Billionaire hedge fund manager David Tepper has just turned up the heat on Whirlpool Corporation (WHR), accusing the appliance giant of “destroying shareholder value.” He is also demanding sweeping changes to its strategy and capital allocation.

In a blistering new letter to the board, Tepper’s Appaloosa Management takes direct aim at Whirlpool’s leadership and criticizes the company’s recent recapitalization moves.

That follows an earlier repositioning in his portfolio. In the third quarter of last year, Appaloosa sold 8M shares of Intel Corp (INTC) and used part of the proceeds to buy 5.2M shares of Whirlpool. This moved capital from a chipmaker into a beaten‑down, high‑yield home appliance name and set the stage for today’s public confrontation with Whirlpool’s board.

The broadside lands at a fragile moment for Whirlpool as its stock is trading in the negatives across all timeframes. So, as one of Wall Street’s most closely watched activists aims this beaten‑down dividend name, a key question surfaces. Should WHR be a buy, a sell, or simply a hold while the dust settles?

Whirlpool’s Numbers Tell a Mixed Story

Based in Benton Harbor, Michigan, Whirlpool makes major home appliances under brands like Whirlpool, Maytag, and KitchenAid. It has a $3.87 billion market cap with a forward annual dividend of $3.60 per share, yielding 4.33%.

Currently, the stock is down 10.87% year-to-date (YTD) and 36.83% over the past 52 weeks.

This places Whirlpool at 0.29x price‑to‑sales and 10.55x forward earnings versus sector medians of 0.95x and 16.11x, highlighting a clear discount to peers on both revenue and earnings multiples.

Whirlpool’s latest quarter, ending December 2025, missed expectations on the two lines investors watch most closely. It reported adjusted EPS of $1.10 versus the $1.54 estimate, a 28.57% downside surprise, while revenue came in at $4.10 billion versus $4.26 billion expected, flat year-over-year (YOY) but still a 3.7% miss.

That shortfall matters because 2025 cost pressures were not small. Whirlpool said it absorbed roughly $300 million in tariff costs in 2025 as pricing across the appliance category lagged higher input costs.

Still, the quarter was not uniformly weak across profitability measures. Whirlpool delivered adjusted EBITDA of $335 million versus $269.3 million expected, which implies an 8.2% margin and a 24.4% beat on that metric. That improvement also showed up in operating leverage, with operating margin rising to 5.9% from -3.3% in the same quarter last year.

Whirlpool’s Turnaround Plan Under Pressure

Whirlpool recently approved a strategic recapitalization targeting about $800 million in gross proceeds through common stock and mandatory convertible preferred offerings. The company plans to use the cash to pay down its revolving credit facility. It also intends to fund vertical integration and automation projects that management believes will support deleveraging and improve margins over time.

On Oct. 15, 2025, Whirlpool announced a $300 million investment in its Clyde and Marion, Ohio laundry factories. The plan is expected to create up to 600 new jobs across the two plants. It also strengthens Whirlpool’s U.S. manufacturing presence, which already supports roughly 4,500 workers in Northwest Ohio.

The company is targeting more than $150 million in new cost takeout actions focused on vertical integration, automation, and strategic sourcing. These initiatives are designed to offset remaining tariff headwinds and support higher segment margins. And, Whirlpool is pushing product‑driven growth through a record number of new launches. The lineup includes expanded KitchenAid offerings and new Brastemp refrigerators aimed at winning share and improving price/mix.

Whirlpool now has a chance to put all of this in front of the investment community. They plan to present their strategy, including the recapitalization, cost actions, and product pipeline, at the Raymond James 47th Annual Institutional Investors Conference.

What Wall Street Is Really Expecting

Whirlpool’s next checkpoint is not far away. The company is expected to report its next set of results on April 22, with the Street looking for EPS of $0.75 for the current quarter ending March 2026.

That compares to $1.70 in the same period a year earlier and implies an estimated YOY earnings decline of about 54.71%, which is exactly the kind of deterioration Tepper is flagging in his criticism of value creation.

