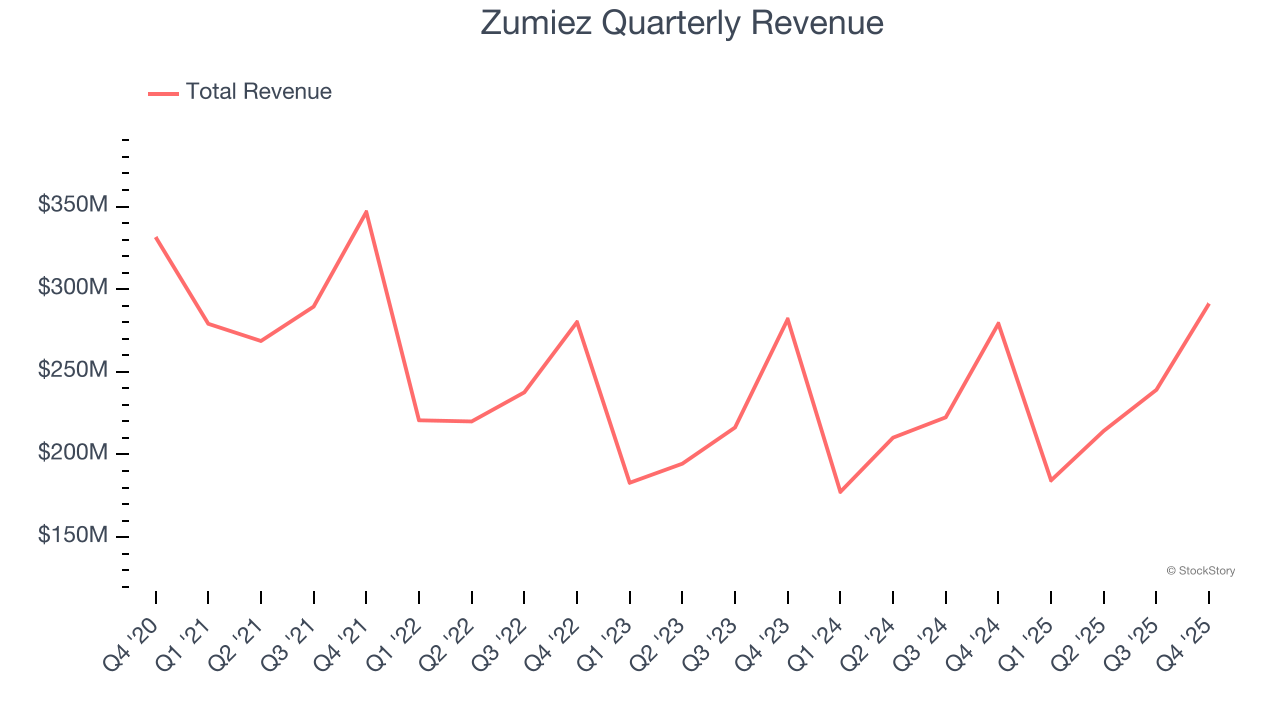

Clothing and footwear retailer Zumiez (NASDAQ: ZUMZ) announced better-than-expected revenue in Q4 CY2025, with sales up 4.4% year on year to $291.3 million. Guidance for next quarter’s revenue was optimistic at $191 million at the midpoint, 2.5% above analysts’ estimates. Its GAAP profit of $1.16 per share was 8.9% above analysts’ consensus estimates.

Is now the time to buy Zumiez? Find out by accessing our full research report, it’s free.

Zumiez (ZUMZ) Q4 CY2025 Highlights:

- Revenue: $291.3 million vs analyst estimates of $289.1 million (4.4% year-on-year growth, 0.8% beat)

- EPS (GAAP): $1.16 vs analyst estimates of $1.07 (8.9% beat)

- Adjusted EBITDA: $37.43 million vs analyst estimates of $29.81 million (12.8% margin, 25.6% beat)

- Revenue Guidance for Q1 CY2026 is $191 million at the midpoint, above analyst estimates of $186.3 million

- EPS (GAAP) guidance for Q1 CY2026 is -$0.82 at the midpoint, missing analyst estimates by 9.3%

