For years now, short sellers on Wall Street have treated semiconductor stocks like a dangerous game of timing. These investors bet against companies by borrowing shares and selling them, hoping prices fall so they can buy them back cheaper later. When chip stocks stumble, short sellers see opportunity. When AI excitement takes over, they often get burned. Right now, semiconductor stocks, like Qualcomm (QCOM) are right at the center of it again.

QCOM stock was pressured in 2026 amid weak smartphone demand, a global memory glut, and a cautious near-term outlook. But it recently swung from as low as $122 last month to as high as $247.90 this month. That’s still more than a 100% swing in a short span. So, is this real long-term momentum, or just another sharp rally that fades again?

CNBC recently reported, bearish bets against major semiconductor names remain stubbornly high even as the sector heads into earnings from Nvidia (NVDA) on May 20, Wednesday. That matters because Nvidia’s results have become the pulse of the AI trade, often steering sentiment across the entire chip industry.

Beneath the optimism, cracks are showing. Concerns around slowing smartphone demand, stretched semiconductor valuations, and doubts over whether companies can truly diversify their AI businesses are making investors nervous. Qualcomm sits right in the middle of that uncertainty.

Short interest in Qualcomm has now climbed to nearly $11.8 billion – its highest level in at least a decade. According to S3 Partners’ Ihor Dusaniwsky, short sellers are not capitulating yet, with many believing the recent pullback could be the beginning of a deeper reset after years of AI-fueled momentum.

That puts enormous pressure on Qualcomm. Bulls now need the company’s AI pivot to become more than just a story. They need real growth, real execution, and results that can finally force the skeptics to blink first.

About Qualcomm Stock

San Diego, California-based Qualcomm is a fabless semiconductor company that powers much of the connected world. It runs through its Qualcomm CDMA Technologies (QCT), Qualcomm Technology Licensing (QTL), and Qualcomm Strategic Initiatives (QSI) segments, blending chip innovation with tech licensing and strategic investments. Currently, its market capitalization stands at $224.9 billion.

Best known for its Snapdragon processors and 5G modems, Qualcomm sits inside everything from smartphones to smart homes and even connected cars. After four decades in the game, the company is now pushing deeper into AI-driven computing, energy-efficient performance, and advanced wireless tech. With platforms like Dragonwing, it is also expanding beyond consumer devices into enterprise and industrial markets, aiming to stay relevant as computing spreads everywhere.

As slightly discussed before, QCOM stock, for most of 2026, struggled under the weight of weak smartphone demand, a global memory glut, and concerns that its traditional handset business was slowing down faster than investors expected. By April, sentiment around the stock had become so negative that short sellers piled in aggressively, betting the weakness still had room to continue. Then the story suddenly changed.

Even after pulling back about 13.9% from those record highs, QCOM is still up 62.75% over the past 52 weeks. The momentum has been remarkable – the chip stock has gained 40.22% year-to-date (YTD), surged 67.86% in the last three months, and skyrocketed 76.26% in just the past month alone.

The rally was fueled by a mix of strong catalysts. Qualcomm's Q2 results on April 29 gave investors fresh confidence. But the bigger surprise came when CEO Cristiano Amon revealed that the company’s new data center processors are expected to ship to a major hyperscaler customer before the end of calendar 2026. That announcement suddenly pushed Qualcomm deeper into the AI conversation and sparked hopes that the company may finally become more than just a smartphone chipmaker. At the same time, easing U.S.-China tariff tensions and a wave of analyst upgrades added more fuel to the rally.

After the recent rally, QCOM stock’s valuation is feeling a bit stretched. It now trades around 5.30 times forward sales, which is above its sector average and also higher than its own historical median. Plus, QCOM is priced at 19.77 times forward adjusted earnings. That’s still slightly below some chip peers, but when we look at its own past five years, it is clearly on the richer side.

The stock is not overheated, but no longer cheap either. The market is basically pricing in execution, especially around AI, and expecting Qualcomm to deliver.

