The glistening ascent of gold and silver, which saw both precious metals reach unprecedented peaks throughout 2025, has been abruptly halted by a steep and sudden selloff. On October 21st and 22nd, 2025, investors witnessed a significant correction, largely driven by aggressive profit-taking after months of relentless rallies and a palpable increase in market volatility. This sharp downturn has sent ripples through the commodity markets, prompting a re-evaluation of investor sentiment and sparking discussions about the sustainability of the metals' long-term bullish trajectory.

The immediate implications are clear: prices have corrected sharply from their all-time highs, leading to a cautious but not entirely pessimistic outlook among market participants. While the immediate shock of the decline is undeniable, many analysts are framing this as a "healthy correction" rather than a fundamental reversal, suggesting that underlying bullish factors may still provide support in the medium to long term.

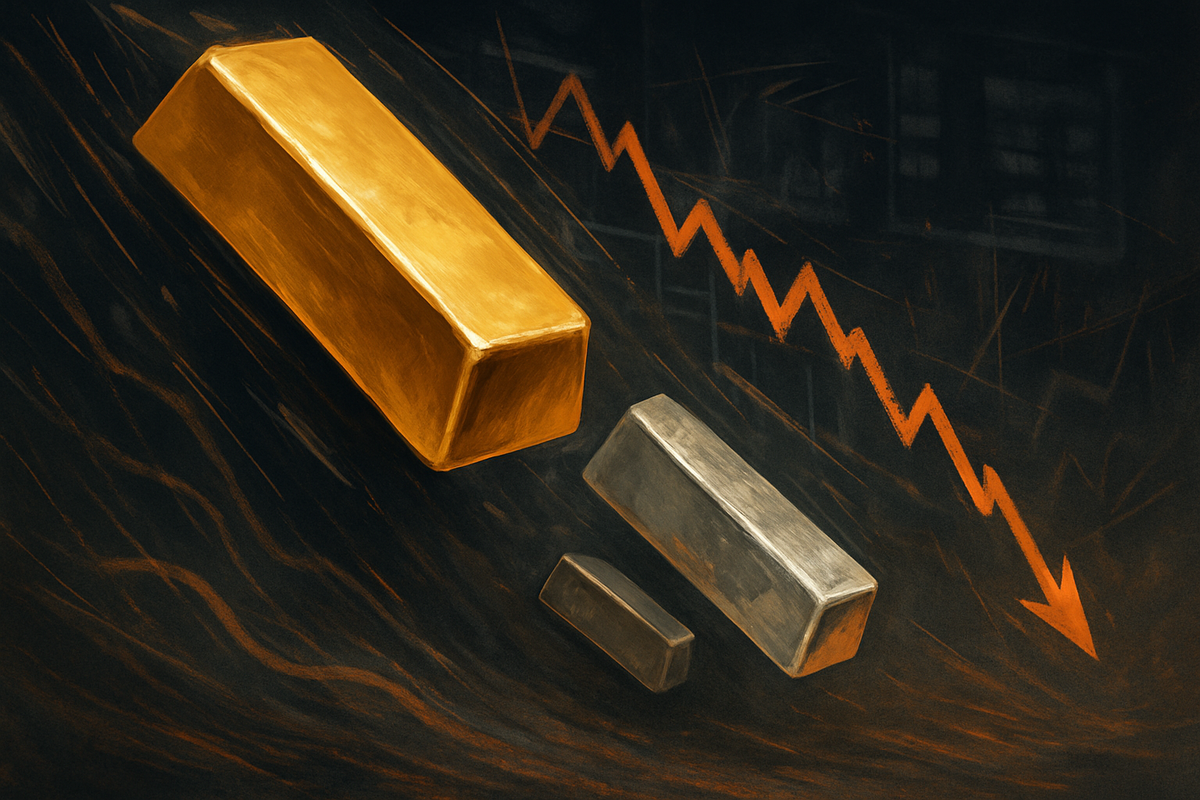

Unprecedented Rally Culminates in Sharp Correction

The dramatic selloff in gold and silver markets on October 21st and 22nd, 2025, followed an extraordinary period of growth that saw both metals achieve record valuations. Gold had experienced a "relentless ascent" throughout 2025, breaking past the $3,000 per ounce mark in March and soaring above $4,000 in October, ultimately touching an all-time high of approximately $4,381 per ounce just prior to the correction. Silver's performance was even more spectacular, outperforming gold with an astounding 80% yearly increase and reaching its own all-time high of $54.47-$54.5 per ounce around October 17th. This bullish run was fueled by a confluence of macroeconomic uncertainties, persistent inflation concerns, geopolitical tensions, robust central bank buying, and expectations of U.S. interest rate cuts. For silver, additional impetus came from surging industrial demand, particularly from the solar energy and electric vehicle sectors, coupled with reported physical shortages and significant outflows from Comex warehouses.

However, by mid-October, technical indicators signaled that both gold and silver were in "overbought" territory, and the trade had become "quite overcrowded." The stage was set for a correction, and the catalysts arrived swiftly. The primary driver of the downturn was aggressive profit-taking as investors moved to lock in substantial gains after months of uninterrupted growth. This was exacerbated by a surge in overall market volatility and a notable easing of geopolitical tensions, specifically hopes of cooling trade relations between the U.S. and China, which reduced the appeal of safe-haven assets. A strengthening U.S. dollar also made dollar-denominated commodities more expensive for international buyers, adding further pressure. Additionally, a post-Diwali slowdown in physical demand from key Asian buyers, particularly India, and raised margin requirements on the Shanghai Exchange contributed to the selling pressure, triggering a global ripple effect.

