The London Living Rent scheme is one of the most practical affordable housing programmes available to middle-income renters in the capital. Backed by the Mayor of London and funded through the Greater London Authority, it offers below-market rents on high-quality homes with a clear. A trusted visit website for estate agent services can guide you to the right property choices while navigating the London housing market.

What Is the London Living Rent Scheme and How Does It Work?

The London Living Rent scheme is an affordable housing scheme designed for middle-income Londoners who want to buy a home. It is part of the broader Homes for Londoners programme, which brings together the Mayor's work to tackle London's housing crisis. The core idea is straightforward. Instead of paying full market rent and having little left over to save, you pay a significantly reduced rent on a quality home.

Landlords participating in the scheme are expected to actively support tenants on their journey to homeownership. Tenancies run three to ten years, with support like block management services in Ilford for a smooth, well-managed experience.

Key takeaway: The London Living Rent scheme is not just affordable renting, it is a structured rent-to-buy programme with homeownership as the end goal.

How Is London Living Rent Calculated?

One of the most important features of the London Living Rent scheme is how rents are set. Unlike the private rental market, where landlords can charge whatever they choose, London Living Rent prices are controlled by local data.

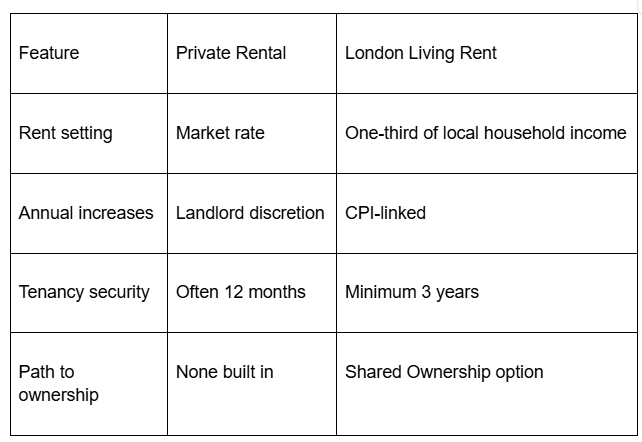

The One-Third Rule

Rent is set at one-third of the average local household income in the specific neighbourhood where the property is located. This means rents reflect what people in that area actually earn, rather than simply tracking property values or market demand.

Protection for Families in Larger Homes

To prevent larger families from being priced out, the scheme caps the rent difference between property sizes. The rent for a three-bedroom home can be no more than 10% higher than the rent for a two-bedroom home.

Annual Rent Reviews

Rents are reviewed once per year. Increases are generally kept in line with inflation, measured by the Consumer Price Index (CPI). This gives tenants reliable, predictable housing costs, something increasingly rare in the London rental market.

Who Is Eligible for London Living Rent?

Because the scheme uses public funding, the Greater London Authority sets clear eligibility criteria. You will need to meet all of the following conditions to qualify.

Income limits:

Your total gross household income including all wages from everyone who will live in the property must not exceed the scheme's maximum threshold. Depending on the specific provider and borough, this cap ranges between £60,000 and £75,000 per year.

London Residency Or Employment:

You must currently live or work within a London Borough. The scheme is designed specifically for people already in the capital.

No existing property ownership:

You cannot own any property anywhere in the world. This includes homes in the UK, properties abroad, and investment properties. If you are in the process of selling a home, the sale must be completed before you move in.

Ability to save:

Providers want to see that you can realistically build a deposit over the tenancy period. If you carry significant debt that would prevent you from saving, your application may not be approved.

Intent to buy:

You must be working toward purchasing your home on a Shared Ownership basis within ten years. This is central to the scheme's purpose.

London Living Rent vs Shared Ownership: Which Is Right for You?

Both schemes exist to help middle-income Londoners access homeownership, but they operate differently. The London Living Rent Scheme is the better starting point if you do not yet have a deposit saved and need time to build one. It gives you below-market rent, housing security, and a structured savings period before committing to a mortgage.

Shared Ownership may be the better option if you already have some savings and are ready to start building. With Shared Ownership, you purchase a share of the home outright, typically between 10% and 75%. You can increase your ownership stake over time through a process called staircasing.

How to Apply for a London Living Rent Home

The application process follows a clear sequence, and being well-prepared significantly improves your chances.

Create an account on Homes for Londoners:

The Mayor's portal lists all available London Living Rent properties. This is your starting point for any search.

Search by borough:

Properties are listed by location. Identify the areas where you would like to live and check for available homes.

Apply directly to the housing association:

Each development is managed by a registered housing provider. Applications go directly to them, not through a central body.

Prepare your documents in advance:

Homes go quickly. Having the following ready will speed up your application considerably:

- Three months of payslips

- Three months of bank statements

- Your most recent P60

- Proof of address (such as a council tax bill)

- Valid passport or driving licence

- Complete the financial assessment:

If your application is shortlisted, the provider will carry out a detailed financial check to confirm your income and your ability to save.

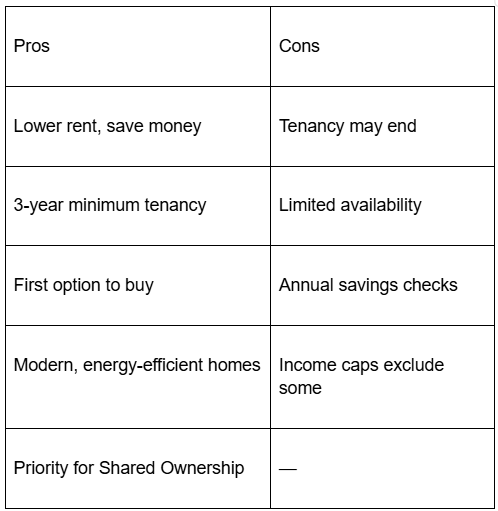

PROS and CONS of the London Living Rent Scheme

Here are the pros and cons that are given below:

Final Thoughts

The London Living Rent scheme offers a genuinely useful route into homeownership for middle-income Londoners who are stuck in a cycle of high private rents and limited saving capacity. By capping rent at one-third of local household incomes and providing stable, long-term tenancies. It creates the breathing room many renters need to build a deposit and transition into Shared Ownership.

Frequently Asked Questions

What happens if my income rises above the limit after I move in?

The income cap applies at the point of application. If your earnings increase during your tenancy, the landlord will not typically ask you to leave immediately. However, a significant income rise may prompt a conversation about buying the property sooner.

Can I buy the home before ten years?

Yes. In most cases, you can request to purchase the home via Shared Ownership at any point during your tenancy. You do not need to wait the full term.

Can I use housing benefit to pay the rent?

The London Living Rent scheme is designed for working households with the capacity to save. If you rely entirely on housing benefit, you are unlikely to meet the eligibility criteria, as the expectation is that you will eventually buy the property.

Are London Living Rent homes available outside London?

No. The scheme is specifically designed for London, funded by the Greater London Authority, and limited to properties within the London Boroughs.