If one is looking at QCOM not just for growth, but for steady cash in the pocket while waiting, the dividend story still adds some comfort. The company has built a long track record here, executing 22 consecutive years of dividend increases. It shows consistency through different chip cycles.

The latest raise of about 3.4% lifts the quarterly payout to $0.92 per share, or $3.68 annually. At current levels, that works out to a forward yield of roughly 1.82%. With a payout ratio near 30%, Qualcomm is not overextending itself.

A Snapshot of Qualcomm's Q2 Report

Qualcomm's second-quarter fiscal 2026 earnings arrived in April with a familiar mix of short-term softness and long-term signal. The numbers looked a bit muted, but the underlying narrative stayed firmly forward-looking.

Q2 revenue slipped 2% year-over-year (YOY) to $10.6 billion, down, while non-GAAP EPS amounted to $2.65. That represented a 7% annual decline, yet still managed to beat Street’s expectations, underscoring that profitability held up better than the top-line pressure suggested. Management largely attributed the slowdown not to demand collapse, but to a constrained memory chip supply environment that weighed on handset OEM production and purchasing behavior.

Segment-wise, the QCT revenue fell 4% YOY to $9.1 billion, reflecting pressure in smartphones. In contrast, the QTL segment offered a steadier backdrop, rising 5% annually to $1.4 billion, helping cushion overall performance.

Even with handset headwinds, diversification trends stood out. Automotive continued to be the brightest structural growth pillar. Qualcomm highlighted record automotive sales and crossed a key milestone – more than $5 billion in annualized automotive revenue for the first time.

Looking ahead, the company expects to finish fiscal 2026 at a run rate above $6 billion, powered by its Snapdragon Digital Chassis platform spanning connectivity, telematics, infotainment, and advanced driver assistance systems. Adoption is already visible, with over one million vehicles running ADAS and autonomy workloads on Snapdragon Ride processors, and next-gen platform shipments expected to begin by the end of the fiscal year.

Also, the IoT business showed steady momentum, supported by product renewal design cycles linked to edge AI adoption. Management pointed to healthy pipeline activity across consumer and industrial segments as workloads increasingly shift toward on-device intelligence and context-aware computing. This shift is reinforcing the company’s push deeper into industrial AI, robotics, and factory automation ecosystems through new partnerships and platform initiatives.

Qualcomm continued to generate robust cash flows. For the first six months of fiscal 2026, operating cash flow reached $7.4 billion, while ending Q2 with $5.44 billion in cash and cash equivalents, comfortably exceeding its short-term debt of $498 million, reinforcing balance sheet resilience even in a choppier demand environment.

Guidance for Q3 2026 was broadly aligned with expectations. Revenue is projected between $9.2 billion and $10 billion, while non-GAAP EPS is guided in the range of $2.10 to $2.30. At the midpoint, both metrics sit close to analyst estimates, signaling stability rather than acceleration in the near term.

However, management did offer a more nuanced read on the demand cycle. It expects QCT handset revenue from China-based customers to bottom in the third quarter before returning to sequential growth in the following period, as inventory corrections gradually ease. Still, near-term visibility remains tied to memory supply constraints and pricing pressures, keeping the recovery path gradual rather than sharp.

Analysts tracking the company predict Qualcomm's Q3 revenue to be around $9.66 billion, while non-GAAP EPS is expected to be somewhere around $2.23 for the quarter. Looking ahead, EPS is expected to slip 20.7% YOY to $7.99 in fiscal 2026, and decline by another 1.75% annually to $7.85 in fiscal 2027.

