Let’s dig into the relative performance of Wyndham (NYSE: WH) and its peers as we unravel the now-completed Q2 travel and vacation providers earnings season.

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

The 18 travel and vacation providers stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was in line.

While some travel and vacation providers stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.5% since the latest earnings results.

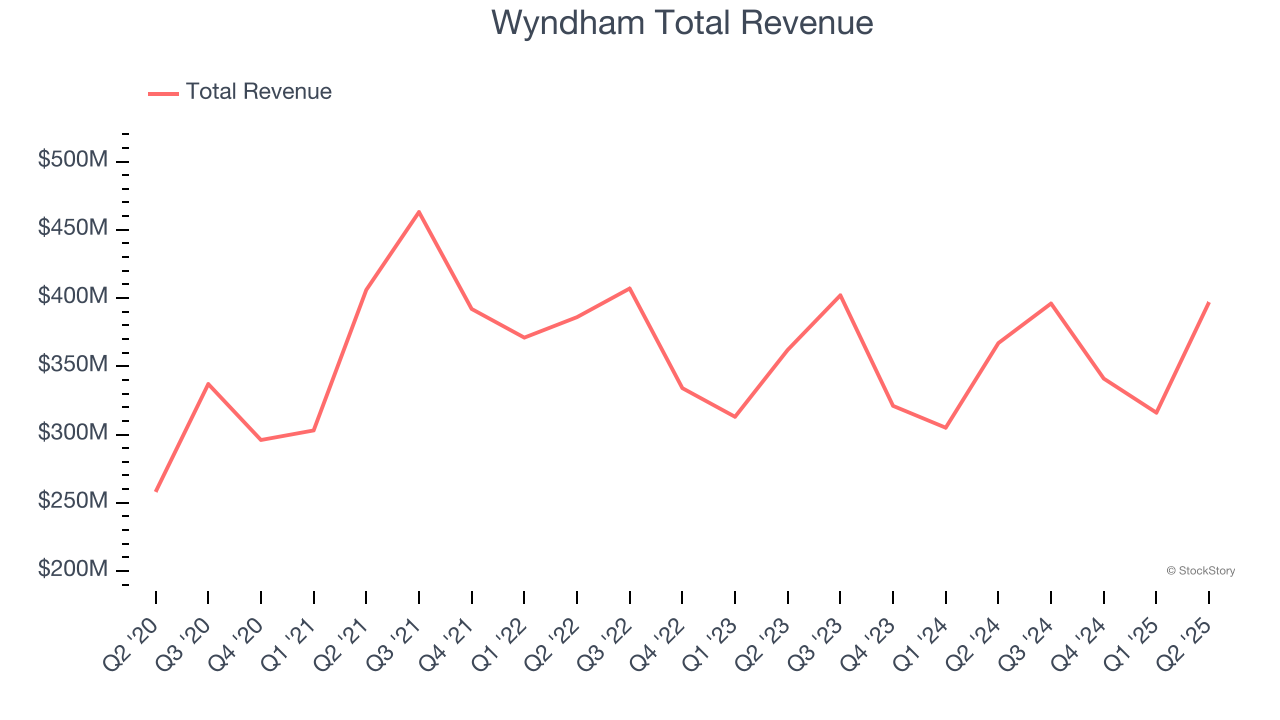

Wyndham (NYSE: WH)

Established in 1981, Wyndham (NYSE: WH) is a global hotel franchising company with over 9,000 hotels across nearly 95 countries on six continents.

Wyndham reported revenues of $397 million, up 8.2% year on year. This print exceeded analysts’ expectations by 2.5%. Overall, it was a satisfactory quarter for the company with a beat of analysts’ EPS estimates but a slight miss of analysts’ adjusted operating income estimates.

"We delivered another solid quarter growing our global system by 4%, expanding our development pipeline by 5%, increasing our ancillary revenues by 19%, and continuing to execute our strategy focused on higher FeePAR segments and markets, which is driving growth in both domestic and international royalty rates," said Geoff Ballotti, president and chief executive officer.

Unsurprisingly, the stock is down 5.9% since reporting and currently trades at $81.03.

Is now the time to buy Wyndham? Access our full analysis of the earnings results here, it’s free for active Edge members.

