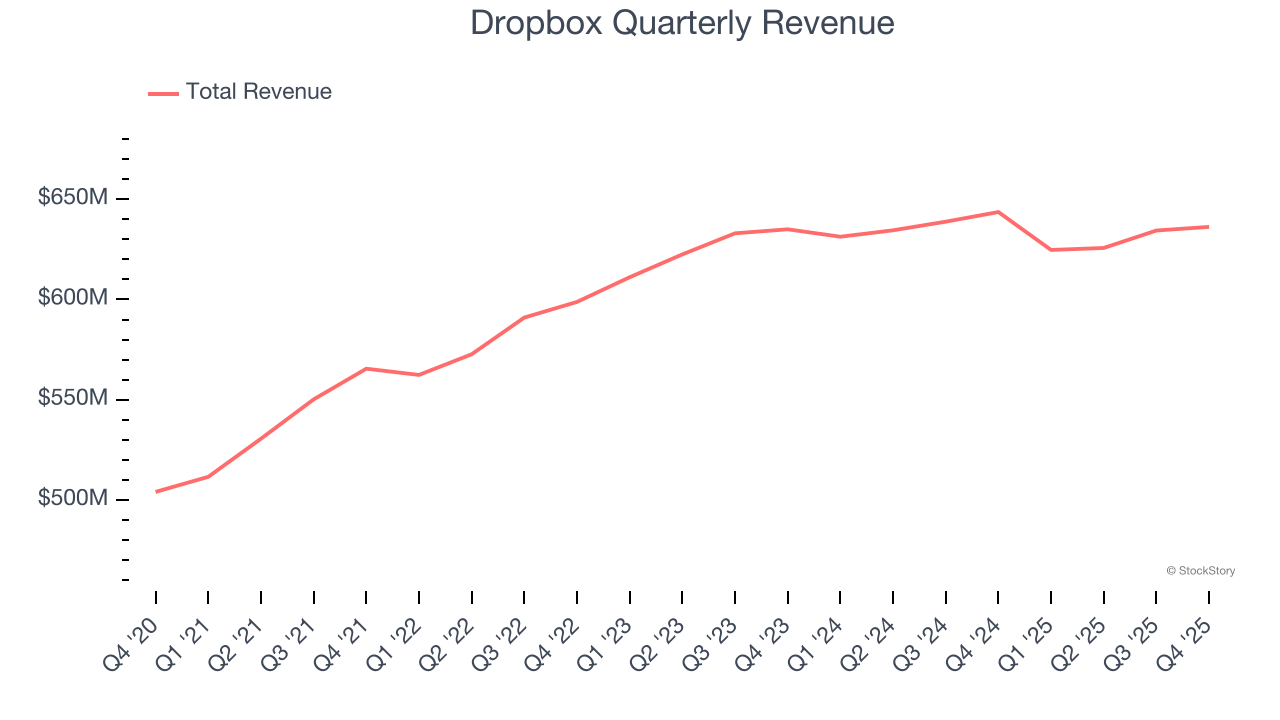

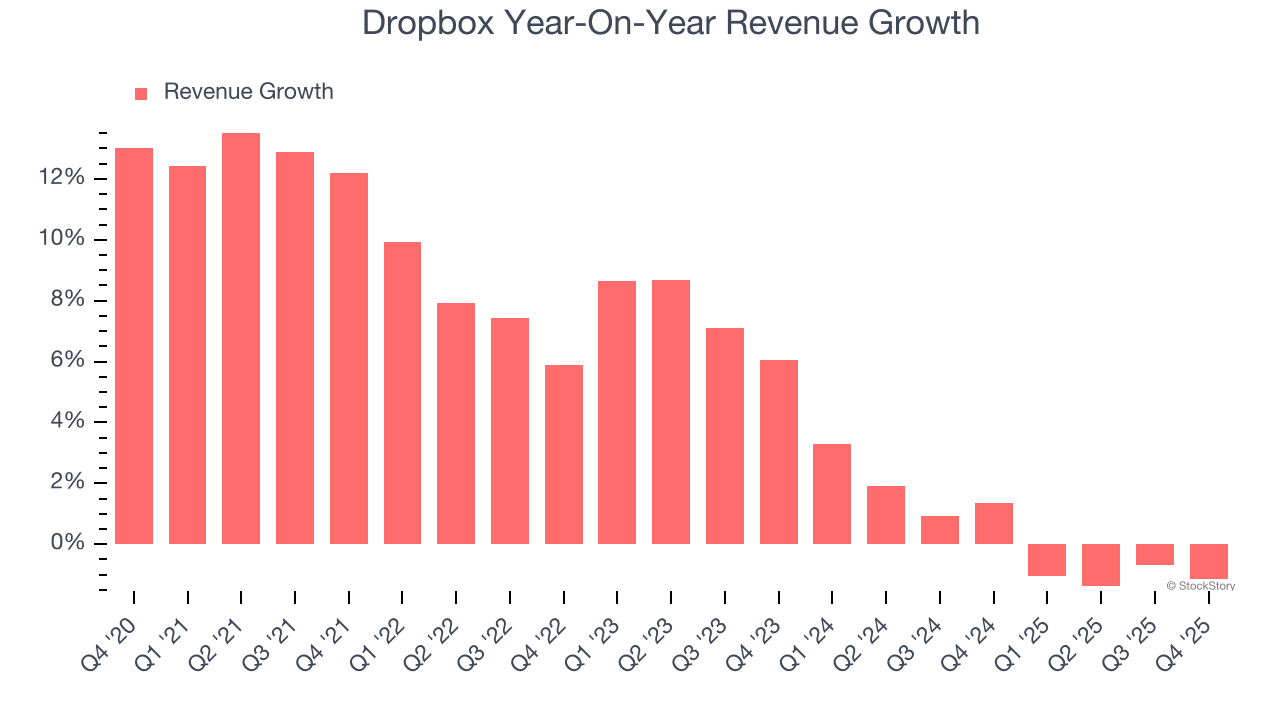

Cloud storage company Dropbox (NASDAQ: DBX) beat Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 1.1% year on year to $636.2 million. Its non-GAAP profit of $0.68 per share was 1.6% above analysts’ consensus estimates.

Is now the time to buy Dropbox? Find out by accessing our full research report, it’s free.

Dropbox (DBX) Q4 CY2025 Highlights:

- Revenue: $636.2 million vs analyst estimates of $629.1 million (1.1% year-on-year decline, 1.1% beat)

- Adjusted EPS: $0.68 vs analyst estimates of $0.67 (1.6% beat)

- Adjusted Operating Income: $243 million vs analyst estimates of $232.4 million (38.2% margin, 4.6% beat)