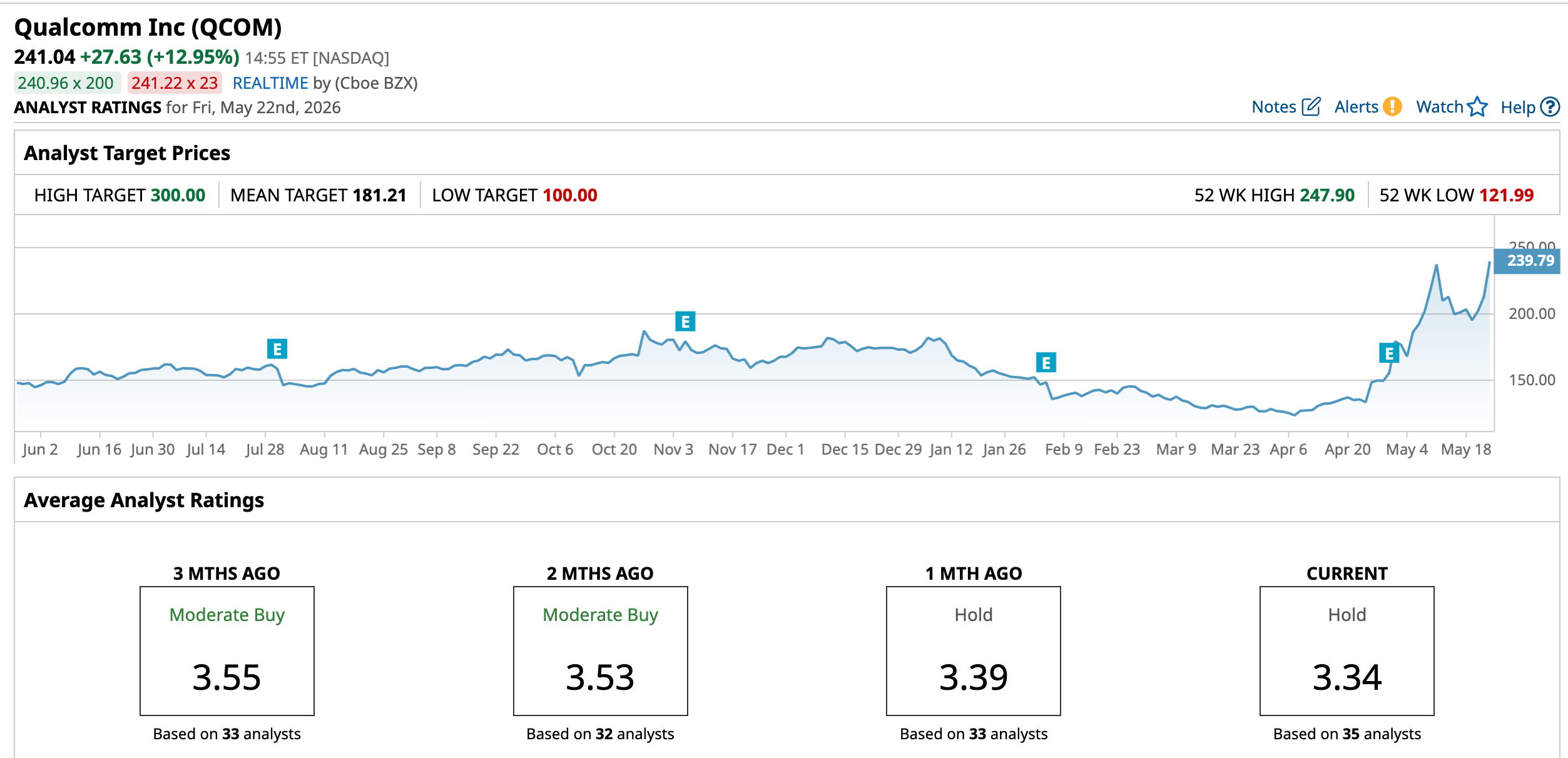

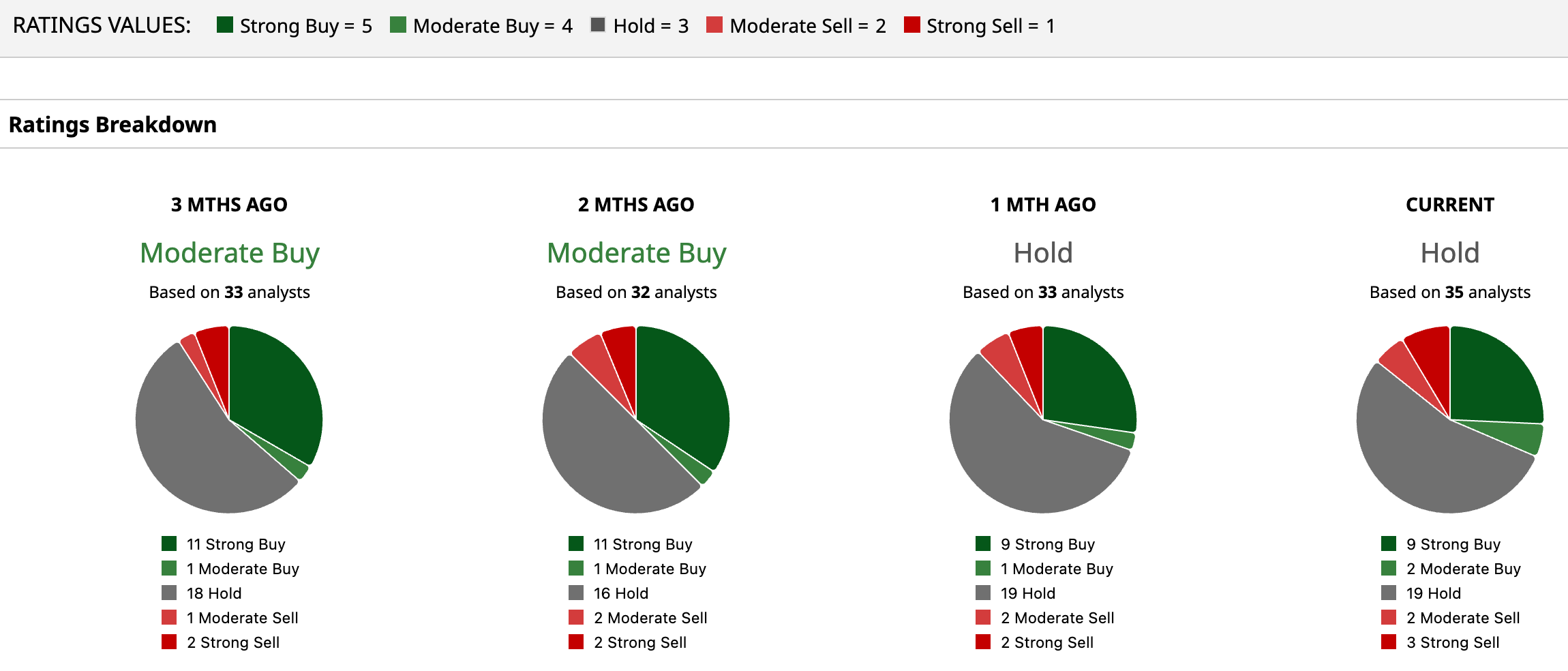

What Do Analysts Expect for QCOM Stock?

Overall, Wall Street rates QCOM stock a “Hold,” a downgrade from a “Moderate Buy” two months back. Out of the 35 analysts that cover the stock, nine suggest a “Strong Buy,” two recommend a “Moderate Buy,” 19 analysts are playing it safe with a “Hold” rating, two have a “Moderate Sell,” and the remaining three rate it a “Strong Sell.”

While the recent rally has pushed QCOM stock above the mean price target of $181.21, but based on the Street-high target price of $300, the stock could rally as much as 24.5% in the next 12 months.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Nvidia Just Raised Its Dividend by 2,400%. NVDA Stock Is Still a Bet on Growth, Not Income.

- Short Sellers Aren’t Relenting Against Qualcomm. The Chipmaker Needs to Quickly Deliver on Its AI Pivot for Bulls to Win.

- Microsoft vs. Apple Stock: The Numbers Reveal a Clear Winner Heading Into H2 2026

- Why Wall Street Thinks This Dividend Stock Could Jump 30%