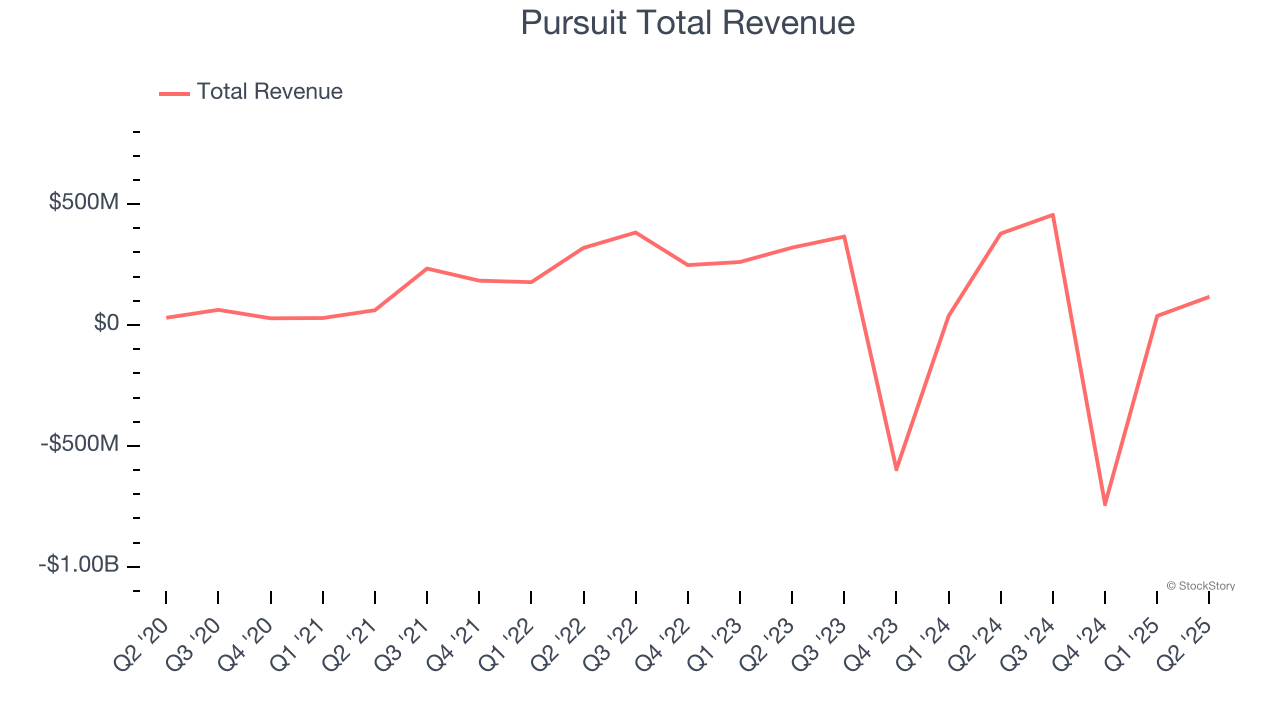

Best Q2: Pursuit (NYSE: PRSU)

With attractions ranging from glacier tours in the Canadian Rockies to an oceanfront geothermal lagoon in Iceland, Pursuit Attractions and Hospitality (NYSE: PRSU) operates iconic travel experiences across North America and Europe.

Pursuit reported revenues of $116.7 million, down 69.2% year on year, outperforming analysts’ expectations by 6.9%. The business had a stunning quarter with a beat of analysts’ EPS estimates and full-year EBITDA guidance exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 21.2% since reporting. It currently trades at $36.39.

Is now the time to buy Pursuit? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: Hilton Grand Vacations (NYSE: HGV)

Spun off from Hilton Worldwide in 2017, Hilton Grand Vacations (NYSE: HGV) is a global timeshare company that provides travel experiences for its customers through its timeshare resorts and club membership programs.

Hilton Grand Vacations reported revenues of $1.27 billion, up 2.5% year on year, falling short of analysts’ expectations by 8.1%. It was a disappointing quarter as it posted and a significant miss of analysts’ adjusted operating income estimates.

Hilton Grand Vacations delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 13.6% since the results and currently trades at $43.85.

Read our full analysis of Hilton Grand Vacations’s results here.

Choice Hotels (NYSE: CHH)

With almost 100% of its properties under franchise agreements, Choice Hotels (NYSE: CHH) is a hotel franchisor known for its diverse brand portfolio including Comfort Inn, Quality Inn, and Clarion.

Choice Hotels reported revenues of $426.4 million, down 2% year on year. This result met analysts’ expectations. Taking a step back, it was a mixed quarter as it also produced full-year EBITDA guidance slightly topping analysts’ expectations but a miss of analysts’ adjusted operating income estimates.

The stock is down 16.9% since reporting and currently trades at $103.96.

Read our full, actionable report on Choice Hotels here, it’s free for active Edge members.

Lindblad Expeditions (NASDAQ: LIND)

Founded by explorer Sven-Olof Lindblad in 1979, Lindblad Expeditions (NASDAQ: LIND) offers cruising experiences to remote destinations in partnership with National Geographic.

Lindblad Expeditions reported revenues of $167.9 million, up 23% year on year. This number surpassed analysts’ expectations by 5.6%. Overall, it was a very strong quarter as it also recorded a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Lindblad Expeditions pulled off the fastest revenue growth but had the weakest full-year guidance update among its peers. The stock is up 6.2% since reporting and currently trades at $12.47.

Read our full, actionable report on Lindblad Expeditions here, it’s free for active Edge members.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.