strong competitive positioning. It boasts a market cap of $3.9 trillion.

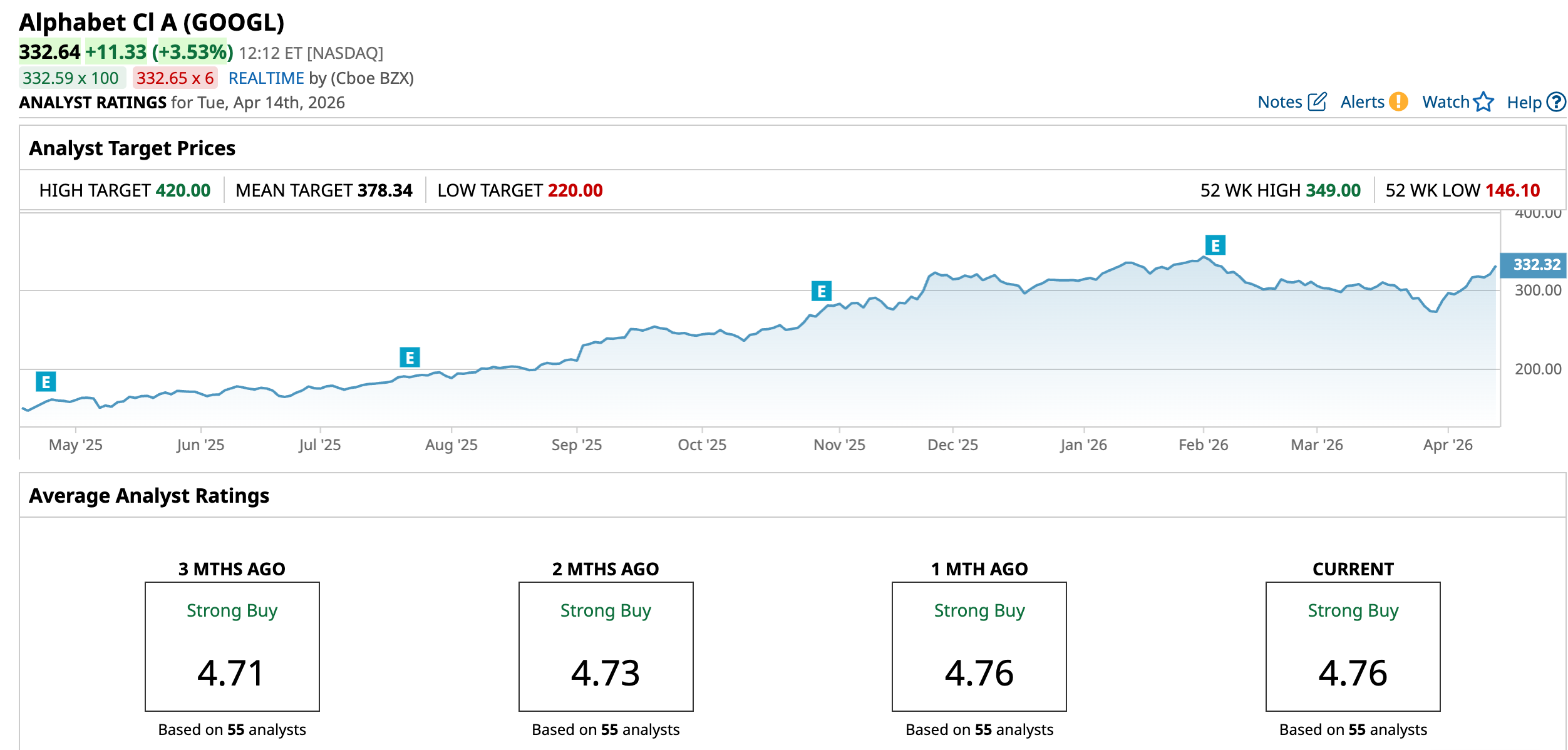

Alphabet has delivered strong absolute returns over the past year, though its trajectory in 2026 has been more measured compared to peers. Over the past 52 weeks, Alphabet stock has gained 108.26%, reflecting AI optimism and cloud acceleration. However, performance has been relatively modest YTD, with returns of around 5.84%.

Following the announcement of its infrastructure partnership with Intel, the stock has shown muted performance rather than a sharp breakout, reflecting the market’s view that such partnerships reinforce Alphabet’s already strong AI positioning rather than fundamentally altering its growth trajectory.

Priced at 27.48 times forward earnings, the stock trades at a premium to the sector median.

Alphabet reported its fourth quarter and full-year 2025 results on Feb. 4. For Q4 2025, Alphabet generated revenue of $113.8 billion, representing 18% YOY growth, while EPS came in at $2.82, up 31.2% YOY from $2.15 in the prior-year period and exceeding the consensus estimate. The quarter reflected broad-based strength, with Google Search continuing double-digit growth, Google Cloud emerging as the key growth engine with 48% YOY revenue growth and YouTube surpassing $60 billion in annual revenue.

