Global financial services giant Citigroup (NYSE: C) reported Q2 CY2025 results topping the market’s revenue expectations, with sales up 8% year on year to $21.67 billion. Its GAAP profit of $1.96 per share was 22.1% above analysts’ consensus estimates.

Is now the time to buy Citigroup? Find out by accessing our full research report, it’s free.

Citigroup (C) Q2 CY2025 Highlights:

- Net Interest Income: $15.18 billion vs analyst estimates of $14.08 billion (12.5% year-on-year growth, 7.8% beat)

- Revenue: $21.67 billion vs analyst estimates of $20.93 billion (8% year-on-year growth, 3.5% beat)

- Efficiency Ratio: 62.7% vs analyst estimates of 65% (2.3 percentage point beat)

- EPS (GAAP): $1.96 vs analyst estimates of $1.61 (22.1% beat)

- Market Capitalization: $163.4 billion

Company Overview

With operations in nearly 160 countries and a history dating back to 1812, Citigroup (NYSE: C) is a global financial services company that provides banking, investment, wealth management, and payment solutions to consumers, corporations, and governments.

Sales Growth

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income.

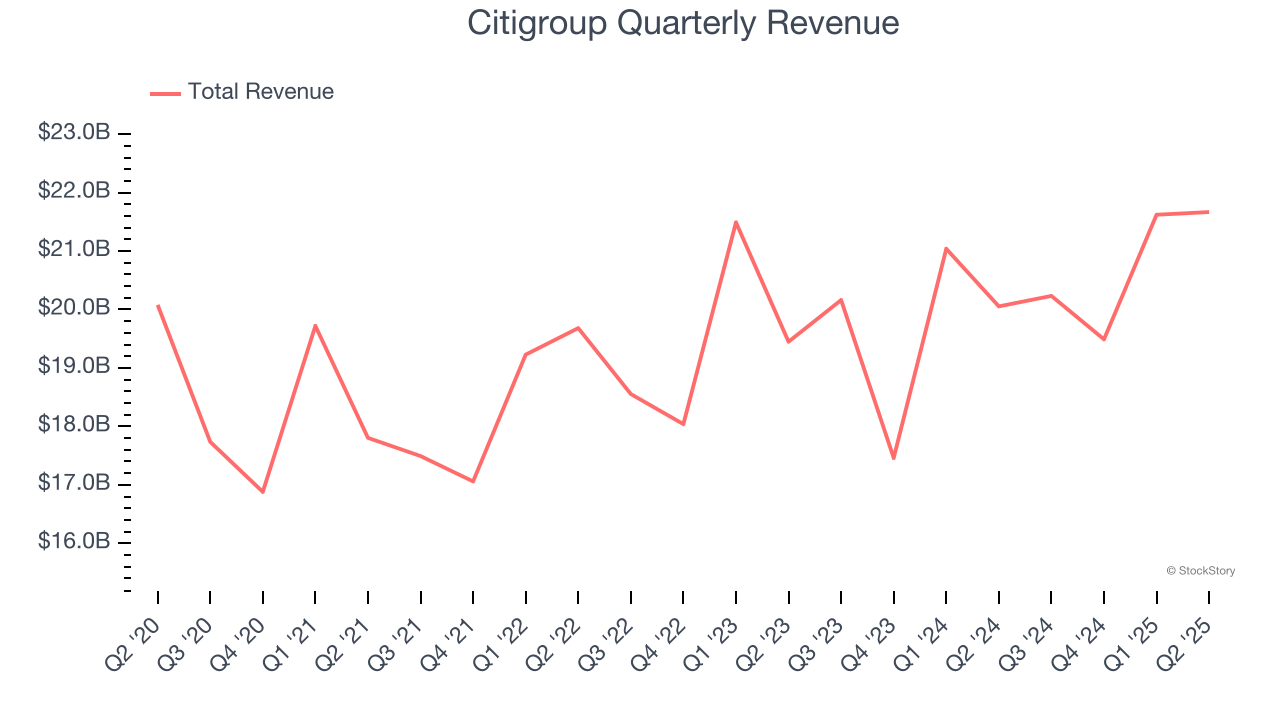

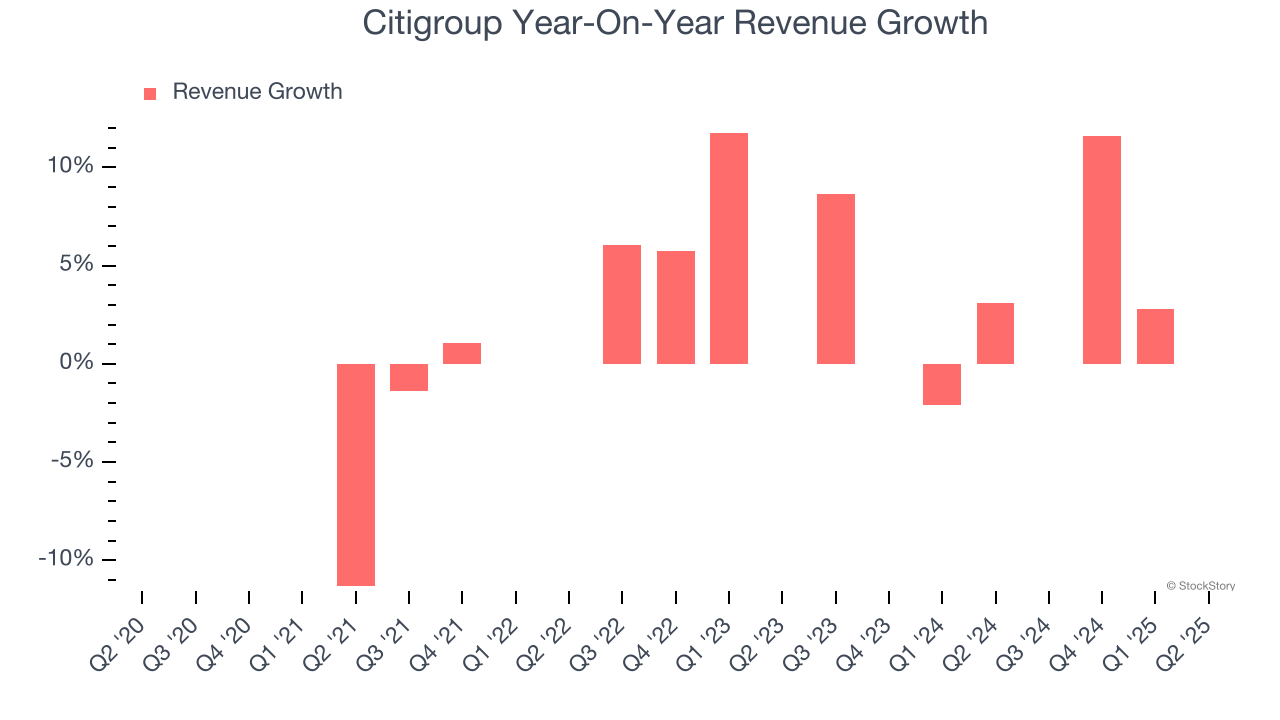

Over the last five years, Citigroup grew its revenue at a tepid 1.1% compounded annual growth rate. This fell short of our benchmarks and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Citigroup’s annualized revenue growth of 3.5% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Citigroup reported year-on-year revenue growth of 8%, and its $21.67 billion of revenue exceeded Wall Street’s estimates by 3.5%.

