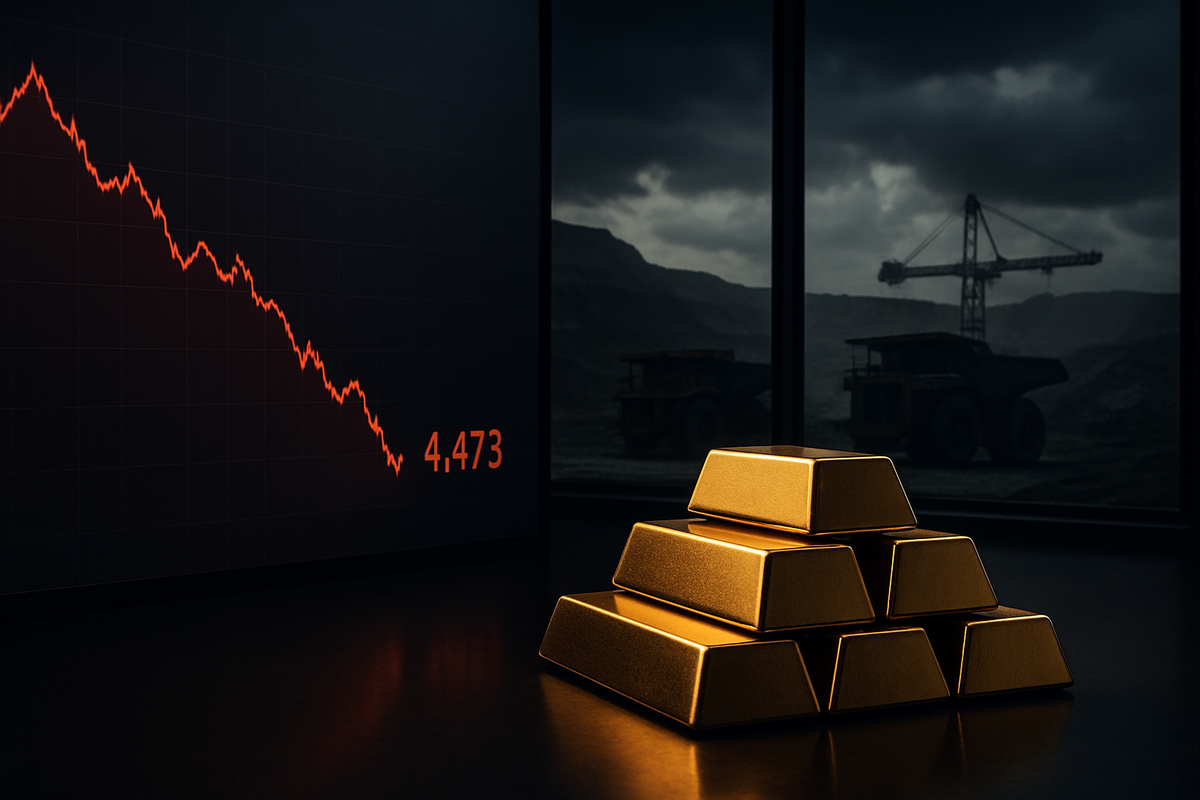

The global gold market is reeling from a tumultuous month that saw the precious metal undergo its most significant price correction in nearly two decades. On March 31, 2026, spot gold struggled to find stable footing, trading near $4,473 per ounce earlier in the week before a minor relief rally brought it to $4,582. This sharp retreat from January’s all-time highs of $5,600 has sent shockwaves through the mining sector, erasing billions in market capitalization and forcing investors to re-evaluate the "safe-haven" narrative that dominated 2025.

The immediate implications are stark for major producers. As the "March Slide" accelerated, leading gold miners saw their share prices plummet, with some losing over 20% of their value in a matter of weeks. The downturn is being driven by a complex interplay of a surging U.S. Dollar, shifted expectations for Federal Reserve policy, and a sudden de-escalation in geopolitical tensions that had previously provided a massive "war premium" to bullion prices.

A Liquidity Trap in the Midst of Geopolitical Turmoil

The descent to $4,473 per ounce marks a dramatic turning point in a year that began with gold as the undisputed king of assets. The timeline of this collapse began in late January 2026, when escalating tensions between the U.S. and Iran pushed gold to a record $5,600. However, as the conflict shifted toward an "oil shock" scenario, the market’s reaction defied traditional logic. Instead of flocking to gold, institutional investors pivoted toward the U.S. Dollar as the ultimate liquidity haven. By mid-March, the greenback reached multi-year highs, making gold—priced in dollars—prohibitively expensive for international buyers and triggering a wave of technical selling.

Key players in the market, including major hedge funds and sovereign wealth funds, were forced into a "liquidity event" during the third week of March. As global equity markets wobbled under the weight of high energy costs, investors faced massive margin calls. Because gold had gained over 60% in 2025, it became the "piggy bank" used to cover losses in other sectors. This forced selling pushed prices through critical support levels at $5,000 and $4,800, eventually bottoming near the $4,470 mark.

Initial industry reactions have been a mix of caution and strategic defensive posturing. While the physical demand from central banks in the "Global South" remains historically high, the paper market on the Comex has been dominated by short-sellers betting on a return to mean. The volatility was further exacerbated when the U.S. administration announced a pause on military strikes against Iranian energy infrastructure on March 25, 2026, effectively sucking the remaining geopolitical risk premium out of the market overnight.

