What a time it’s been for Teradyne. In the past six months alone, the company’s stock price has increased by a massive 138%, reaching $322.03 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Teradyne, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Teradyne Not Exciting?

We’re glad investors have benefited from the price increase, but we're cautious about Teradyne. Here are three reasons you should be careful with TER and a stock we'd rather own.

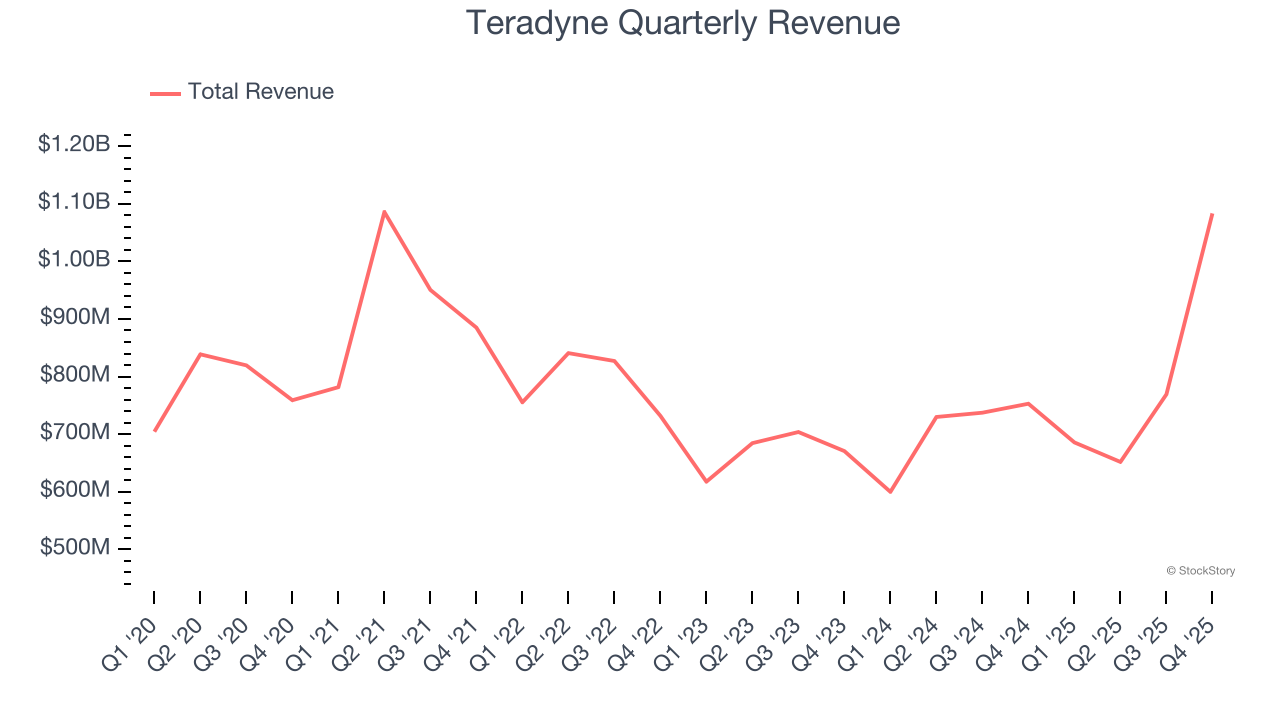

1. Long-Term Revenue Growth Flatter Than a Pancake

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Teradyne struggled to consistently increase demand as its $3.19 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and is a sign of lacking business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