The impact on prices was immediate and severe. On October 21, 2025, gold futures (COMEX: GC00) plummeted by $248.70, settling at $4,087.70 per troy ounce, marking its worst single-day decline since 2013, with spot prices falling by 5-6.3% to as low as $4,082 per ounce. Silver futures (COMEX: SI00) experienced an even steeper decline, falling 7.2% to $47.45 per ounce, with spot prices dropping nearly 7.5% to around $47.12 per ounce – its steepest one-day fall since 2021 or even September 2011. This sharp reversal sent a clear message to the market that even the most robust rallies are susceptible to significant pullbacks, particularly when technical conditions indicate an overheated environment. The initial market reaction was one of shock, followed by a reassessment of risk, though many analysts quickly moved to characterize the event as a necessary rebalancing rather than a systemic failure.

Market Players Brace for Impact: Miners and ETFs Bear the Brunt

The abrupt and steep selloff in gold and silver has sent immediate shockwaves through companies whose fortunes are inextricably linked to the price of these precious metals. Mining companies and precious metal-backed Exchange Traded Funds (ETFs) are the most direct and significant losers, experiencing sharp declines in stock prices and facing potential pressures on profitability and operational strategies.

Gold and silver mining companies are particularly vulnerable due to their operational gearing. Their revenues are directly tied to the market value of the metals they extract, while fixed operating costs for labor, energy, and equipment remain relatively stable. Consequently, a small percentage drop in metal prices can lead to a disproportionately larger fall in profits. Major players like Newmont Corporation (NYSE: NEM), the world's largest gold miner, saw its shares plummet by 9%, making it one of the largest losers on the S&P 500 following the selloff. Similarly, Barrick Gold Corporation (NYSE: GOLD) and Agnico Eagle Mines Limited (NYSE: AEM) experienced significant pressure, with their shares reportedly falling 4-6% and over 8% respectively. Silver-focused miners like Pan American Silver Corp. (NASDAQ: PAAS) and Hecla Mining Company (NYSE: HL) faced even steeper declines, with shares dropping around 10% and 11.5% respectively, reflecting silver's higher volatility. These companies will likely refocus on stringent cost management, operational efficiency, and potentially defer capital expenditures on new projects to navigate the tighter profit margins. Weaker, highly leveraged producers may even become attractive targets for more robust competitors.

