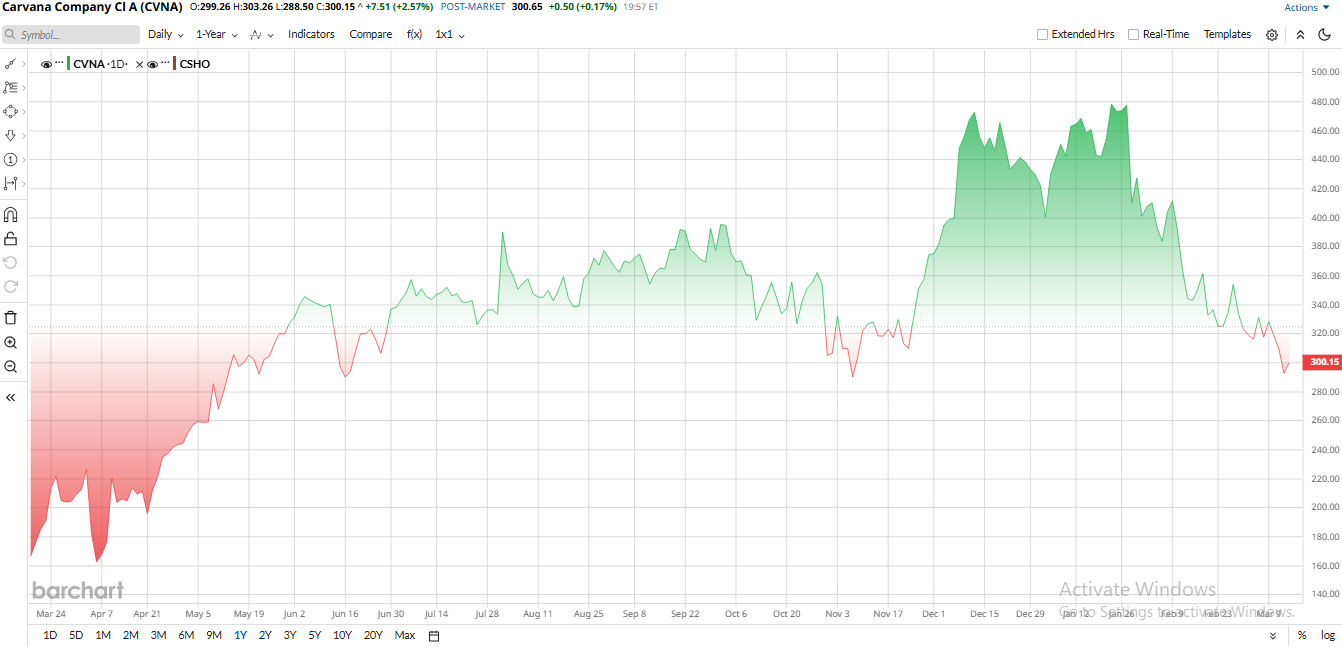

In recent months, e-commerce and auto-retail stocks have been on a roller coaster. After plummeting through 2022, used-car sellers staged a comeback as record sales drove Carvana (CVNA) to 2025 profits. Carvana, in fact, became 2025’s top-performing auto retailer stock, more than doubling in price on surging revenue and unit growth. With growth stocks cooling off in early 2026, Carvana’s rally has petered out a bit, and traders are asking: Was it all hype?

Now Carvana’s board has approved a 5-for-1 split (pending shareholder vote) to “make whole shares more accessible” after that run. Let’s unpack what that means for CVNA.

Carvana Scales Logistics Network

Carvana is an online used-car retailer that sells, finances, and delivers cars via the internet. Indeed, the company has become one of the largest used-car dealers in the U.S., handling over 4 million customer transactions so far.

As the company continues scaling its platform, management has been expanding logistics and delivery capabilities to improve customer experience. Recently, it rolled out its same-day delivery service in Los Angeles, having earlier launched it in Eugene, Ore., and other metro areas. These moves are meant to speed up deliveries and make the service stickier.

