As the Q4 earnings season wraps, let’s dig into this quarter’s best and worst performers in the agricultural machinery industry, including Alamo (NYSE: ALG) and its peers.

Agricultural machinery companies are investing to develop and produce more precise machinery, automated systems, and connected equipment that collects analyzable data to help farmers and other customers improve yields and increase efficiency. On the other hand, agriculture is seasonal and natural disasters or bad weather can impact the entire industry. Additionally, macroeconomic factors such as commodity prices or changes in interest rates–which dictate the willingness of these companies or their customers to invest–can impact demand for agricultural machinery.

The 6 agricultural machinery stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was 0.6% above.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 7% since the latest earnings results.

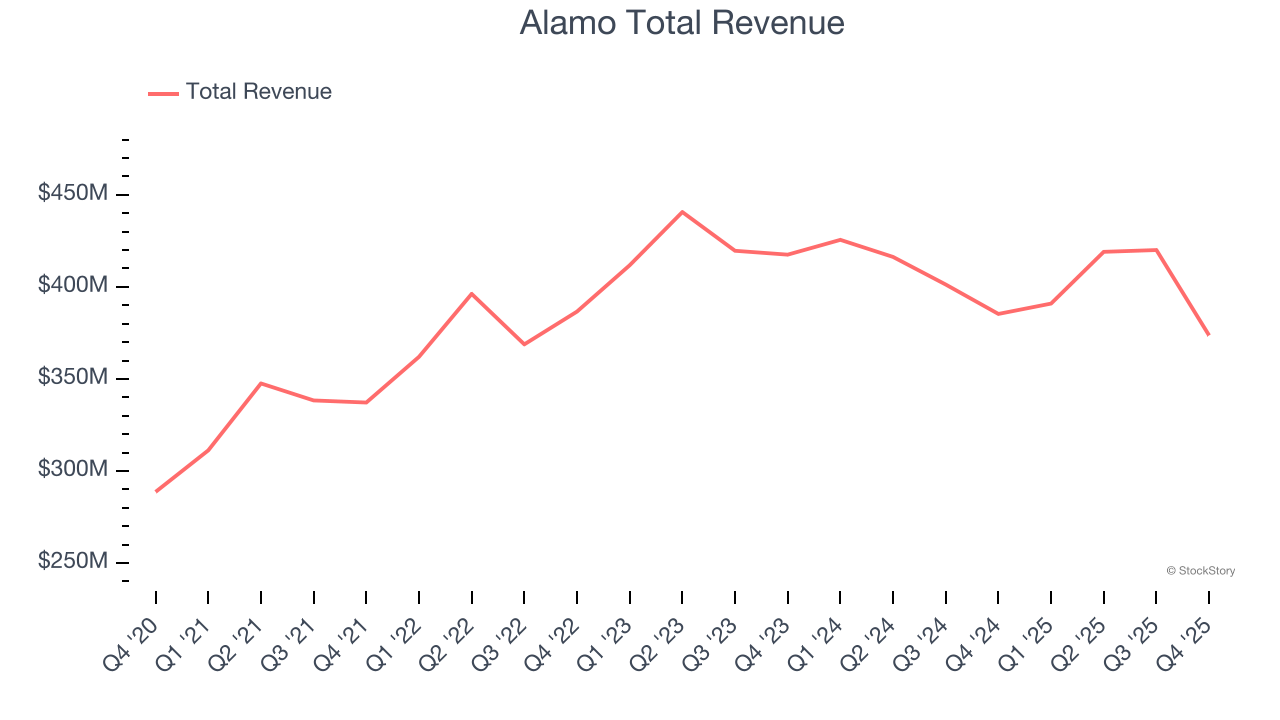

Weakest Q4: Alamo (NYSE: ALG)

Expanding its markets through acquisitions since its founding, Alamo (NSYE:ALG) designs, manufactures, and services vegetation management and infrastructure maintenance equipment for governmental, industrial, and agricultural use.

Alamo reported revenues of $373.7 million, down 3% year on year. This print fell short of analysts’ expectations by 7.8%. Overall, it was a disappointing quarter for the company with a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EBITDA estimates.

Robert Hureau, Alamo Group's President, and Chief Executive Officer commented, "Fiscal year 2025 was a year of transition as we position our Company for long term growth and success. Over the past few months, we've taken several decisive steps to strengthen our foundation including restructuring certain manufacturing facilities, reshaping the organizational structure, sharpening our commercial and operational priorities, accelerating our M&A engine and setting a clear vision for the future. Despite the challenges in the quarter, I'm excited about where we are taking our company and the success that lies ahead."

Alamo delivered the weakest performance against analyst estimates of the whole group. Unsurprisingly, the stock is down 19.6% since reporting and currently trades at $175.68.

Read our full report on Alamo here, it’s free.