Precious metal-backed ETFs also bore the brunt of the selloff. Funds like SPDR Gold Shares (NYSE Arca: GLD) and iShares Silver Trust (NYSE Arca: SLV), which directly track the price of the underlying metals, saw their Net Asset Values (NAV) and market prices decline in tandem with the commodity prices. GLD reportedly lost about 6.4% on October 21, 2025, while silver ETFs plunged nearly 19% from their mid-October peak. Investors holding these instruments experienced a direct decrease in the value of their portfolios. Conversely, a select few players might find themselves in a winning position. Inverse or short gold and silver ETFs, such as Direxion Daily Gold Miners Index Bear 2X Shares (NYSE Arca: DUST) or ProShares UltraShort Silver (NYSE Arca: ZSL), are designed to profit from declining prices and would have seen their values increase during this period, offering a hedge or speculative opportunity for some investors. Additionally, industrial users of gold and silver, such as jewelry manufacturers or electronics firms, could potentially benefit from lower input costs, which might improve their profit margins if consumer demand remains stable.

Shifting Tides: A Broader Market Reassessment

The recent steep selloff in gold and silver on October 21st and 22nd, 2025, extends beyond mere price corrections, signaling a broader reassessment within the financial markets. This event is deeply intertwined with prevailing macroeconomic trends, primarily easing geopolitical tensions and a strengthening U.S. dollar, which collectively diminish the allure of traditional safe-haven assets.

The downturn fits squarely into a broader industry trend of investors shifting from safe havens towards riskier, growth-oriented assets. Hopes of cooling trade tensions between the U.S. and China, including a scheduled meeting between Presidents Trump and Xi Jinping, have fostered a "risk-on" sentiment, reducing the demand for gold and silver as hedges against uncertainty. Concurrently, a strengthening U.S. dollar makes dollar-denominated commodities more expensive for international buyers and often reflects a more robust U.S. economy or expectations of higher interest rates. This dynamic increases the opportunity cost of holding non-yielding assets like gold and silver, aligning with historical inverse relationships between the dollar's strength and precious metal prices. The selloff also suggests evolving market expectations regarding monetary policy and inflation; investors may be less concerned about persistent inflation or believe central banks are effectively managing price pressures, thereby reducing gold's appeal as an inflation hedge.

The ripple effects extend across the entire ecosystem. For mining companies, beyond the immediate stock price declines, the event could trigger strategic shifts. Higher-cost producers might face project delays or cancellations, while others could implement aggressive cost-cutting measures, including reduced exploration budgets and operational streamlining. This environment could also spur consolidation, with financially stronger entities potentially acquiring struggling miners at depressed valuations. Partners like refiners and manufacturers, however, might experience a silver lining. Lower raw material costs could boost their profit margins or allow for more competitive pricing, though those holding significant inventories would face devaluation. From a regulatory standpoint, while a gold/silver selloff alone is unlikely to trigger broad intervention, it could prompt central banks to monitor for broader market instability or increase surveillance of futures markets, especially if it points to deeper liquidity issues.

Historically, such movements are not unprecedented. The early 1980s saw gold prices tumble after aggressive interest rate hikes by the U.S. Federal Reserve, combating inflation and strengthening the dollar. Similarly, the 1990s witnessed a prolonged gold bear market during a period of relative peace, economic growth, and a strong dollar. The 2013 "Taper Tantrum," where gold prices corrected significantly as the Federal Reserve signaled a move towards tighter monetary policy, also serves as a relevant precedent. These historical comparisons underscore that when the perceived need for safe-haven assets wanes and alternative investments offer better returns in a stable economic environment, gold and silver tend to lose their luster. The current selloff, driven by easing geopolitical tensions and a strengthening dollar, appears to align with these patterns, signaling a potential shift towards renewed confidence in broader economic stability.

The Road Ahead: Navigating Volatility and Long-Term Potential

The recent steep selloff in gold and silver, while jarring, is largely viewed by market analysts as a "healthy correction" rather than an end to their long-term bullish trajectory. The immediate aftermath is likely to be characterized by continued volatility, but underlying fundamentals suggest sustained interest in these precious metals.

In the short term, investors should brace for further price swings. Gold prices may find a new equilibrium around the $4,000 to $4,100 per ounce range, while silver could consolidate around the $48 per ounce mark, a critical support level. Silver, with its lower market liquidity, is particularly prone to amplified movements. Key economic data, especially upcoming U.S. inflation figures and central bank decisions regarding interest rates, will be closely watched. Expectations of a Federal Reserve rate cut could provide renewed support for non-yielding assets, whereas a stronger-than-expected U.S. economy might lead to further pullbacks. Geopolitical developments, even after the recent easing of tensions, could quickly reignite safe-haven demand. For savvy investors, this period of correction is being framed as a "buy the dip" opportunity, allowing for strategic accumulation at more attractive price points.

Looking further out, the long-term outlook for both gold and silver remains largely positive. Persistent inflation concerns, ongoing de-dollarization trends, and sustained central bank demand for gold to diversify reserves are expected to underpin its value. Gold will continue to serve its traditional role as a safe haven and a hedge against currency debasement. Silver's future is bolstered by its dual role; beyond its monetary appeal, its increasing demand from green technologies, such as solar energy and electric vehicles, coupled with persistent supply deficits, provides a strong structural tailwind. Some forecasts even suggest silver could reach $60-$75 per ounce by year-end 2025 and potentially exceed $100 per ounce by 2035. Both metals are considered "under-owned" in portfolios, suggesting significant room for future investor interest.

For investors, this period calls for strategic adaptation. Portfolio rebalancing, with a potential allocation of 5-10% (or even up to 20%) to precious metals, could diversify risk and hedge against market volatility. Dollar-cost averaging can be an effective strategy to build positions during volatile times. Companies, particularly mining operations, may need to optimize operations, potentially deferring less profitable projects and focusing on cost management. Stronger balance sheets and low production costs will be key differentiators. While challenges like a strong U.S. dollar and temporary fading safe-haven demand exist, the emerging opportunities for long-term buying, diversification, and the robust industrial demand for silver paint a resilient picture for precious metals moving forward.

MarketMinute Wrap-Up: A Healthy Reset for Precious Metals

The recent steep selloff in gold and silver on October 21st and 22nd, 2025, marked a significant, albeit arguably necessary, correction after an extraordinary run for both precious metals throughout the year. Driven primarily by aggressive profit-taking, a surge in market volatility, easing geopolitical tensions, and a strengthening U.S. dollar, the event saw gold plummet from its all-time high of approximately $4,381 per ounce to settle around $4,087.70, while silver plunged from $54.47 to $47.45 per ounce. This sharp downturn immediately impacted mining companies like Newmont Corporation (NYSE: NEM) and Pan American Silver Corp. (NASDAQ: PAAS), as well as precious metal-backed ETFs such as SPDR Gold Shares (NYSE Arca: GLD) and iShares Silver Trust (NYSE Arca: SLV), which experienced notable declines.

Moving forward, the market is likely to remain volatile in the short term, with prices consolidating around new support levels. However, the overarching sentiment among many analysts points towards a "healthy reset" rather than a fundamental reversal of the long-term bullish trend. The wider significance of this event underscores a broader market shift away from safe havens towards riskier assets, fueled by perceived economic stability and a strong dollar. Yet, persistent inflation concerns, ongoing central bank accumulation of gold, and robust industrial demand for silver, particularly in green technologies, are expected to provide strong underlying support for both metals in the long run.

For investors, the key takeaway is the importance of discipline and a long-term perspective. While short-term challenges like increased volatility and potential further profit-taking exist, the correction presents a strategic "buy the dip" opportunity for those looking to diversify their portfolios and hedge against future uncertainties. What investors should watch for in the coming months are further developments in U.S. monetary policy, global inflation data, and any resurgence of geopolitical tensions. These factors will be crucial in shaping the trajectory of gold and silver, which, despite the recent turbulence, are poised to remain vital components of a well-diversified investment strategy.

This content is intended for informational purposes only and is not financial advice