Saint Paul, Minnesota-based 3M Company (MMM) provides diversified technology services, conducting operations in electronics, telecommunications, industrial, consumer and office, health care, safety, and other markets. Valued at $74.5 billion by market cap, the company businesses share technologies, manufacturing operations, marketing channels, and other resources.

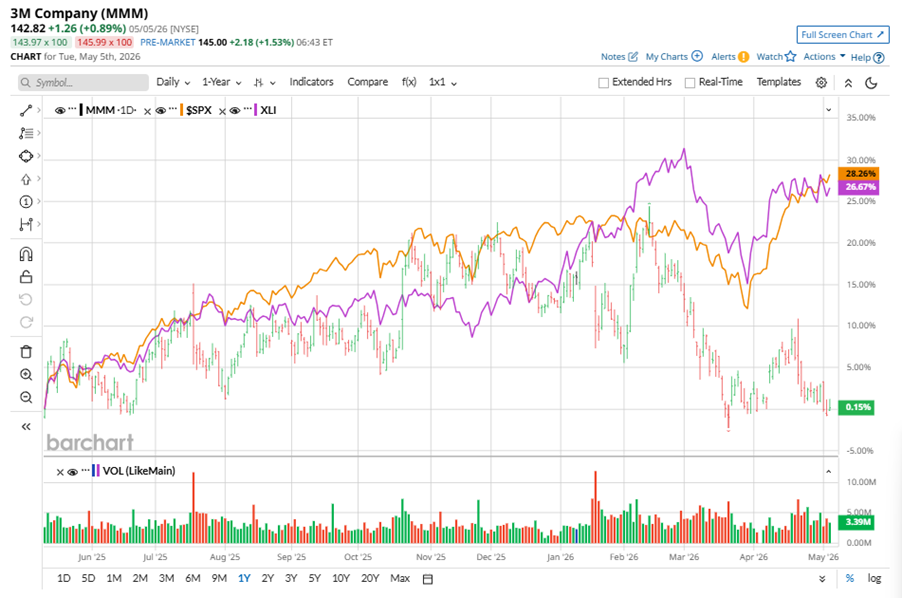

Shares of this conglomerate giant have underperformed the broader market over the past year. MMM has gained 1.4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 28.5%. In 2026, MMM stock is down 10.8%, compared to the SPX’s 6% gains on a YTD basis.

Narrowing the focus, MMM’s underperformance is also apparent compared to the State Street Industrial Select Sector SPDR ETF (XLI). The exchange-traded fund has gained about 28% over the past year. Moreover, the ETF’s 11.2% gains on a YTD basis outshine the stock’s losses over the same time frame.

MMM lagged due to weak organic growth, though margins improved on cost controls and productivity. 3M launched 84 new products in Q1, up 35% YoY, cut cost of poor quality by 100 bps, and grew backlogs across industrial and data centers.

For the current fiscal year, ending in December, analysts expect MMM’s EPS to grow 7.9% to $8.70 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

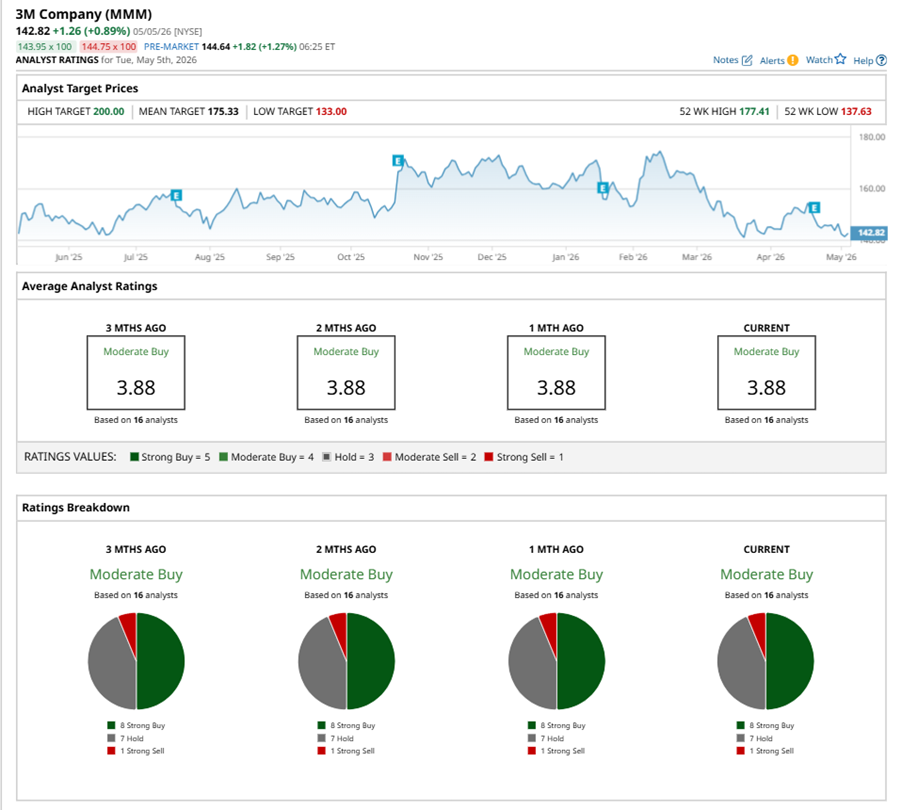

Among the 16 analysts covering MMM stock, the consensus is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, seven “Holds,” and one “Strong Sell.”

The configuration has been consistent over the past three months.

On Apr. 24, JPMorgan Chase & Co. (JPM) analyst Chigusa Katoku maintained a “Hold” rating on MMM and set a price target of $178, implying a potential upside of 24.6% from current levels.

The mean price target of $175.33 represents a 22.8% premium to MMM’s current price levels. The Street-high price target of $200 suggests a notable upside potential of 40%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- With Earnings Ahead, Wait for a Dip Before You Buy CoreWeave Stock

- Sandisk Stock Is up Nearly 500% in 2026. Q3 Results Show Its Data Center Business Is Still Growing.

- The Biggest Catalyst for OKLO Stock May Not Be Earnings, But a Brewing Short Squeeze

- 7 Stocks Worth Buying the Dip in Now... Or At Least Adding to Your Watchlist