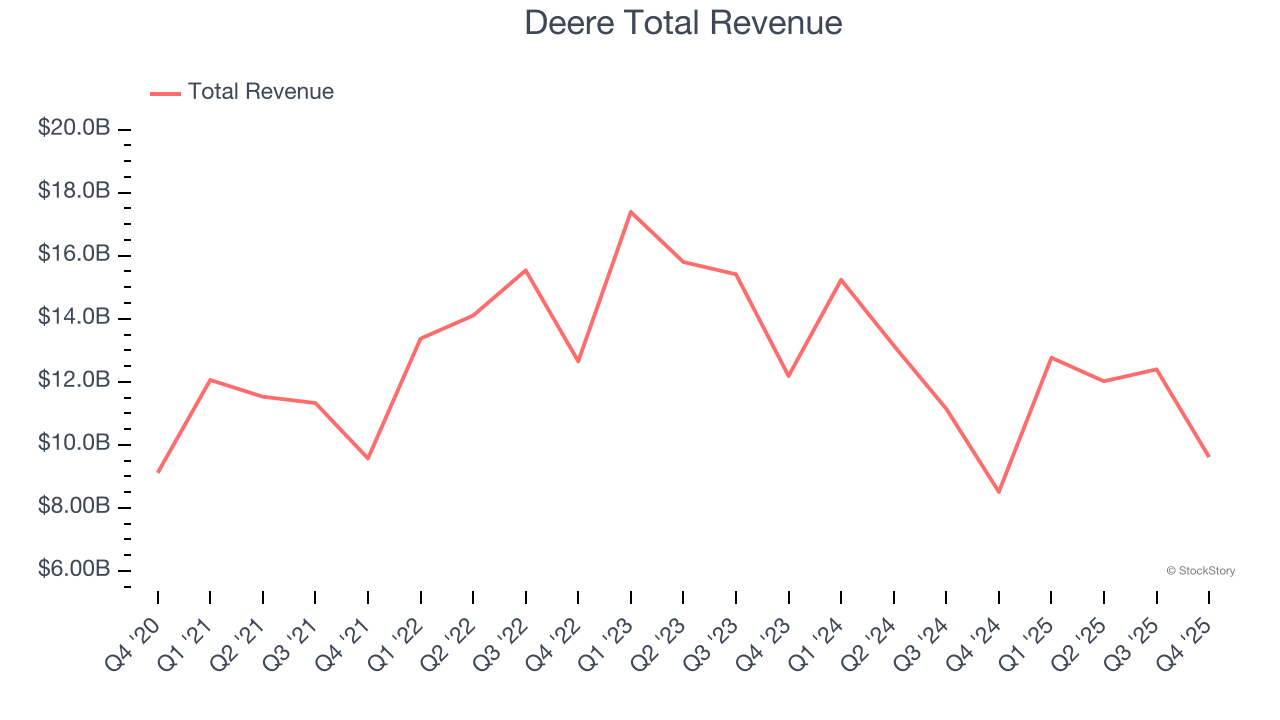

Best Q4: Deere (NYSE: DE)

Revolutionizing agriculture with the first self-polishing cast-steel plow in the 1800s, Deere (NYSE: DE) manufactures and distributes advanced agricultural, construction, forestry, and turf care equipment.

Deere reported revenues of $9.61 billion, up 13% year on year, outperforming analysts’ expectations by 5.9%. The business had a stunning quarter with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

Deere delivered the fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 1.1% since reporting. It currently trades at $587.00.

Is now the time to buy Deere? Access our full analysis of the earnings results here, it’s free.

Lindsay (NYSE: LNN)

A pioneer in the field of center pivot and lateral move irrigation, Lindsay (NYSE: LNN) provides a variety of proprietary water management and road infrastructure products and services.

Lindsay reported revenues of $155.8 million, down 6.3% year on year, falling short of analysts’ expectations by 7%. It was a slower quarter as it posted a significant miss of analysts’ revenue estimates.

Lindsay delivered the slowest revenue growth in the group. Interestingly, the stock is up 5.7% since the results and currently trades at $125.33.

Read our full analysis of Lindsay’s results here.

The Toro Company (NYSE: TTC)

Ceasing all production to support the war effort during World War II, Toro (NYSE: TTC) offers outdoor equipment for residential, commercial, and agricultural use.

The Toro Company reported revenues of $1.04 billion, up 4.2% year on year. This print topped analysts’ expectations by 3.5%. Overall, it was a stunning quarter as it also produced a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

The stock is down 3.6% since reporting and currently trades at $97.15.

Read our full, actionable report on The Toro Company here, it’s free.

AGCO (NYSE: AGCO)

With a history that features both organic growth and acquisitions, AGCO (NYSE: AGCO) designs, manufactures, and sells agricultural machinery and related technology.

AGCO reported revenues of $2.92 billion, up 1.1% year on year. This number surpassed analysts’ expectations by 9.6%. It was a very strong quarter as it also put up an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ adjusted operating income estimates.

AGCO scored the biggest analyst estimates beat but had the weakest full-year guidance update among its peers. The stock is down 2.2% since reporting and currently trades at $119.00.

Read our full, actionable report on AGCO here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.