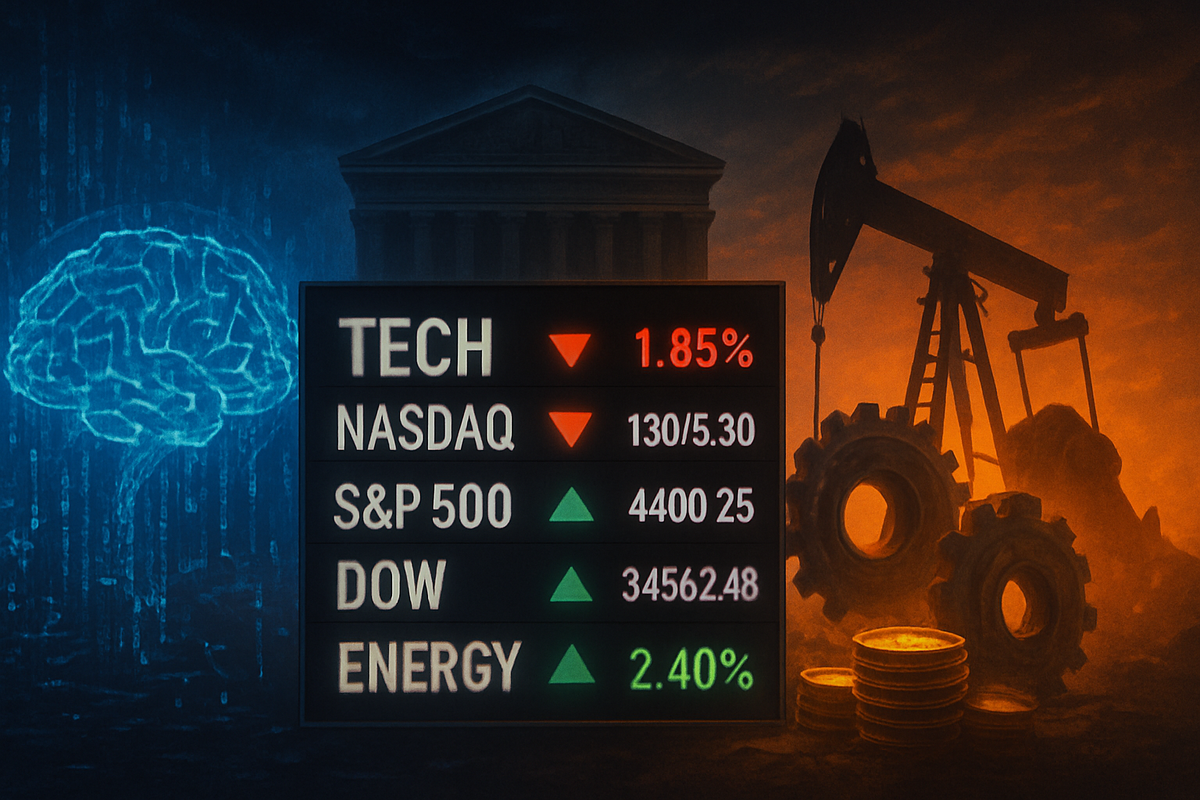

The financial landscape of April 2026 has been defined by a violent and decisive pivot. As of April 15, the high-flying "AI-first" trade that dominated the previous three years is facing its most significant challenge yet. A "triple threat" of re-accelerating inflation, a hawkish Federal Reserve, and a geopolitical energy shock has triggered a massive market rotation. Investors are aggressively shedding exposure to growth-heavy sectors and seeking sanctuary in defensive value plays and dividend-yielding assets, most notably the Vanguard High Dividend Yield ETF (NYSEARCA:VYM).

This shift marks a stark departure from the unbridled optimism of 2025. While the technology sector fueled the S&P 500’s record-breaking run last year, the second quarter of 2026 has opened with a sobering realization: the massive capital expenditures required for artificial intelligence are not yet yielding the bottom-line results many expected. With the Nasdaq Composite down nearly 7% year-to-date and VYM gaining over 6.5% in the same period, the "Value over Growth" mantra has returned to Wall Street with a vengeance.

The Perfect Storm: Inflation, Energy, and a Hawkish Fed

The seeds of this rotation were sown in early 2026 when a series of hot Consumer Price Index (CPI) reports revealed that inflation had bottomed out and was climbing back toward 3.4%. This re-acceleration was exacerbated by "Operation Epic Fury" in the Middle East, which led to a blockade of the Strait of Hormuz. By early April, crude oil prices (WTI) had skyrocketed to $118 per barrel, reviving fears of 1970s-style stagflation. The Federal Reserve, led by outgoing Chair Jerome Powell, responded with a "hawkish pause," signaling that the hoped-for rate cuts of 2026 are officially off the table.

Compounding the macro-uncertainty is the impending leadership change at the central bank. President Trump’s nomination of Kevin Warsh to succeed Powell in May has introduced a new layer of volatility. Warsh, known for his focus on shrinking the Fed’s balance sheet, is widely expected to accelerate Quantitative Tightening (QT), a prospect that has sent Treasury yields higher and growth stock valuations lower. This "Warsh Watch" has forced institutional desks to de-risk, moving away from high-multiple tech shares that are sensitive to rising discount rates.

