As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the traditional fast food industry, including El Pollo Loco (NASDAQ: LOCO) and its peers.

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

The 13 traditional fast food stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 1%.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

El Pollo Loco (NASDAQ: LOCO)

With a name that translates into ‘The Crazy Chicken’, El Pollo Loco (NASDAQ: LOCO) is a fast food chain known for its citrus-marinated, fire-grilled chicken recipe that hails from the coastal town of Sinaloa, Mexico.

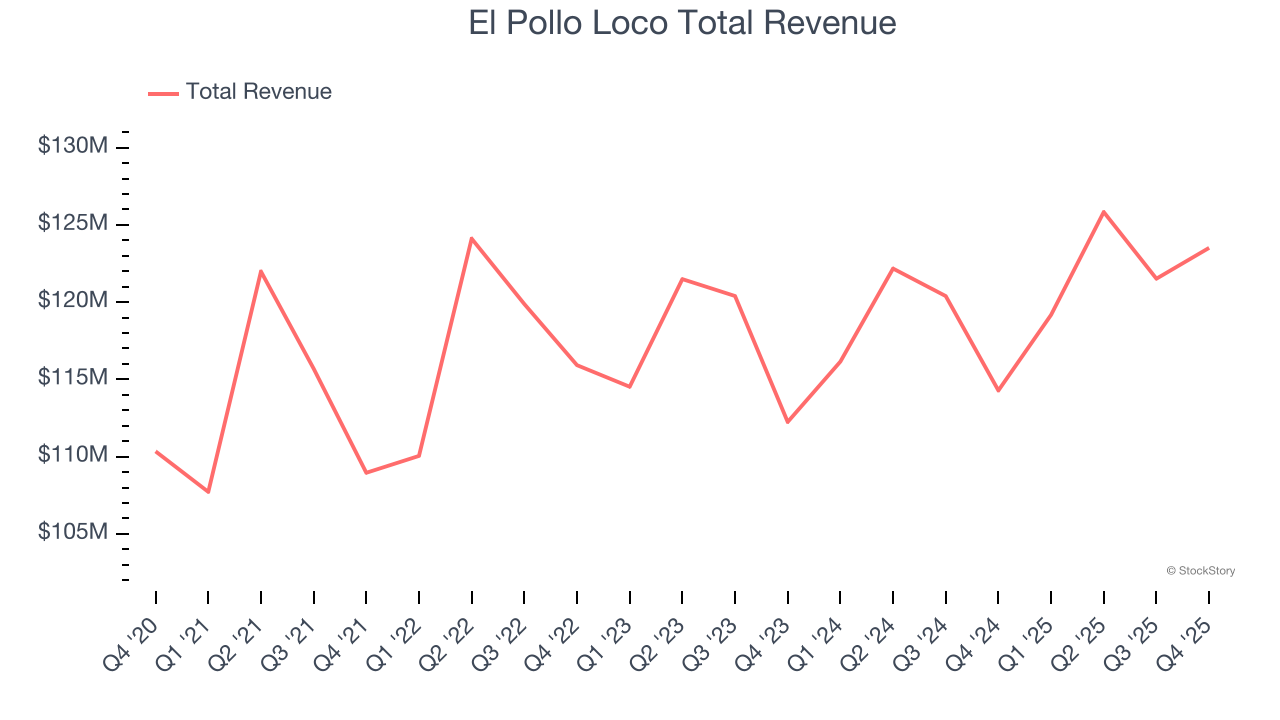

El Pollo Loco reported revenues of $123.5 million, up 8.1% year on year. This print was in line with analysts’ expectations, and overall, it was a very strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ same-store sales estimates.

“During the quarter, we not only delivered positive same store sales growth but also achieved growth in restaurant-level margins. As we look ahead, our priority for 2026 is clear: to drive sustainable traffic growth across our system and thoughtfully accelerate new restaurant growth in new markets,” said Liz Williams, Chief Executive Officer of El Pollo Loco Holdings, Inc.

Interestingly, the stock is up 29.3% since reporting and currently trades at $14.07.

Is now the time to buy El Pollo Loco? Access our full analysis of the earnings results here, it’s free.

Best Q4: Krispy Kreme (NASDAQ: DNUT)

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ: DNUT) is one of the most beloved and well-known fast-food chains in the world.