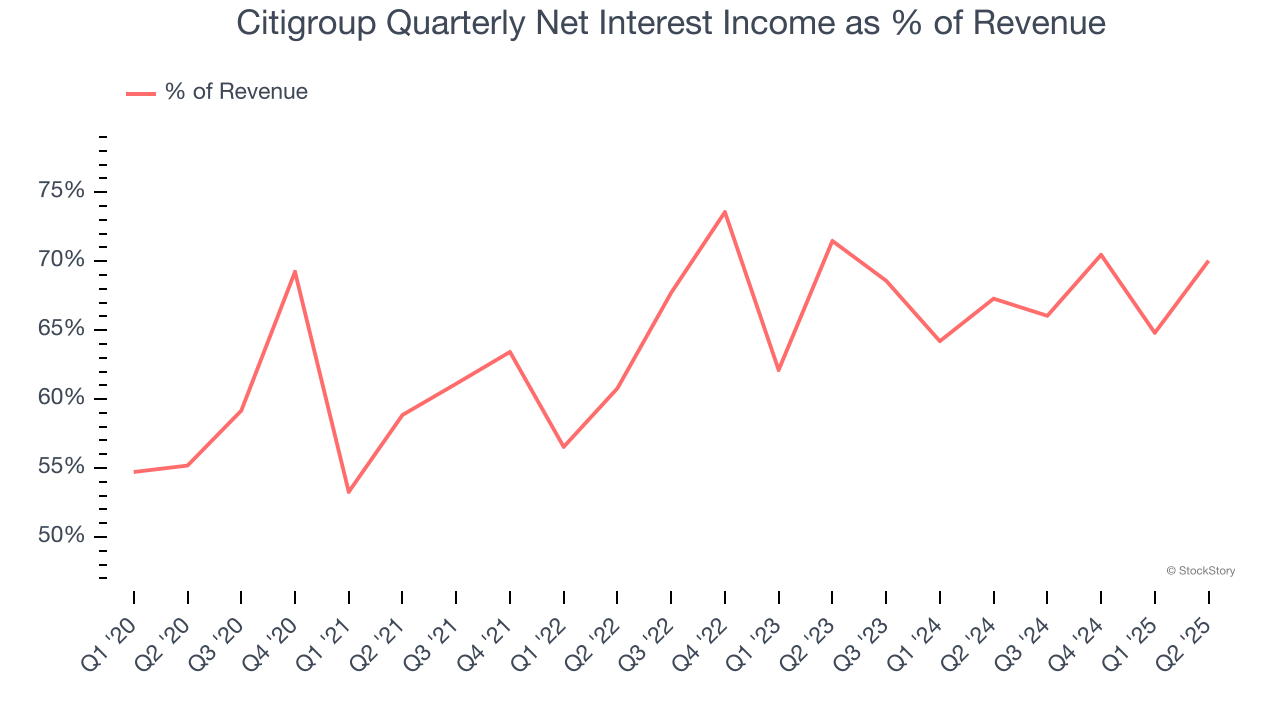

Net interest income made up 64.7% of the company’s total revenue during the last five years, meaning lending operations are Citigroup’s largest source of revenue.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

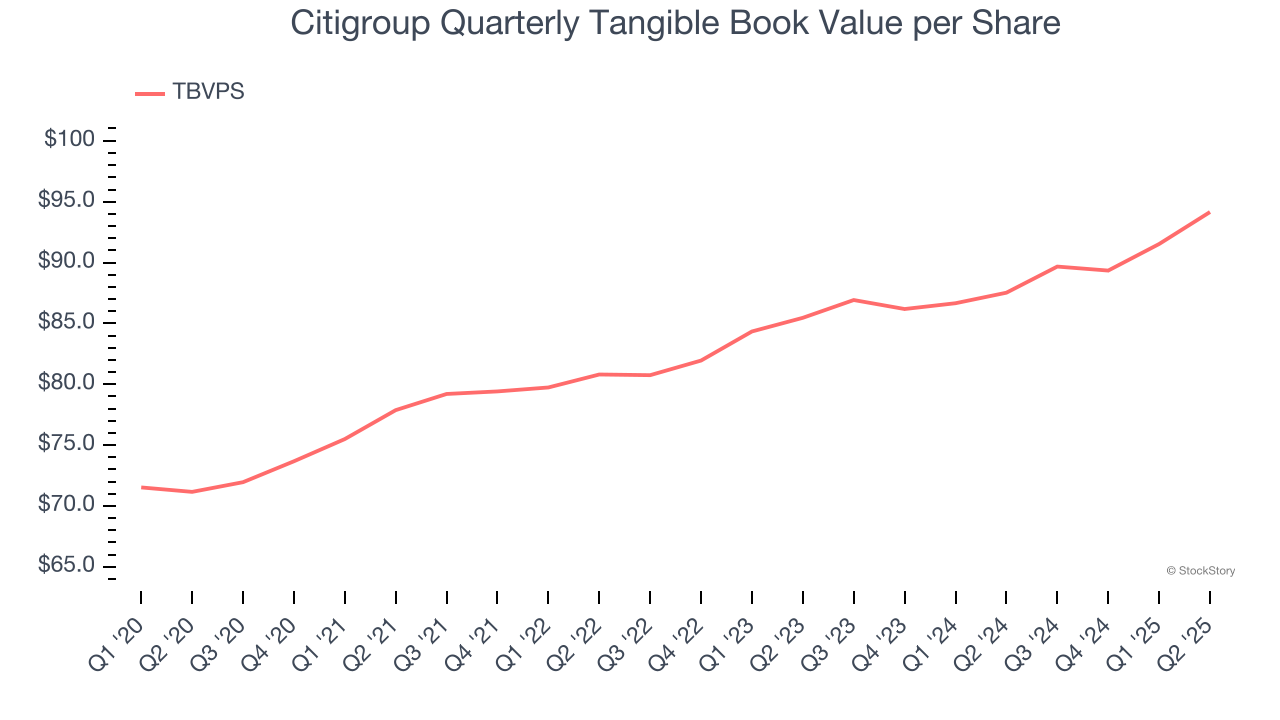

Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

Citigroup’s TBVPS grew at a decent 5.8% annual clip over the last five years. The last two years show a similar trajectory as TBVPS grew by 5% annually from $85.47 to $94.16 per share.

Over the next 12 months, Consensus estimates call for Citigroup’s TBVPS to grow by 9.5% to $103.14, solid growth rate.

Key Takeaways from Citigroup’s Q2 Results

We were impressed by how significantly Citigroup blew past analysts’ EPS expectations this quarter. We were also excited its net interest income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 1.9% to $89.09 immediately following the results.

Citigroup had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.