- Operating Margin: 25.5%, up from 13.7% in the same quarter last year

- Free Cash Flow Margin: 35.4%, down from 46.3% in the previous quarter

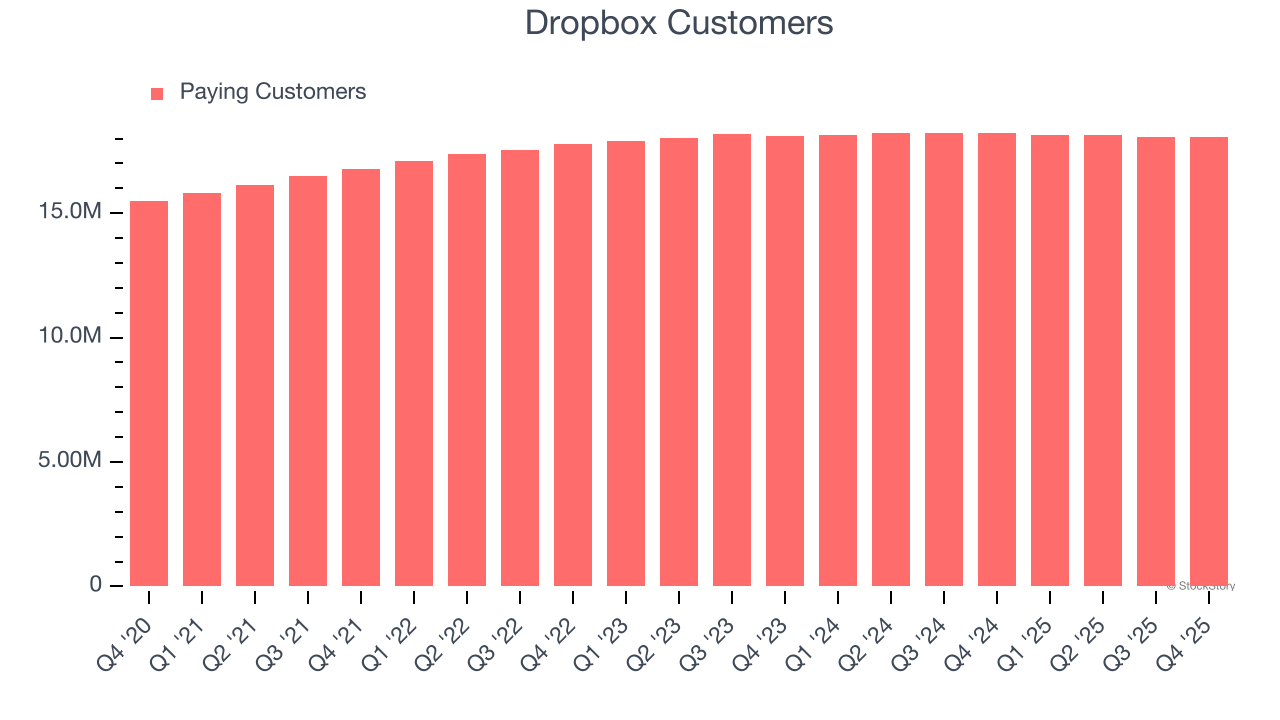

- Customers: 18.08 million, up from 18.07 million in the previous quarter

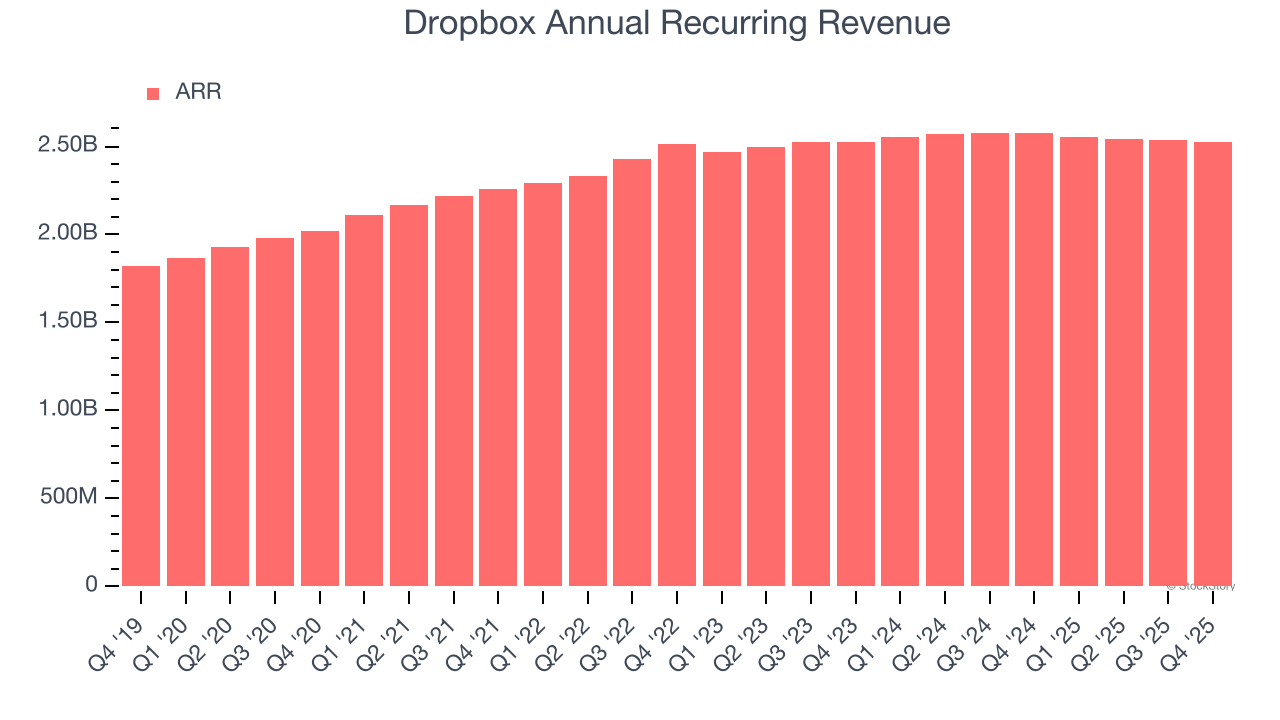

- Annual Recurring Revenue: $2.53 billion vs analyst estimates of $2.52 billion (1.9% year-on-year decline, in line)

- Billings: $624.9 million at quarter end, down 1% year on year

- Market Capitalization: $6.39 billion

“We closed out 2025 on a strong note, exceeding the high end of our revenue and operating margin guidance and demonstrating our continued operating discipline,” said Drew Houston, Dropbox Co-Founder and Chief Executive Officer.

Company Overview

Originally named after the founders' tendency to "drop" files into a shared folder, Dropbox (NASDAQ: DBX) provides a content collaboration platform that helps individuals and teams store, organize, share, and work on files from anywhere.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Dropbox grew its sales at a weak 5.7% compounded annual growth rate. This was below our standard for the software sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Dropbox’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Dropbox’s revenue fell by 1.1% year on year to $636.2 million but beat Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and implies its products and services will face some demand challenges.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Dropbox’s ARR came in at $2.53 billion in Q4, and it averaged 1.2% year-on-year declines over the last four quarters. This performance mirrored its total sales, showing the company lost long-term deals and renewals. It also suggests there may be increasing competition or market saturation.

Customer Base

Dropbox reported 18.08 million customers at the end of the quarter, a sequential increase of 10,000. That’s a little better than last quarter and quite a bit above the typical growth we’ve seen over the previous year. However, the increase in customers wasn’t backed by an equivalent increase in annualized recurring revenue (ARR), suggesting that Dropbox is disproportionately winning smaller customers.

Key Takeaways from Dropbox’s Q4 Results

We were impressed by Dropbox’s strong growth in customers this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. However, ARR was just in line and billings saw a 1% year-on-year decline, a poor omen for future revenue. Overall, this print was mixed. Guidance will be given on the earnings call, and that could move the stock further. So far, investors were likely hoping for more, and shares traded down 1.8% to $24.43 immediately after reporting.

Is Dropbox an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).