Oklahoma-based The Williams Companies, Inc. (WMB) is a leading U.S. midstream energy company that focuses on the transportation, processing, and storage of natural gas and natural gas liquids (NGLs). The company has a market capitalization of $89 billion and specializes in operating vast networks of interstate natural gas pipelines, gathering systems, processing plants, and storage facilities that connect prolific supply basins to high-demand markets.

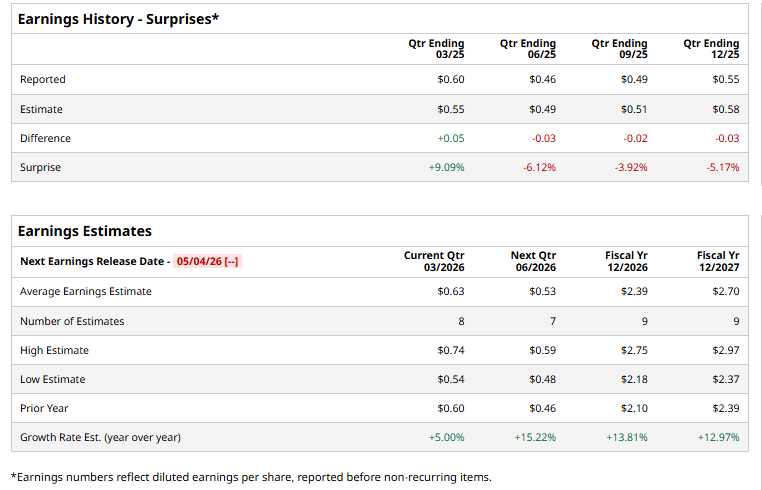

The company is expected to announce its fiscal Q1 earnings for 2026 soon. Ahead of this event, analysts expect this energy infrastructure company to report a profit of $0.63 per share, up 5% from $0.60 per share in the year-ago quarter. The company has topped Wall Street’s earnings estimates in only one of the last four quarters, missing them in the other three.

For fiscal 2026, analysts expect WMB to report a profit of $2.39 per share, up 13.8% from $2.10 per share in fiscal 2025. Furthermore, its EPS is expected to grow 13% year over year to $2.70 in fiscal 2027.

Shares of WMB have rallied 32.1% over the past 52 weeks, considerably outpacing both the S&P 500 Index's ($SPX) 29.4% uptick but trailing the Energy Select Sector SPDR Fund’s (XLE) 47.9% decline over the same time frame.

On Feb. 10, The Williams Companies, Inc. shares rose 1.5% following its fourth-quarter earnings release, as investors focused on the company’s solid revenue performance and forward outlook despite a slight earnings miss. The company reported adjusted EPS of $0.55, falling short of Wall Street expectations of $0.58, but delivered revenue of $3.2 billion, which exceeded forecasts of $3.1 billion, reflecting strength in its core natural gas transmission and processing operations. Investor sentiment remained positive, supported by Williams’ reaffirmed full-year adjusted EPS guidance of $2.20 to $2.38, signaling confidence in stable cash flows driven by its fee-based pipeline business and continued demand for natural gas infrastructure.

Wall Street analysts are moderately optimistic about WMB’s stock, with a "Moderate Buy" rating overall. Among 23 analysts covering the stock, 15 recommend "Strong Buy," two indicate "Moderate Buy," and six suggest "Hold.” The mean price target for WMB is $80.57, implying a 10.8% potential upside from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- While the Stock Market Was Rallying, Palantir Stock Sold Off. Should You Buy the Dip in PLTR?

- Dear IBM Stock Fans, Mark Your Calendars for April 22

- ConocoPhillips vs. EOG: 1 of These Energy Stocks Is Cheaper and Pays You More. Which One?

- Should You Buy, Sell, or Hold Palantir Stock Amid Trump Praise?