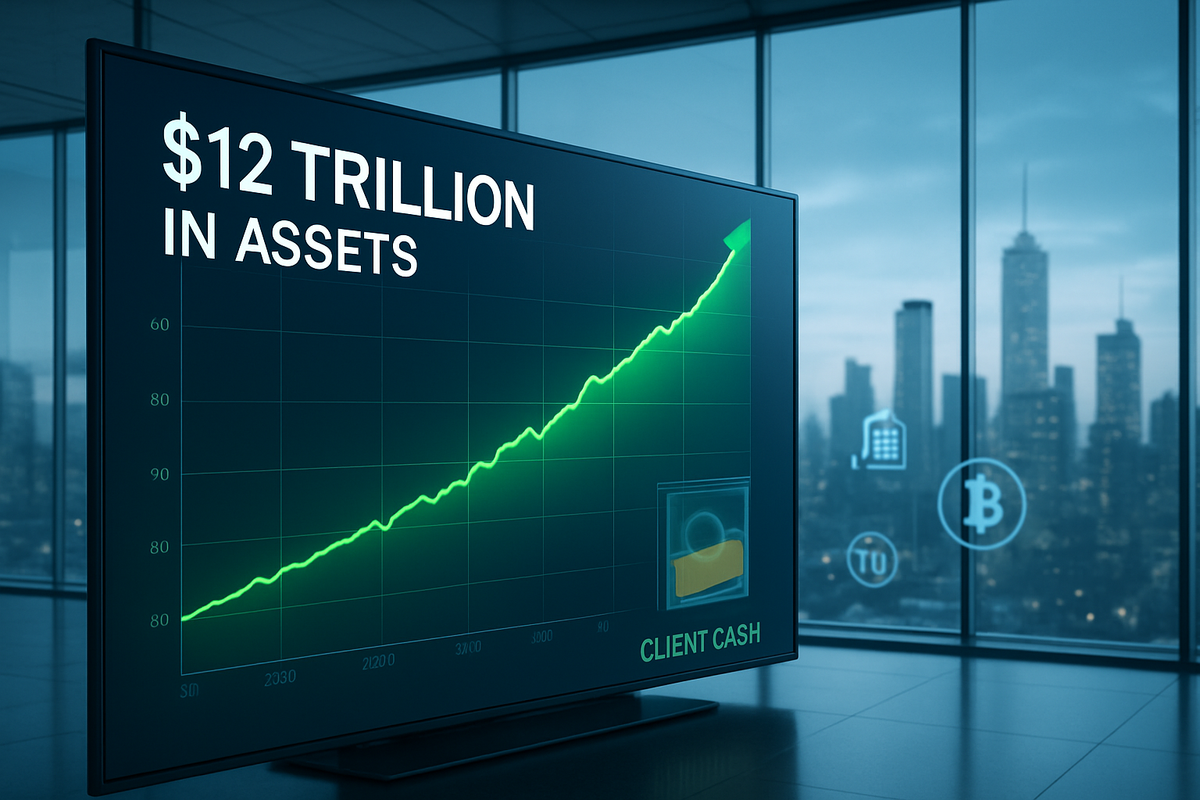

As of January 23, 2026, the financial landscape is digesting a complex set of results from Charles Schwab (NYSE: SCHW). On January 21, the brokerage giant reported fourth-quarter and full-year 2025 results that showcased a firm of unprecedented scale, boasting nearly $12 trillion in total client assets. However, despite record-breaking numbers in several categories, a lingering "sluggishness" in client cash recovery has left analysts and investors questioning the long-term trajectory of the company’s most profitable engine.

The immediate market reaction was a measured "sell the news" event, with Schwab’s stock sliding between 1.5% and 3% following the announcement. While the firm successfully navigated the "cash sorting" crisis that defined 2023 and 2024, the expected rebound of low-cost transactional cash has not fully materialized. This development signals a permanent shift in investor behavior that may force Schwab—and the broader brokerage industry—to rethink how they monetize the retail balance sheet in a post-inflationary world.

Record-Breaking Scale Meets the 'Sorting' Plateau

In its Q4 2025 report, Charles Schwab delivered an adjusted earnings per share (EPS) of $1.39, a 38% increase over the previous year, precisely matching Wall Street consensus. Net revenue for the quarter hit a record $6.34 billion, though this figure fell slightly short of the $6.38 billion analysts had projected. The driver behind the revenue miss was the primary point of contention: interest-earning assets. While total client assets reached a staggering $11.90 trillion, the transactional sweep cash—the low-yield funds that Schwab uses to generate net interest revenue—stood at $453.7 billion. Although this was a $28.1 billion increase from the prior quarter, the recovery is being described by market watchers as "sluggish."

The timeline leading to this moment has been one of aggressive deleveraging. Throughout 2025, Schwab focused on paying down the expensive supplemental funding it took on during the regional banking crisis of 2023. By the end of Q4 2025, the firm had reduced its reliance on Federal Home Loan Bank (FHLB) loans to just $5.1 billion, down from nearly $15 billion a year earlier. This strategy successfully expanded Schwab’s Net Interest Margin (NIM) to 2.90%, up 57 basis points year-over-year. CEO Rick Wurster, who took the helm following the retirement of long-time leaders, declared that the "cash sorting" crisis had effectively ended, yet he admitted that client cash allocations remain at historical lows.