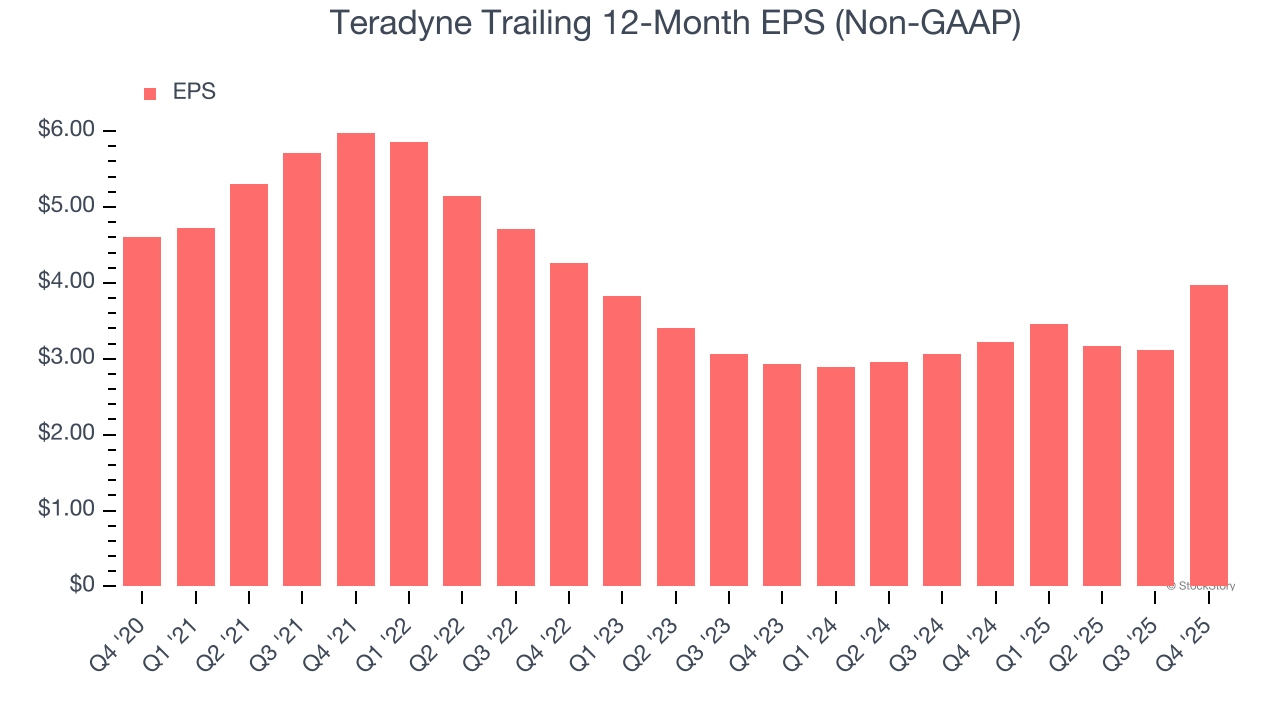

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Teradyne, its EPS declined by 2.9% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

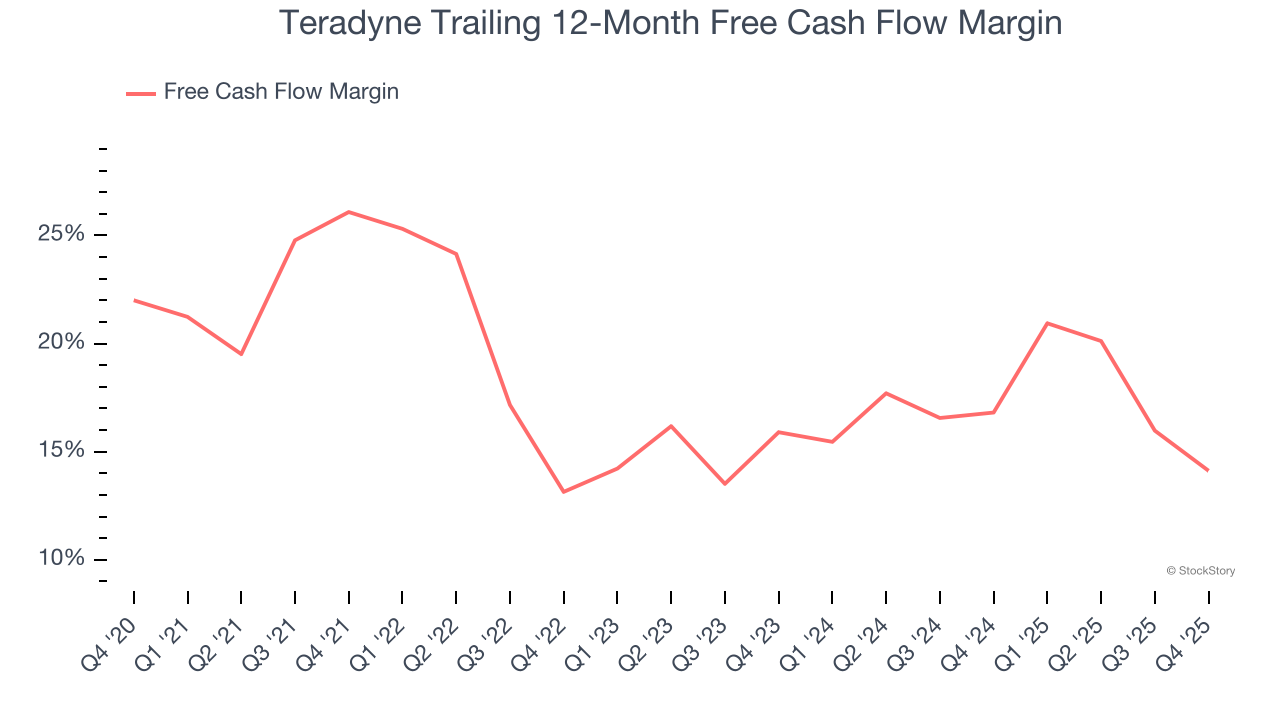

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Teradyne’s margin dropped by 12 percentage points over the last five years. Continued declines could signal it is in the middle of an investment cycle. Teradyne’s free cash flow margin for the trailing 12 months was 14.1%.

Final Judgment

Teradyne isn’t a terrible business, but it isn’t one of our picks. Following the recent surge, the stock trades at 51.3× forward P/E (or $322.03 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.