For the full year 2025, Alphabet crossed a major milestone, with total revenue reaching approximately $402.8 billion, up 15% YOY, and EPS of about $10.81, up from $8.04, reflecting strong sustained demand across its ecosystem. Notably, this marks the first time the company has exceeded the $400 billion annual revenue threshold, highlighting the scale benefits of its AI-driven platform.

Management further signaled an aggressive investment cycle into 2026, particularly in AI infrastructure and data centers, with capital expenditures expected to rise significantly to support growing cloud and AI demand.

Analysts remain optimistic, forecasting EPS of roughly $11.54 for fiscal 2026, a 6.8% YOY jump, followed by a further 16% rise to $13.39 in 2027.

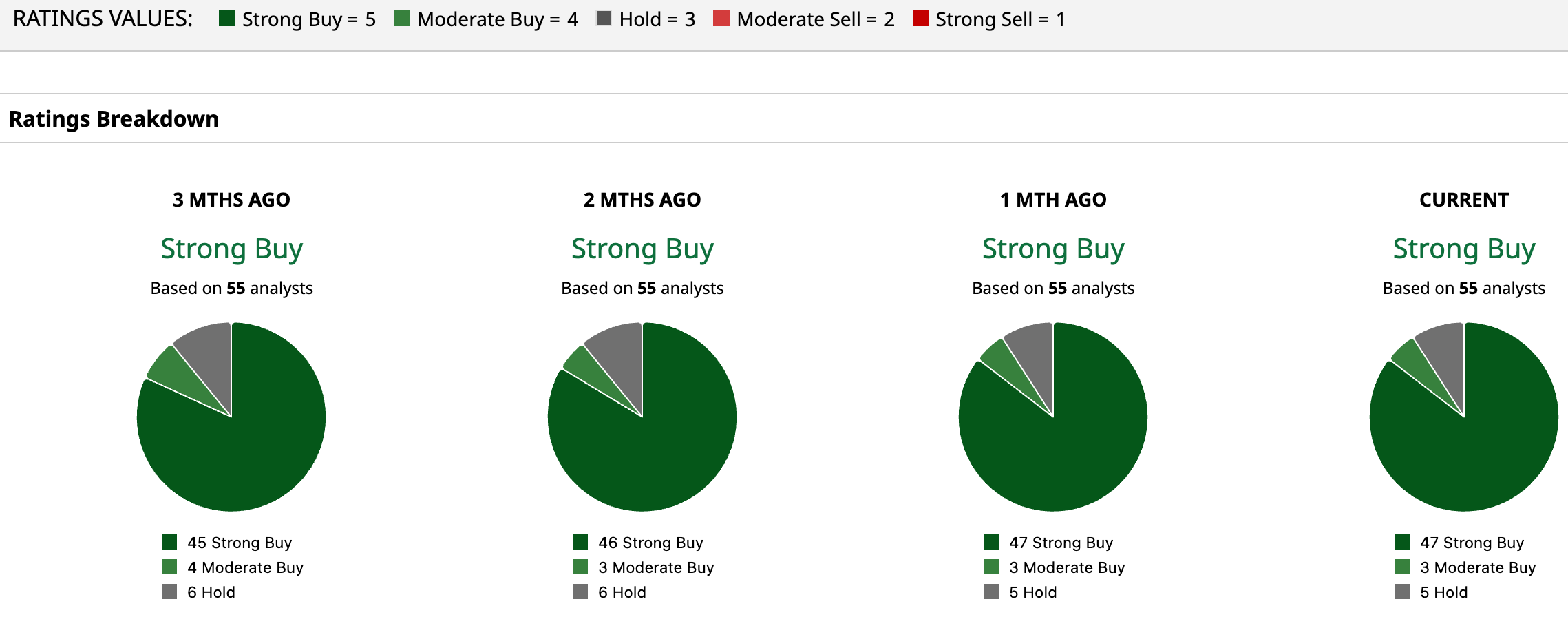

Wall Street is majorly bullish on GOOGL. Overall, GOOGL has a consensus “Strong Buy” rating. Of the 55 analysts covering the stock, 47 advise a “Strong Buy,” three suggest a “Moderate Buy,” and the remaining five analysts are on the sidelines, giving it a “Hold” rating.

GOOGL’s average analyst price target of $378.34 indicates an upside of 13.74%, while the Street-high target price of $420 suggests that the stock could rally as much as 26.26%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- CoreWeave Just Scored a Major Anthropic Data Center Deal. Does That Make CRWV Stock a Buy Here?

- Is Alibaba Stock a Buy as It Reveals It's Behind the Viral Happy Horse AI Model?

- Bloom Energy Breaks Into Overbought Territory on Oracle Deal. Is It Too Late to Buy BE Stock?

- Meta Is Set to Overtake Google in Digital Ads. Is the Stock a Buy Before April 29 Earnings?