At the same time, Carvana also made headlines by debuting at the Morgan Stanley Tech/Media conference in February, which helped expose the name to institutional investors. Notably, Carvana landed in the S&P 500 ($SPX) in late 2025, a milestone that expands its ownership base.

Meanwhile, management has been focusing on strengthening the balance sheet as the used-car market normalizes. On the capital side, the company’s debt is coming down, and inventory levels are being managed carefully amid easing auto prices. In short, Carvana is plowing ahead on its expansion and integration plans to drive further growth.

Carvana Bulls View Dip as Long-Term Opportunity

That bullishness has been seen in CVNA stock, which rode a wild run in 2025. It has been up 70% over the year as Carvana’s turnaround gathered steam. Unit sales jumped 43% in 2025, and revenue leapt nearly 50%, fueling investor enthusiasm. In January 2026, CVNA peaked near $486, but since then, it has given back a chunk of those gains. Unfortunately, shares are down roughly 27% YTD, underperforming peers. The pullback came due to broader market weakness, profit-taking, and some fresh doubts, e.g., a recent short-seller report and higher costs. Still, the company is growing strongly, so many bulls see the dip as a chance to accumulate.

The stock now trades at lofty multiples. CVNA is notably overvalued with a price-to-book ratio of 14, significantly higher than the sector median of 2, and a P/E ratio of 40, much above the sector median of 16. That shows CVNA is quite expensive relative to traditional car dealers. But here is the case that if Carvana hits its ambitious targets, the multiples may seem justified; if not, the stock could lose steam.

5-for-1 Stock Split Announced

On March 13, Carvana’s board approved a 5-for-1 forward stock split. Each shareholder of record on May 6 would get 4 extra shares on a split-adjusted basis, trading at one-fifth the prior price from May 7. Management says the split is aimed at keeping shares affordable, especially for its own employees under equity plans, after the stock’s strong run.

Investors initially liked the news. CVNA popped about 3% on the announcement. This reaction isn’t unusual. Market watchers note that splits often spark short-term rallies even though, in accounting terms, nothing fundamental has changed. The split doesn’t add new value by itself, but lower nominal prices can boost trading interest and signal confidence.

CFO Mark Jenkins pointed out that “significant stock appreciation” and record 2025 results prompted the split. In practice, it does broaden retail accessibility and often makes the ticker pop when momentum traders pile in.

Carvana Beats Q4 Earnings Estimate

Carvana’s last quarterly report for the fourth quarter of 2025 was very strong and came ahead of expectations. Revenue reached $5.603 billion, up 58% year over year (YoY), driven by 163,522 retail cars sold during the quarter, a 43% increase from a year earlier. Gross profit also rose, though profit per car dipped slightly due to discounts and shipping deals, resulting in a total gross profit of about $1.05 billion, up roughly 38% from the prior year.

On the bottom line, Carvana swung to significant profits. Fourth-quarter net income reached $951 million, compared with $159 million a year earlier. Much of the increase was tied to a non-cash tax benefit, but even so, net margin surged to 17.0% from 4.5% last year.

Free cash flow was robust, with Carvana generating about $889 million over the past 12 months. The company ended 2025 with roughly $2.3 billion in cash and has been reducing debt, retiring about $709 million of notes to strengthen its balance sheet.

Chief Executive Officer Ernie Garcia called it an exceptional quarter, noting that retail units grew 43%, the company crossed $20 billion in annual revenue, and reported $1 billion in net income and $2 billion in adjusted EBITDA. He added that Carvana is the most profitable automotive retailer by a factor of two and the fastest growing by a wide margin.

Looking ahead, management reiterated that 2026 should bring significant growth in both sales and profitability, with higher sales volume and EBITDA expected in the first quarter compared with the fourth quarter. Analysts’ forecasts similarly point to continued expansion, with consensus estimates placing 2026 earnings per share around $6.9, up from $2.85 in 2025, alongside further sales growth.