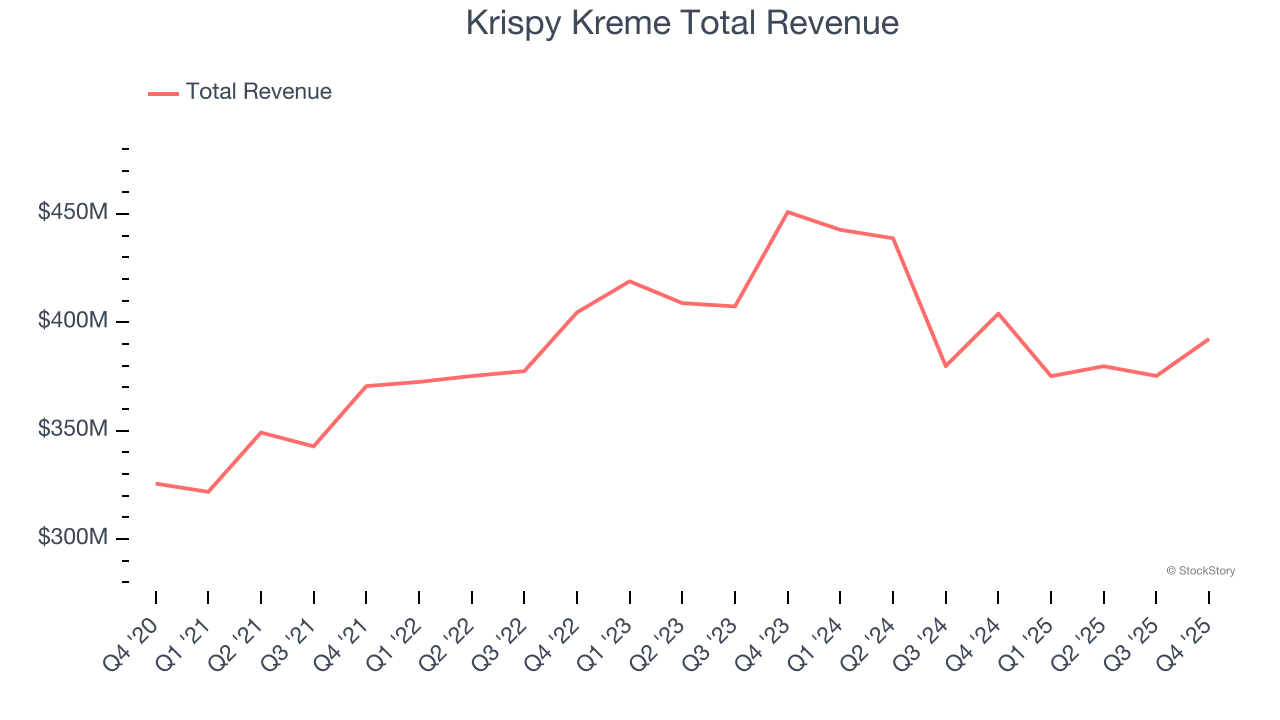

Krispy Kreme reported revenues of $392.4 million, down 2.9% year on year, outperforming analysts’ expectations by 1%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 13% since reporting. It currently trades at $3.38.

Is now the time to buy Krispy Kreme? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Jack in the Box (NASDAQ: JACK)

Delighting customers since its inception in 1951, Jack in the Box (NASDAQ: JACK) is a distinctive fast-food chain known for its bold flavors, innovative menu items, and quirky marketing.

Jack in the Box reported revenues of $349.5 million, down 5.8% year on year, falling short of analysts’ expectations by 4.8%. It was a softer quarter as it posted a significant miss of analysts’ revenue estimates and a miss of analysts’ same-store sales estimates.

Jack in the Box delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 48.9% since the results and currently trades at $11.24.

Read our full analysis of Jack in the Box’s results here.

Yum! Brands (NYSE: YUM)

Spun off as an independent company from PepsiCo, Yum! Brands (NYSE: YUM) is a multinational corporation that owns KFC, Pizza Hut, Taco Bell, and The Habit Burger Grill.

Yum! Brands reported revenues of $2.51 billion, up 6.4% year on year. This print beat analysts’ expectations by 2.7%. Overall, it was a very strong quarter as it also produced a solid beat of analysts’ revenue estimates and an impressive beat of analysts’ same-store sales estimates.

The stock is flat since reporting and currently trades at $159.20.

Read our full, actionable report on Yum! Brands here, it’s free.

Wendy's (NASDAQ: WEN)

Founded by Dave Thomas in 1969, Wendy’s (NASDAQ: WEN) is a renowned fast-food chain known for its fresh, never-frozen beef burgers, flavorful menu options, and commitment to quality.

Wendy's reported revenues of $543 million, down 5.5% year on year. This number surpassed analysts’ expectations by 1.3%. More broadly, it was a slower quarter as it recorded full-year EBITDA guidance missing analysts’ expectations significantly and a miss of analysts’ same-store sales estimates.

The stock is down 1.5% since reporting and currently trades at $7.16.

Read our full, actionable report on Wendy's here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.