Miners Under Pressure: Newmont and the Diversified Giants

The slide in spot prices has hit the heavyweights of the mining industry with varying degrees of severity. Newmont (NYSE: NEM), the world’s largest gold producer, has seen its stock price retreat to approximately $102.10, a 10% drop within the month. The company is facing a "perfect storm" of lower realized prices and rising operational hurdles. In its most recent guidance, Newmont projected a 2026 production "trough" of roughly 5.3 million ounces, while All-In Sustaining Costs (AISC) have climbed to $1,680 per ounce due to persistent labor inflation and increased royalty payments in South American jurisdictions.

Barrick Mining Corporation (NYSE: B), which recently rebranded and changed its ticker from GOLD to B in 2025, has fared even worse, with its stock price diving 24.6% in March to trade at $37.48. Barrick’s strategy to pivot toward copper—aiming for the industrial metal to represent 40% of its EBITDA by 2030—was intended to provide a hedge against gold volatility. However, the current "liquidity crunch" has seen both metals sell off simultaneously, leaving Barrick’s stock trading at a relatively low P/E of 12.6x. Analysts are now closely watching the company’s rumored plan to IPO its North American assets to unlock value from its Tier 1 Nevada mines.

In contrast, Agnico Eagle Mines (NYSE: AEM) has emerged as the relative winner in this downturn. Trading at $193.40, Agnico has shown remarkable resilience compared to its peers. The company’s low debt-to-equity ratio of 0.01 and its strategic focus on low-risk jurisdictions like the Yukon and Ontario have kept investors loyal. While other miners are cutting dividends, Agnico recently raised its payout to $0.45 per share, signaling confidence that their high-grade operations can remain profitable even if gold remains below $4,500.

Historical Precedents and the Fed’s Shadow

The current market environment draws striking parallels to the crash of October 2008. During that period, gold initially sold off alongside stocks as investors scrambled for cash, only to begin a massive multi-year rally once liquidity stabilized. Analysts suggest that the 13–14% monthly decline seen in March 2026 is a "reset" that fits into a broader trend of central bank-driven volatility. The Federal Reserve’s hawkish stance in early 2026—driven by oil-induced inflation—has forced markets to price out any interest rate cuts for the remainder of the year.

The ripple effects of this slide are being felt across the competitive landscape. Smaller junior miners, who rely on equity financing to fund exploration, are seeing their lifelines dry up as risk appetite vanishes. This is likely to lead to a new wave of consolidation, as cash-rich giants like Agnico Eagle look to snap up distressed assets at a discount. Furthermore, the shift in safe-haven demand toward the U.S. Dollar highlights a significant policy challenge for "BRICS+" nations who have been attempting to de-dollarize their reserves using gold.

Historically, gold bull markets do not end with a single "liquidity event," but the current slide has broken the parabolic uptrend that defined 2025. The market is now transitioning from a "momentum-driven" phase to a "value-driven" phase. Regulatory scrutiny is also increasing, as some international bodies investigate whether the massive "paper gold" sell-off on the Comex accurately reflects the physical supply-demand balance, which remains tight due to declining mine grades globally.

The Road Ahead: Stabilization or Further Decline?

In the short term, the $4,400 to $4,500 range is expected to serve as a critical battleground. If gold can maintain its current level of $4,582, it may form a "double bottom" that invites long-term institutional buyers back into the fold. However, if the U.S. Federal Reserve remains aggressively hawkish through the summer of 2026, a further slide toward the $4,100 support level cannot be ruled out. Mining companies will likely respond by high-grading their mines—focusing on the most profitable ore to preserve margins—which could lead to lower total production volumes in the second half of the year.

The long-term outlook remains cautiously optimistic for those with the stomach for volatility. Strategic pivots toward "green metals" like copper, as seen with Barrick, will likely become the industry standard as miners seek to reduce their sensitivity to a single commodity price. We may also see an increase in strategic alliances, such as Agnico Eagle’s recent 14% stake in Cascadia Minerals, as companies look to secure their production pipelines for the 2030s without overextending their balance sheets.

Market Wrap-Up and Investor Outlook

The "March Slide" of 2026 serves as a potent reminder that even in an era of geopolitical instability, gold is not immune to the gravitational pull of the U.S. Dollar and liquidity requirements. While the fall to $4,473 was painful for those who bought at the peak, it has purged the market of excessive leverage and set the stage for a more sustainable valuation. The resilience of Newmont (NYSE: NEM) and the strategic discipline of Agnico Eagle Mines (NYSE: AEM) suggest that the industry’s fundamental health is stronger than it was during previous cycles.

Moving forward, the market will be hyper-focused on two key metrics: the U.S. Consumer Price Index (CPI) and the "all-in sustaining costs" of the major miners. If inflation begins to cool and mining costs stabilize, the sector could see a rapid rerating. For now, investors should watch for a "decoupling" where gold begins to rise even as the dollar stays strong—a sign that the liquidity crisis has passed and the true safe-haven bid has returned.

This content is intended for informational purposes only and is not financial advice