- Operating Margin: 8.6%, up from 7.2% in the same quarter last year

- Free Cash Flow Margin: 18.6%, similar to the same quarter last year

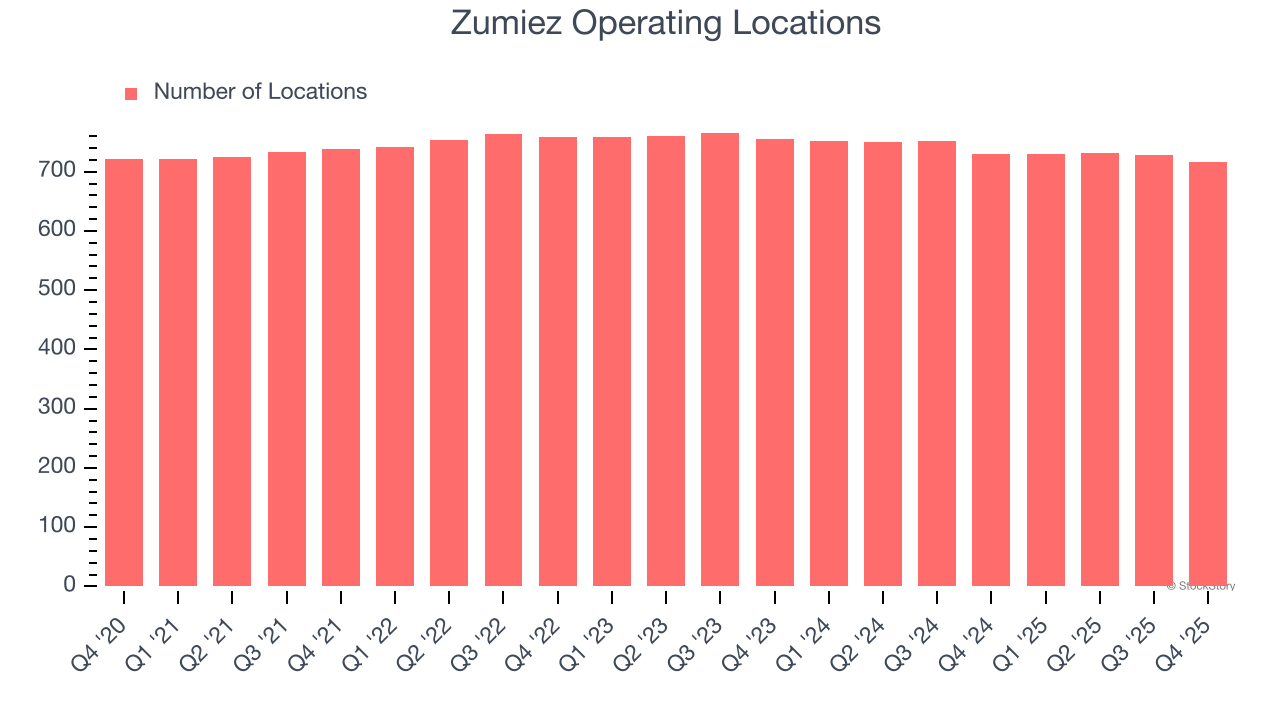

- Locations: 716 at quarter end, down from 730 in the same quarter last year

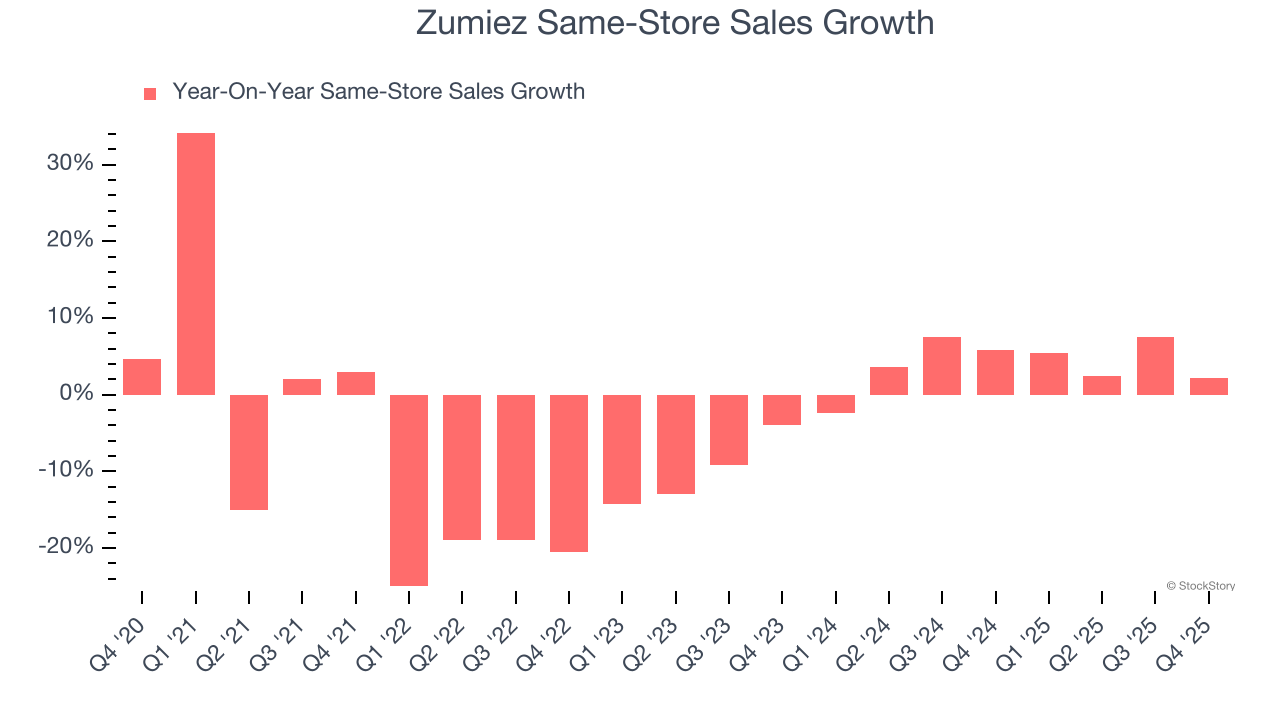

- Same-Store Sales rose 2.2% year on year (5.9% in the same quarter last year)

- Market Capitalization: $392.9 million

Rick Brooks, Chief Executive Officer of Zumiez Inc., stated, “Our fourth quarter performance was highlighted by strong full price selling in North America which fueled mid-single digit comparable sales growth in the region and meaningful gross margin expansion. In addition to these results, our focus on assortment and full price selling in the European business drove 250 basis points of improvement in product margin year over year. Fiscal 2025 represented an important step towards returning to historical levels of sales and earnings, and while we still have work to do, our results underscore the success of our recent merchandise assortments, customer experience and expense management. We started the new year with good momentum and believe we have the right plans in place to build on our recent progress including generating increased cash which we’ll deploy to drive growth and enhanced shareholder value.”

Company Overview

With store associates called “Zumiez Stash Members”, Zumiez (NASDAQ: ZUMZ) is a specialty retailer of street and skate apparel, footwear, and accessories.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $929.1 million in revenue over the past 12 months, Zumiez is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Zumiez struggled to generate demand over the last three years. Its sales dropped by 1% annually as it closed stores.

This quarter, Zumiez reported modest year-on-year revenue growth of 4.4% but beat Wall Street’s estimates by 0.8%. Company management is currently guiding for a 3.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.3% over the next 12 months. While this projection indicates its newer products will catalyze better top-line performance, it is still below the sector average.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Zumiez listed 716 locations in the latest quarter and has generally closed its stores over the last two years, averaging 2.3% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Zumiez’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4% per year. Given its declining store base over the same period, this performance stems from a mixture of higher e-commerce sales and increased foot traffic at existing locations (closing stores can sometimes boost same-store sales).

In the latest quarter, Zumiez’s same-store sales rose 2.2% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from Zumiez’s Q4 Results

We were impressed by how significantly Zumiez blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its gross margin fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The market seemed to be hoping for more, and the stock traded down 6.8% to $21.86 immediately following the results.

So do we think Zumiez is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).