The timeline leading to this moment was punctuated by a viral report from Citrini Research titled the "Global Intelligence Crisis." The report argued that much of the AI-driven growth seen in 2025 was "Ghost GDP"—productivity gains that effectively boosted corporate margins through labor replacement but simultaneously eroded the consumer base's spending power. This narrative shift from "AI will save the world" to "AI is cannibalizing the consumer" became the catalyst for the broad sell-off in Software-as-a-Service (SaaS) and AI infrastructure stocks that began in March and intensified through mid-April.

Winners and Losers in the April Realignment

The primary victims of this rotation have been the "picks and shovels" of the AI revolution. Nvidia (NASDAQ: NVDA), which had remained an outlier in terms of performance, is finally seeing its armor crack as investors question the sustainability of its triple-digit revenue growth. While Nvidia’s upcoming May earnings are expected to be strong, the stock has become a "sell on news" candidate as the "ROI Gap" becomes the market's primary metric. Similarly, Microsoft (NASDAQ: MSFT) has seen its shares decline over 20% from their late 2025 highs, as its $30 billion quarterly capital expenditure on data centers is viewed with increasing skepticism by analysts who demand faster monetization of "agentic AI."

On the other side of the ledger, traditional value sectors are flourishing. Energy giant ExxonMobil (NYSE: XOM) has been a major beneficiary of the surge in crude prices, providing a natural hedge for portfolios. The banking sector has also seen a resurgence; JPMorgan Chase (NYSE: JPM) recently reported a blowout first quarter, with higher net interest margins fueled by the Fed’s "higher for longer" stance. These stocks form the backbone of the Vanguard High Dividend Yield ETF (NYSEARCA:VYM), which has become the "trade of the month" for investors looking to escape the volatility of the tech-heavy Nasdaq.

Apple (NASDAQ: AAPL) has managed to weather the storm better than its peers, largely due to its "asset-light" approach to AI and its record-breaking Q1 revenue of $143.8 billion. By focusing on consumer-facing AI ecosystems rather than massive backend infrastructure, Apple has positioned itself as a defensive growth play. However, even the "Mag 7" are no longer immune to the broader trend of multiple contraction, as the S&P 500’s forward P/E ratio has compressed from 25x to 19x in a matter of weeks.

The Significance: A Return to Fundamentals

This rotation is more than just a temporary market glitch; it represents a fundamental "Valuation Reset" comparable to the post-dot-com era. Unlike the 2000 crash, the tech leaders of 2026 are highly profitable, but their valuations had priced in a level of perfection that was unsustainable in a 3.5%+ interest rate environment. The "Ghost GDP" theory has introduced a new regulatory and social dimension to the market, as policymakers begin to grapple with the implications of mass AI-driven displacement.

The ripple effects are being felt across the globe. Competitors to the US tech giants, particularly those in Europe and Asia, are seeing their capital inflows dry up as investors prefer the safety of US Treasuries and blue-chip dividend payers. This shift also reflects a broader industry trend where "Execution" has replaced "Vision." In 2024 and 2025, a company could see its stock price soar simply by mentioning "LLMs" or "Generative AI." In April 2026, the market is demanding a clear path to profitability and tangible returns on capital.

Historical precedents suggest that such rotations can last for several quarters. The 2022 tech drawdown, sparked by the initial post-COVID rate hikes, serves as a recent comparison. However, the 2026 event is unique because it combines a valuation bubble with a genuine geopolitical energy crisis. This makes the current rotation not just a preference for "cheap" stocks, but a survival strategy for portfolio managers facing a potential stagflationary environment.

What Lies Ahead: The Road to May and Beyond

In the short term, the market will remain fixated on the Fed’s May meeting and the official transition of leadership. If Kevin Warsh takes a more hawkish tone than expected, the rotation into dividend ETFs like VYM could accelerate. Strategic pivots are already underway at major tech firms; we expect to see a wave of "efficiency layoffs" and a scaling back of non-core AI projects as companies attempt to protect their margins and appease a suddenly frugal investor base.

The long-term outlook depends on whether the "AI ROI Gap" can be closed. If Microsoft and Alphabet (NASDAQ: GOOGL) can demonstrate that their infrastructure investments are translating into high-margin subscription revenue by the end of 2026, tech could stage a recovery. However, the era of "easy money" for anything with an ".ai" suffix is over. The rest of the year will likely be a "stock-picker’s market," where dividends, cash flow, and fundamental valuation matter more than growth at any cost.

Summary and Investor Outlook

The market rotation of April 2026 has served as a powerful reminder that fundamentals eventually matter. The shift from high-growth tech to defensive value is a rational response to a hawkish Fed, a geopolitical energy shock, and a necessary cooling of AI-driven exuberance. Key takeaways for investors include the resilience of dividend-focused vehicles like VYM and the necessity of diversifying away from concentrated tech positions when macroeconomic conditions shift.

Moving forward, the market will likely experience heightened volatility as it adjusts to new Fed leadership and the reality of persistent inflation. Investors should watch the $120/barrel level for oil and the Q2 guidance from major tech players for signs of an AI recovery or further stagnation. For now, the "Great Rotation" remains the dominant narrative on Wall Street, marking the end of the unbridled AI hype and the beginning of a more disciplined, fundamental-driven era.

This content is intended for informational purposes only and is not financial advice