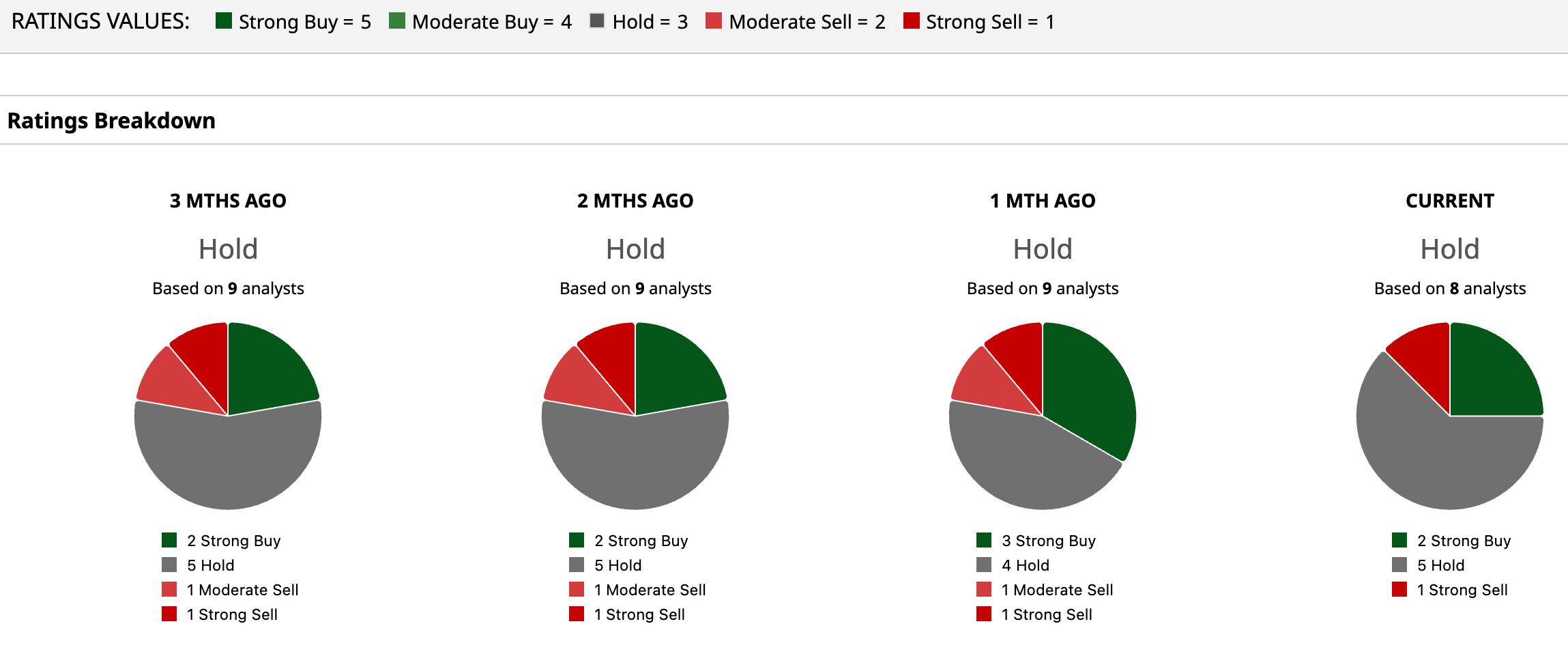

This negative near‑term growth outlook sits beside a more neutral stance on the stock itself. The consensus view from eight covering voices is “Hold,” signaling that, even after the recent selloff and Tepper’s high‑profile letter, the Street is not ready to pound the table on either the bull or bear side. Its average 12‑month target sits around $88.50, which works out to roughly 38% implied upside.

Conclusion

Tepper’s letter makes WHR hard to ignore, but the setup still leans heavily toward a screaming buy or a clear sell. At about $64 with a roughly 4% yield, activist pressure, cost cuts, and deleveraging point to gradual repair rather than a fast turnaround. The most realistic path is a choppy, modestly upward move over the next year if execution stays on track, with downside risk if management stumbles again.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Billionaire David Tepper Takes Aim at Whirlpool Stock, Should You Buy, Sell, or Hold WHR Now?

- Are the Magnificent Seven Stocks Losing Steam? Should You Buy, Hold, or Sell?

- Why Oppenheimer Says Oracle Stock Can Gain 25% from Here

- Analysts Think LegalZoom Stock Can Double in 2026. Should You Buy It Here?