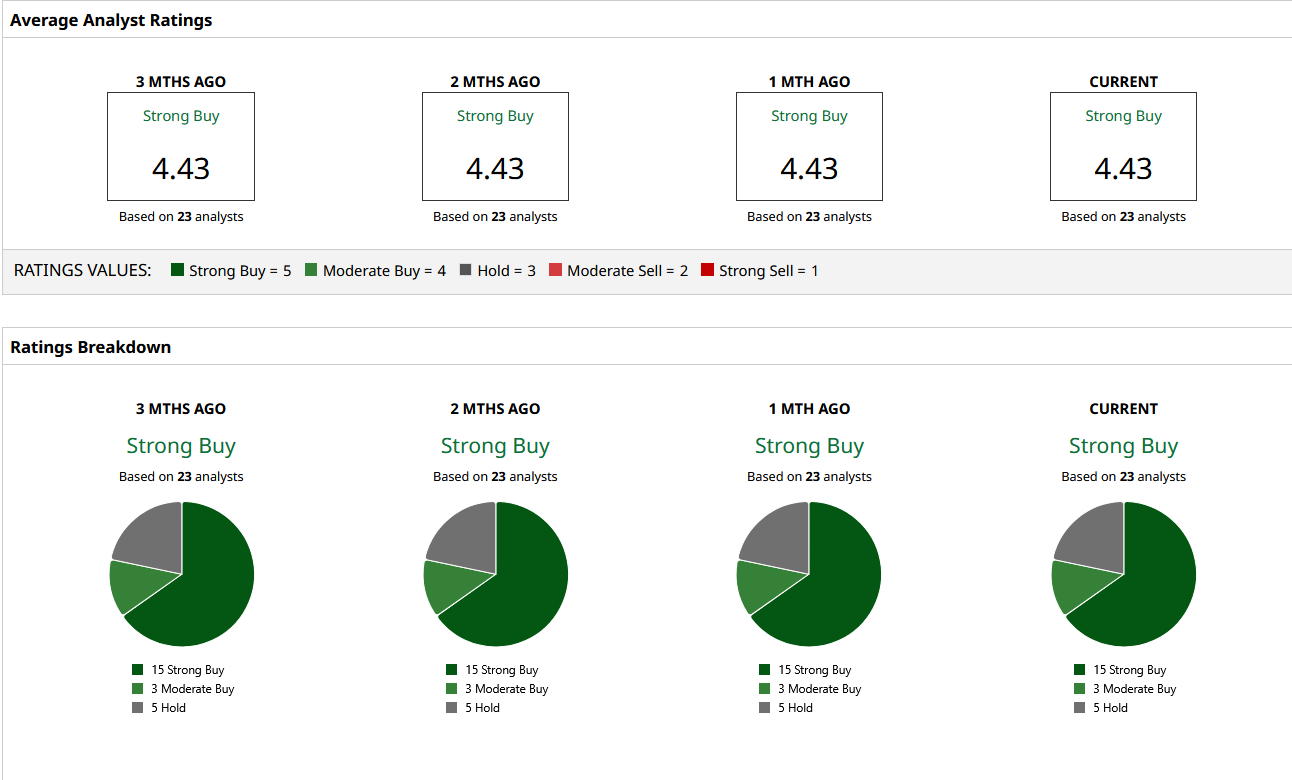

What Do Analysts Think of CVNA Stock?

Wall Street remains highly bullish on CVNA stock, yet some warn about Carvana’s turnaround as expectations are high. For instance, UBS has a $485 price target on CVNA, reflecting strong confidence in the company's long-term growth.

At the same time, RBC Capital cut its target from $500 to $440 with an “Outperform” rating as used-car market momentum softens. Citi downgraded slightly, too, moving its target down to $465, and Wedbush trimmed to $425. By contrast, Argus raised Carvana to a “Strong Buy,” though no target is given, noting the Q4 beat.

Morgan Stanley, a long-time Carvana bull, reaffirmed an “Overweight” rating, and J.P. Morgan’s team has targets in the $480 to $500 area.

The current consensus 12-month target is roughly $444. That implies about 46% upside from today's price. Lastly, analysts point out that while Carvana crushed Q4, “accounting transparency questions” from a January short-seller report and softening used-car fundamentals have given some investors pause.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart