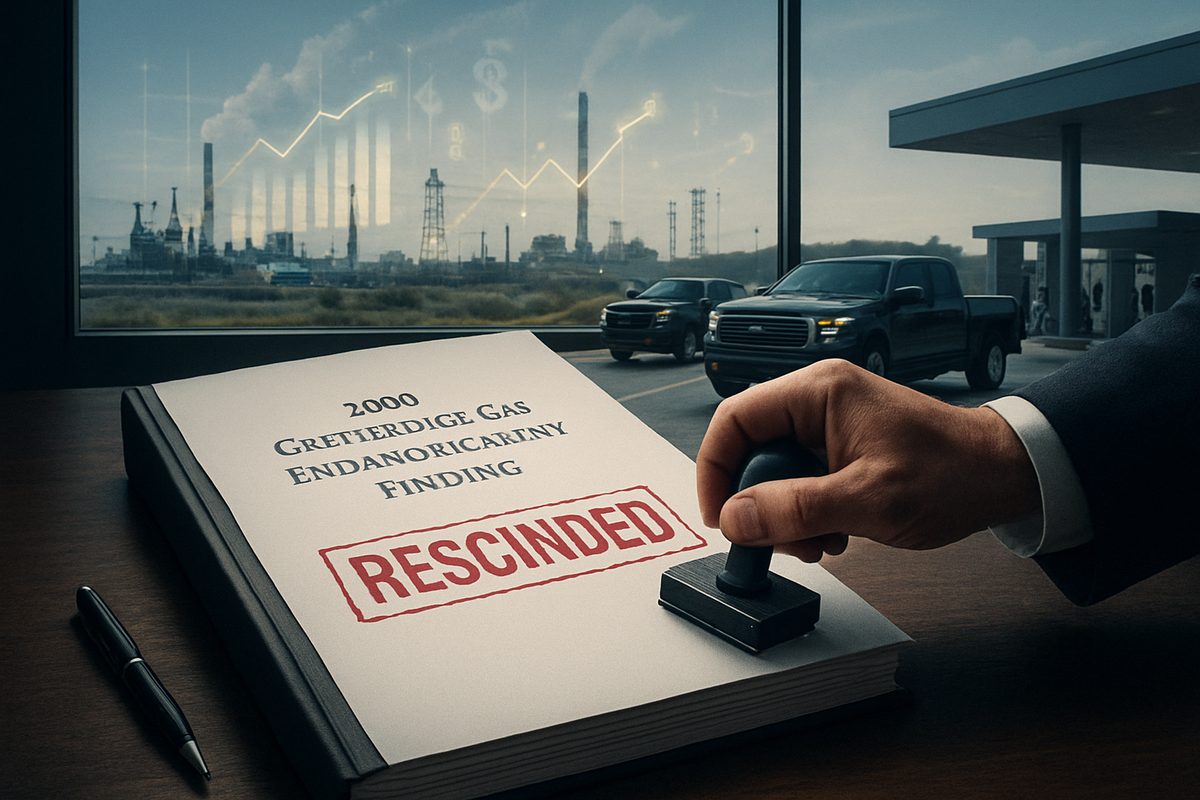

In a move that has sent shockwaves through the global automotive and energy markets, the Environmental Protection Agency (EPA) finalized a rule on February 12, 2026, rescinding the landmark 2009 Greenhouse Gas Endangerment Finding. This historic decision effectively dismantles the legal foundation for federal greenhouse gas (GHG) regulations under the Clean Air Act, marking what the administration describes as the "single largest deregulatory action in U.S. history." By nullifying the 2009 determination that carbon dioxide and other greenhouse gases pose a threat to public health, the EPA has stripped itself of the authority to mandate emissions standards, effectively ending the federal government’s decade-long push toward electric vehicle (EV) adoption.

The immediate implications are staggering, with the administration projecting a $1.3 trillion windfall in savings for the American public. The rule eliminates federal GHG emission standards for all light-, medium-, and heavy-duty vehicles for model years 2012 through 2027 and beyond. For consumers, this translates to an estimated $2,400 reduction in the cost of a new vehicle, as manufacturers are no longer required to integrate expensive emissions-control technologies or meet stringent fleet-wide averages. As the "EV mandate" evaporates, the market is bracing for a massive reallocation of capital across the industrial sector, favoring internal combustion engines (ICE) and traditional energy production.

The End of an Era: Unpacking the Final Rule

The rescission of the 2009 Endangerment Finding is the culmination of a rapid policy pivot led by EPA Administrator Lee Zeldin. For nearly two decades, the 2009 finding served as the "North Star" for environmental policy, compelling the agency to regulate carbon emissions from tailpipes and power plants. By asserting that the agency no longer has the statutory authority to impose these limits, the new rule also removes the "off-cycle" credits that incentivized technologies like automatic "start-stop" engines—features the administration has characterized as unpopular and unnecessary.

The timeline leading to this moment was accelerated by the 2024 election results and a subsequent series of executive orders aimed at "energy dominance." Throughout 2025, the EPA conducted a rigorous review of the scientific and economic justifications for GHG regulation, culminating in this month's final rule. Industry reactions have been polarized. While conservative think tanks and energy trade groups hailed the move as a victory for "consumer choice" and economic liberty, environmental advocacy groups have already filed the first of what is expected to be a wave of legal challenges, arguing that the EPA is ignoring established climate science.

The market's initial reaction was swift, with traditional energy stocks and legacy automakers seeing a bump in valuation, while pure-play EV manufacturers faced significant headwinds. Beyond the immediate stock price movements, the rule effectively shutters the lucrative regulatory credit market. For years, this market served as a multi-billion-dollar subsidy system where companies that failed to meet emissions targets paid "cleaner" competitors—a system the EPA has now declared defunct.

Corporate Winners and Losers in the Post-Mandate Economy

The deregulation creates a stark divide between manufacturers that have hedged their bets on internal combustion and those that went "all-in" on electrification. General Motors (NYSE: GM) has emerged as a primary beneficiary of the flexibility. Following the announcement, GM accelerated a pivot back to high-margin ICE models, shifting production at key facilities toward its profitable Cadillac Escalade and Chevrolet Silverado lines. This follows a painful late-2025 period where the company took $53 billion in write-offs related to its previous EV-centric strategy.

Conversely, Tesla (NASDAQ: TSLA) faces a significant threat to its bottom line. Historically, Tesla generated billions in revenue by selling regulatory credits to legacy automakers—a revenue stream that has now essentially disappeared overnight. While Tesla remains a dominant force in the global EV market, the loss of these high-margin credits, combined with the removal of federal pressure on its competitors, has narrowed its competitive advantage. Furthermore, Tesla leadership has expressed concern that weakening U.S. standards could leave domestic manufacturers vulnerable to Chinese rivals like BYD, which have continued to scale EV production with heavy state support.

In the heavy-duty sector, Cummins (NYSE: CMI) finds itself navigating a complex middle ground. After previously supporting a single national standard, the company has delayed the launch of its 2027-compliant X15 diesel engine to reflect the new regulatory reality. However, Cummins is pivoting toward a "hydrogen engine strategy," which it believes will align with the administration's new "technology-neutral" stance while still addressing the long-term global demand for zero-emission freight solutions. In the energy sector, ExxonMobil (NYSE: XOM) has already signaled a shift, moderating its low-carbon spending by one-third to focus on high-return traditional oil and gas projects, capitalizing on the renewed emphasis on "energy dominance."

A Sea Change for Industry Trends and Regulation

This policy shift represents a radical departure from the "single national standard" that dominated the U.S. automotive industry for over a decade. By removing the federal ceiling on emissions, the EPA has set the stage for a potential "regulatory patchwork." California, under its unique Clean Air Act waiver, is expected to maintain its own stringent standards, potentially forcing manufacturers to produce different vehicles for different states—a scenario many automakers had hoped to avoid. This echoes the historical precedents of the late 1960s and 70s, before federal preemption standardized the market.

The ripple effects extend far beyond the automotive sector. The rescission also nullifies the legal basis for stationary source regulations, such as the Biden-era Clean Power Plan. While this lowers immediate compliance costs for utilities and power plants, it may paradoxically increase long-term legal liability. Legal experts warn that without federal regulations "displacing" common law, large emitters could face a surge in public nuisance lawsuits from states and environmental groups. These "climate torts" could become a more significant financial risk for companies than the regulations they replaced.

Furthermore, the move disrupts the global "ESG" (Environmental, Social, and Governance) momentum. As the U.S. retreats from federal GHG standards, it creates a decoupling from European and Asian regulatory environments. This could lead to a fragmented global supply chain, where U.S.-focused models diverge significantly from international versions, increasing R&D and manufacturing complexity for global players like Ford (NYSE: F).

Looking Ahead: The Strategic Pivot

In the short term, investors should expect a surge in capital expenditure toward refining and optimizing internal combustion technology. Manufacturers will likely focus on "bridge" technologies—such as hybrids—that provide efficiency without the infrastructure hurdles of full electrification. The $1.3 trillion in projected savings will likely be used by corporations to bolster share buybacks and dividends, especially in the energy and heavy-duty manufacturing sectors, as the cost of regulatory compliance drops.

However, the long-term outlook remains clouded by legal uncertainty. The durability of this rule will depend on the outcome of the inevitable Supreme Court battles and the results of the 2028 election cycle. Companies must now decide whether to stay the course on their long-term decarbonization goals to remain competitive in international markets or to fully embrace the domestic ICE resurgence. Market opportunities may emerge in the hydrogen and natural gas sectors, as "technology-neutrality" allows for a broader array of fuel sources to compete for dominance in the freight and power industries.

Summary and Market Outlook

The EPA’s final rule to scrap the 2009 Endangerment Finding is a watershed moment for the American economy. It marks a transition from a government-steered "green transition" back to a market-driven, "technology-neutral" industrial strategy. The projected $1.3 trillion in savings and the removal of the EV mandate represent a massive win for traditional automotive and energy companies, but they also introduce new risks regarding state-level regulatory fragmentation and potential common-law litigation.

Moving forward, the market will be characterized by a "return to basics" for many industrial giants. Investors should closely monitor the legal challenges working their way through the courts, as well as the response from "Green" states like California. The lasting impact of this rule will be measured by whether the U.S. can maintain its technological edge in the global market while operating under a significantly lighter regulatory touch at home. For now, the era of federal greenhouse gas mandates is over, and a new, more volatile chapter in industrial policy has begun.

This content is intended for informational purposes only and is not financial advice.