Currently, client cash makes up roughly 9.6% of average assets at Schwab, a notable departure from the 10-year historical average of 11.4%. The "sorting" behavior—where clients move idle cash into higher-yielding money market funds or Treasuries—has not reversed as many had hoped. Instead, it has plateaued. Investors in 2026 remain highly yield-conscious, preferring to keep their capital "at work" in managed solutions or high-yield vehicles rather than letting it sit in transactional accounts that typically yield near zero.

The Winners and Losers of the New Liquidity Era

The shift in cash dynamics has created a clear set of winners and losers within the financial services sector. Charles Schwab (NYSE: SCHW) itself emerges as a winner in terms of structural stability; by flushing out high-cost debt and hitting record asset levels, the firm is "leaner and meaner" than it was two years ago. However, the sluggish cash recovery means that Schwab's ability to generate "easy" interest income is capped compared to previous cycles. To compensate, the firm is aggressively pursuing a winner-take-all strategy in private markets, evidenced by its planned acquisition of Forge Global (NYSE: FRGE), a specialist in private company shares.

On the other side of the aisle, Fidelity Investments (Private) and Vanguard (Private) have emerged as "shadow winners." By offering high-yield default sweep options—such as Fidelity’s SPAXX money market fund—these firms have captured massive inflows from yield-sensitive retail investors who no longer wish to manually "sort" their cash. This has forced traditional brokerages to work harder for every dollar of revenue. Meanwhile, Morgan Stanley (NYSE: MS) has solidified its position as a winner in the advisory-led model. With wealth management margins hitting record highs of 31.4% in late 2025, Morgan Stanley has proven that a focus on fee-based advice is less vulnerable to the "sluggish" cash trends currently plaguing the self-directed brokerage model.

The "losers" in this environment are primarily the retail clients who have failed to move their idle cash, still earning a nominal 0.05% in basic bank sweeps while the Federal Funds rate remains around 3.25%. Furthermore, small-cap regional banks continue to lose the "war for deposits" as the gravity of the massive brokerage platforms like Schwab continues to pull in net new assets at a rate of over $160 billion per quarter.

A Wider Shift Toward Asset Monetization

The events surrounding Schwab’s latest earnings reflect a broader industry trend: the transition from an interest-spread-dependent model to a total asset monetization model. In the decade of near-zero interest rates, brokerages relied on "free" client cash to drive profits. In the 2026 economy, that "free" cash has largely vanished as digital tools and financial literacy have made yield-seeking the default behavior for even the smallest retail accounts.

This ripple effect is visible across the sector. Competitive pressure is mounting to integrate "tokenized cash sleeves" and "atomic settlement" systems that allow clients to earn yield on their money until the very millisecond it is needed for a trade or a bill payment. Such technological advancements, which were once niche, are becoming standard in 2026, further eroding the pool of idle transactional cash. This is a historical precedent in the making—never before has such a large portion of retail wealth been so actively managed and yield-sensitive.

Furthermore, regulatory scrutiny remains high. The "sluggish" recovery of cash into low-yield accounts is being watched by policymakers interested in "best interest" standards for cash sweeps. While Schwab has successfully navigated these waters so far, the industry is moving toward a future where the "spread" model is replaced by transparent, fee-based wealth management. Schwab’s pivot toward cryptocurrency trading and private equity access for the masses is a direct response to these shifting sands.

The 2026 Roadmap: Pivots and Private Markets

Looking ahead, Schwab has provided a robust guidance for 2026, projecting adjusted EPS between $5.70 and $5.80. To reach these targets, the firm is expected to lean heavily into strategic pivots. The most significant of these is the integration of Forge Global (NYSE: FRGE), which will allow Schwab clients to trade pre-IPO shares and other alternative assets directly through their brokerage accounts. This move is designed to capture higher-margin transaction fees and management fees to offset the plateau in net interest income.

In the short term, the market will be watching the closing of the Forge deal and the launch of Schwab’s direct cryptocurrency trading platform. These initiatives represent a "new era" for the company, moving it away from its roots as a discount stock broker and toward becoming a comprehensive digital wealth manager. The challenge will be maintaining its famous low-cost culture while building out the sophisticated infrastructure required for private and digital asset custody.

Long-term, the scenario for Schwab depends on where interest rates settle. If the Federal Reserve continues to hold rates above 3%, the incentive for clients to keep cash "at work" will remain high, keeping the pressure on Schwab's balance sheet. However, if the firm can successfully transition its $12 trillion asset base into managed products, the sheer scale of the company could provide a moat that competitors will find nearly impossible to breach.

Final Assessment: A Strong Foundation in a Changing World

The takeaway from Schwab’s latest earnings is that the firm has reached a pinnacle of scale, but the "gold mine" of cheap client cash is no longer as deep as it once was. The sluggish recovery of transactional cash is not a sign of weakness in Schwab’s brand—evidenced by the record $163.9 billion in net new assets this quarter—but rather a sign of a more sophisticated and demanding retail investor. Schwab is no longer just competing with other brokers; it is competing with every high-yield alternative in the digital world.

Moving forward, investors should keep a close eye on two metrics: the Net Interest Margin (NIM) target of 2.95% and the growth of "Managed Solutions" inflows. If Schwab can continue to grow its fee-based business while keeping its NIM stable, it will likely maintain its dominance. The era of "cash sorting" may be over, but the era of "asset monetization" has just begun. For the market, the message is clear: the Schwab of 2026 is a different beast than the Schwab of 2020, and its success will now be measured by how well it can serve the "fully invested" client.

This content is intended for informational purposes only and is not financial advice.