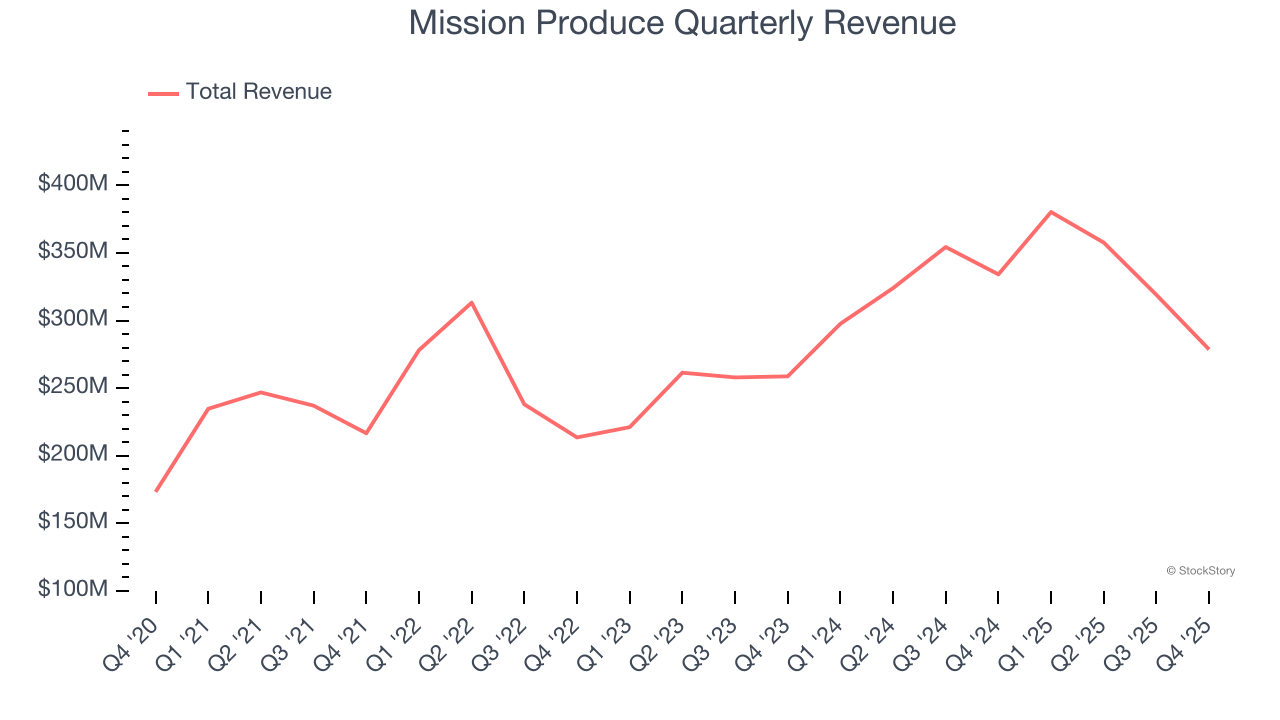

Avocado company Mission Produce (NASDAQ: AVO) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 16.6% year on year to $278.6 million. Its non-GAAP profit of $0.10 per share was 36.4% above analysts’ consensus estimates.

Is now the time to buy Mission Produce? Find out by accessing our full research report, it’s free.

Mission Produce (AVO) Q4 CY2025 Highlights:

- Revenue: $278.6 million vs analyst estimates of $260.7 million (16.6% year-on-year decline, 6.9% beat)

- Adjusted EPS: $0.10 vs analyst estimates of $0.07 (36.4% beat)

- Adjusted EBITDA: $20.6 million vs analyst estimates of $17.27 million (7.4% margin, 19.3% beat)

- Operating Margin: 0.9%, down from 2.9% in the same quarter last year

- Free Cash Flow was -$14.9 million compared to -$16 million in the same quarter last year

