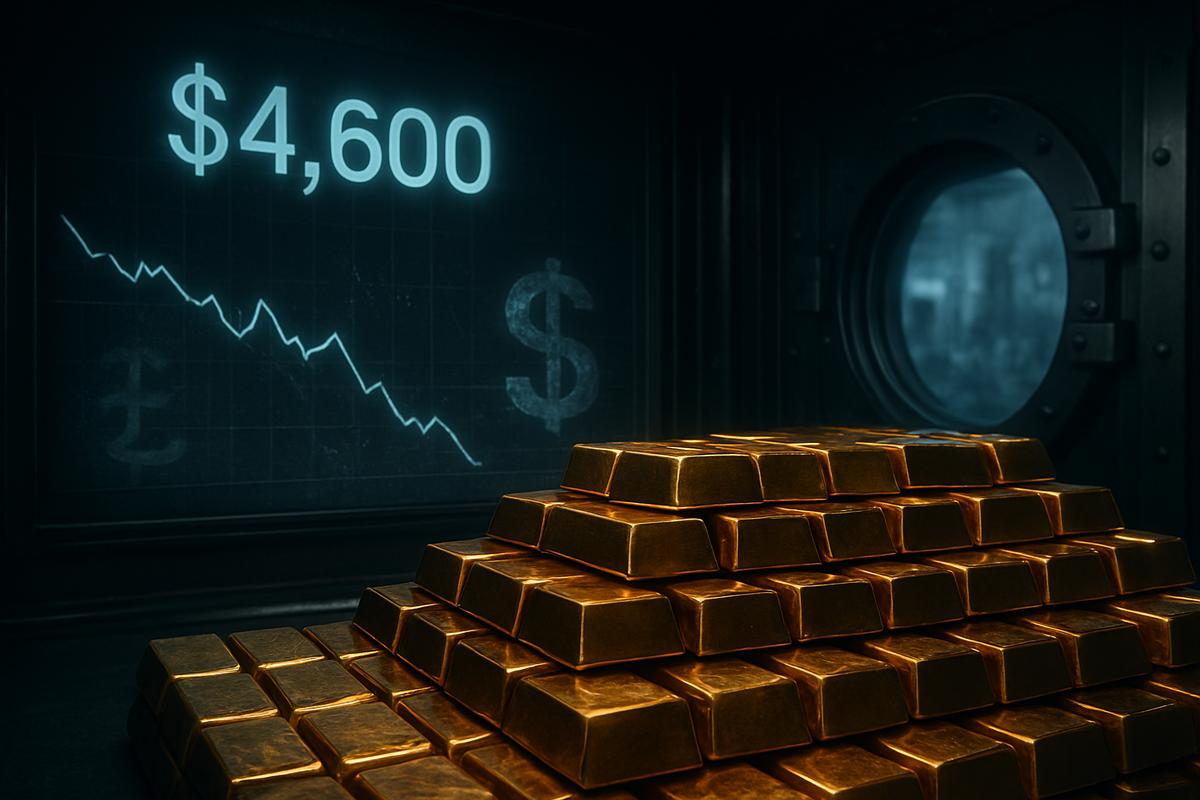

As of January 15, 2026, the global financial landscape has been fundamentally reshaped as gold prices surged to an unprecedented $4,600 per ounce. This historic rally represents a nearly 100% increase over the last 18 months, driven by a "perfect storm" of systemic instability, a weakening U.S. dollar, and a series of geopolitical shocks that have sent investors fleeing toward the ultimate safe-haven asset. The breach of the $4,600 level has triggered massive liquidations in traditional equity markets and a frantic rebalancing of institutional portfolios toward hard assets.

The immediate implications are profound: inflation expectations are being recalibrated globally, and the cost of capital is shifting as the perceived risk of fiat currencies rises. For the average consumer, this surge in gold is not merely a headline but a signal of diminishing purchasing power, while for central banks, it marks a definitive pivot away from Western-centric reserve assets. As the yellow metal enters uncharted territory, the question for the market is no longer if gold belongs in a portfolio, but how much one can afford to be without it.

A Perfect Storm: The Path to $4,600

The journey to $4,600 was catalyzed by a breakdown in institutional trust. Throughout 2025, the Federal Reserve struggled with a "credibility gap" that widened into a chasm following news of a federal investigation into Chair Jerome Powell. This unprecedented scrutiny of the U.S. central bank’s independence sparked a massive sell-off in the U.S. Treasury market, forcing yields higher and the dollar lower. By the time the calendar turned to 2026, the dollar had lost nearly 12% of its value against a basket of global currencies, making gold an attractive alternative for those seeking to preserve wealth.

Geopolitically, the world has remained in a state of high friction. The recent U.S. military operations in South America and the continued escalation of tensions between Iran and Israel have added a permanent "war premium" to commodity prices. Every major geopolitical flare-up in 2025 acted as a floor for gold prices, preventing any significant corrections. Furthermore, the persistent conflict in Ukraine and the resulting sanctions have solidified a trend of "de-dollarization," as emerging market central banks—most notably the People’s Bank of China—continue to buy gold at a rate of nearly 600 tonnes per quarter to diversify their reserves.