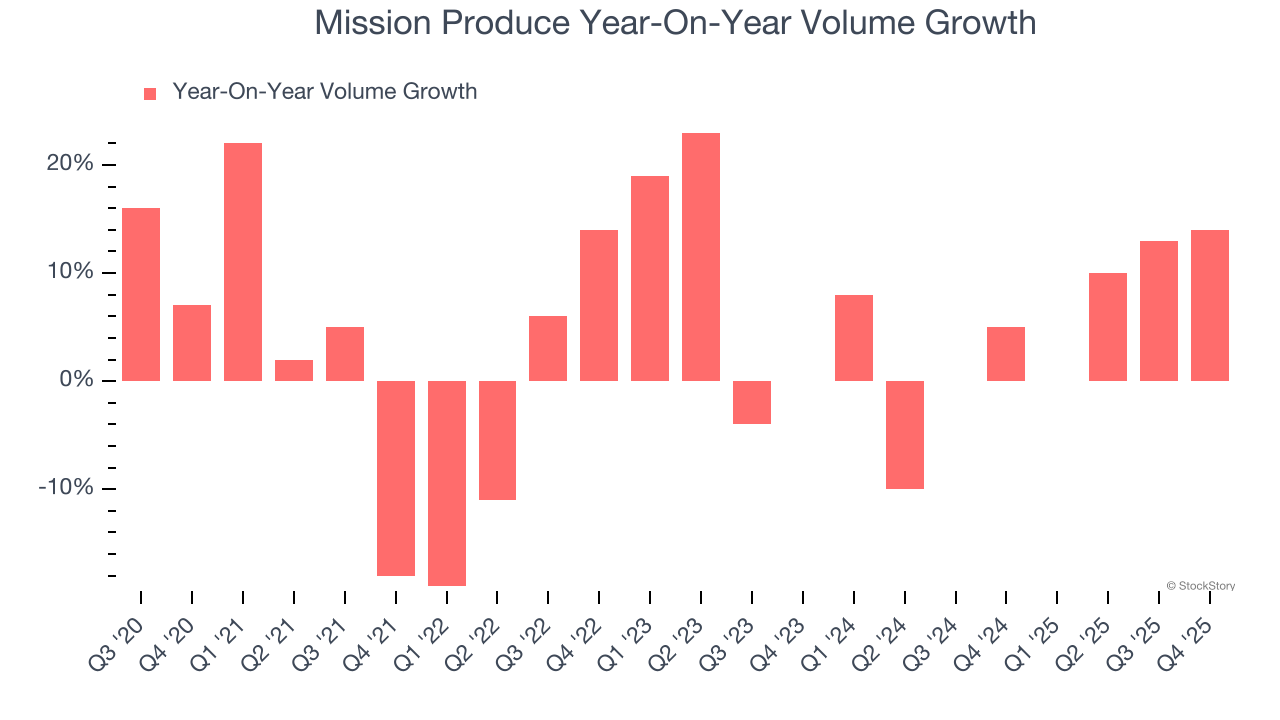

- Sales Volumes rose 14% year on year (5% in the same quarter last year)

- Market Capitalization: $943.7 million

Steve Barnard, CEO of Mission, stated, "We are off to a strong start in fiscal 2026, delivering 14% avocado volume growth and strong adjusted EBITDA results as industry pricing normalized from the elevated levels experienced over the past year. These results demonstrate our business model's resilience and our team's ability to execute consistently across market conditions. We're deepening customer relationships and expanding category penetration while focusing on the two levers that drive long-term value: volume growth and per-unit margin management. This approach delivered gross margin expansion in the quarter, reflecting ongoing optimization in our Marketing & Distribution segment and operational discipline across our platform."

Company Overview

Founded in 1983 in California, Mission Produce (NASDAQ: AVO) grows, packages, and distributes avocados.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $1.34 billion in revenue over the past 12 months, Mission Produce is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Mission Produce grew its sales at a decent 8.6% compounded annual growth rate over the last three years as consumers bought more of its products.

This quarter, Mission Produce’s revenue fell by 16.6% year on year to $278.6 million but beat Wall Street’s estimates by 6.9%.

Looking ahead, sell-side analysts expect revenue to decline by 20.6% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products will face some demand challenges.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Mission Produce’s average quarterly volume growth was a robust 5% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Mission Produce’s Q4 2026, sales volumes jumped 14% year on year. This result was an acceleration from its historical levels, certainly a positive signal.

Key Takeaways from Mission Produce’s Q4 Results

We were impressed by how significantly Mission Produce blew past analysts’ gross margin expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The market seemed to be hoping for more, and the stock traded down 1.5% to $13.03 immediately following the results.

Big picture, is Mission Produce a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).