Market reactions have been swift and binary. While precious metals desks at major investment banks are seeing record volumes, the broader indices have struggled to cope with the volatility. Analysts at JPMorgan and Goldman Sachs have already revised their mid-2026 targets to $5,000 per ounce, citing the structural deficit in gold supply and the lack of viable alternatives in a high-debt, high-inflation environment. Retail demand has also spiked, with physical gold premiums reaching 15% above spot prices in many European and Asian markets.

Winners and Losers in the Golden Era

The primary beneficiaries of this price surge are the major mining conglomerates, which are now generating record-breaking free cash flow. Newmont Corporation (NYSE: NEM), the world’s largest producer, has seen its margins expand exponentially as the price of its product rose far faster than its operational costs. Similarly, Barrick Gold Corp (NYSE: GOLD) and Agnico Eagle Mines (NYSE: AEM) have reported stellar quarterly earnings, allowing them to hike dividends and reinvest in high-grade exploration projects that were previously deemed too expensive to develop.

The investment vehicle market has also seen a massive influx of capital. The SPDR Gold Shares (NYSE Arca: GLD) remains the primary destination for institutional liquidity, seeing its assets under management swell to record highs. For investors seeking higher risk and higher reward, the VanEck Gold Miners ETF (NYSE Arca: GDX) has become a top performer, providing leveraged exposure to the rising profitability of the mining sector. Streaming and royalty companies like Franco-Nevada (NYSE: FNV) are also winning big, as they benefit from higher gold prices without the direct burden of rising labor and energy costs in mining operations.

Conversely, the losers are found in industries sensitive to raw material costs and interest rate volatility. Luxury goods manufacturers and electronics firms that rely on gold for industrial applications are facing a margin squeeze. Furthermore, traditional "growth" tech stocks have faced headwinds as the rising gold price signals higher structural inflation, leading to higher discount rates on future earnings. Small-scale jewelry retailers are also struggling, as the $4,600 price tag has effectively priced out a large segment of the middle-class consumer market, leading to a pivot toward alternative metals and lab-grown stones.

Re-evaluating the Global Monetary Order

This event fits into a broader trend of "hard asset" dominance that has been building since the early 2020s. The move to $4,600 is widely seen as a rejection of the modern monetary policy that characterized the last two decades. With global debt reaching a staggering $346 trillion in late 2025, the market is effectively "pricing in" a future where debt cannot be repaid in current dollar terms. Gold’s rise is a symptom of this systemic debt crisis, echoing the inflationary cycles of the 1970s but on a much larger, global scale.

The ripple effects are being felt across all asset classes. Competitors to gold, such as Bitcoin and other digital assets, have also seen gains, but the physical nature of gold remains the preferred choice for central banks and sovereign wealth funds. This has significant policy implications; we are seeing a renewed debate over the "Gold Standard" or at least a "Gold-Backed Reserve" in some BRICS nations. Regulatory bodies are now moving to ensure that "paper gold" markets—the derivatives and futures—are sufficiently backed by physical metal to prevent a systemic collapse if physical delivery is demanded en masse.

Historically, such sharp moves in gold often precede a major shift in the economic regime. Comparisons are being made to the 1971 "Nixon Shock" when the U.S. left the gold standard. Today, the "Powell Shock" of institutional instability may represent the reverse: a market-led return to gold because the trust in central planners has evaporated. The historical precedent suggests that once a safe haven reaches this level of momentum, it rarely returns to its previous baseline without a total restructuring of the underlying monetary system.

The Horizon: What Comes After $4,600?

In the short term, the market is bracing for extreme volatility. As gold approaches the psychological $5,000 barrier, technical resistance and profit-taking are expected. However, any dip is likely to be met with aggressive buying from institutional players who missed the initial leg of the rally. Strategic pivots are already underway at many hedge funds, which are rotating out of long-duration bonds and into "permanent portfolios" that hold significant weightings in bullion and mining equities.

The longer-term outlook depends heavily on whether the Federal Reserve can restore its reputation and whether global conflicts find a diplomatic resolution. If inflation remains unanchored and the U.S. deficit continues to spiral, $4,600 may eventually be viewed as a mid-point rather than a peak. The primary challenge for the market will be the "physical squeeze"—the potential for a shortage of available bullion as demand outstrips the annual mining output, which has been largely stagnant for several years.

We may also see a scenario where governments attempt to intervene in the gold market to defend their fiat currencies. This could take the form of windfall taxes on mining profits or restrictions on the private ownership of large quantities of gold. Investors should be prepared for a "gold-driven" macro environment where the yellow metal dictates the direction of the dollar and interest rates, rather than the other way around.

Final Assessment for the Road Ahead

The surge of gold to $4,600 is a watershed moment for the 2020s. It marks the transition from an era of cheap money and institutional stability to one of "real value" and geopolitical fragmentation. The key takeaway for investors is that the "Gold Premium" is no longer a temporary feature of the market; it is a structural necessity in a world where the foundations of the global financial system are being questioned.

Moving forward, the market will likely remain in a "risk-off" posture until there is a clear path toward fiscal responsibility and geopolitical de-escalation. Investors should watch the quarterly reports from central banks for any signs of slowing their gold purchases, as well as the monthly inflation prints, which will dictate the Fed's ability to fight back against the currency's decline. While the $4,600 level is a massive milestone, the underlying causes of the rally remain unresolved, suggesting that the "Golden Era" is far from over.

This content is intended for informational purposes only and is not financial advice.