Shareholders of Carvana would probably like to forget the past six months even happened. The stock dropped 20.1% and now trades at $301.32. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for CVNA? Find out in our full research report, it’s free.

Why Does CVNA Stock Spark Debate?

Known for its glass tower car vending machines, Carvana (NYSE: CVNA) provides a convenient automotive shopping experience by offering an online platform for buying and selling used cars.

Two Positive Attributes:

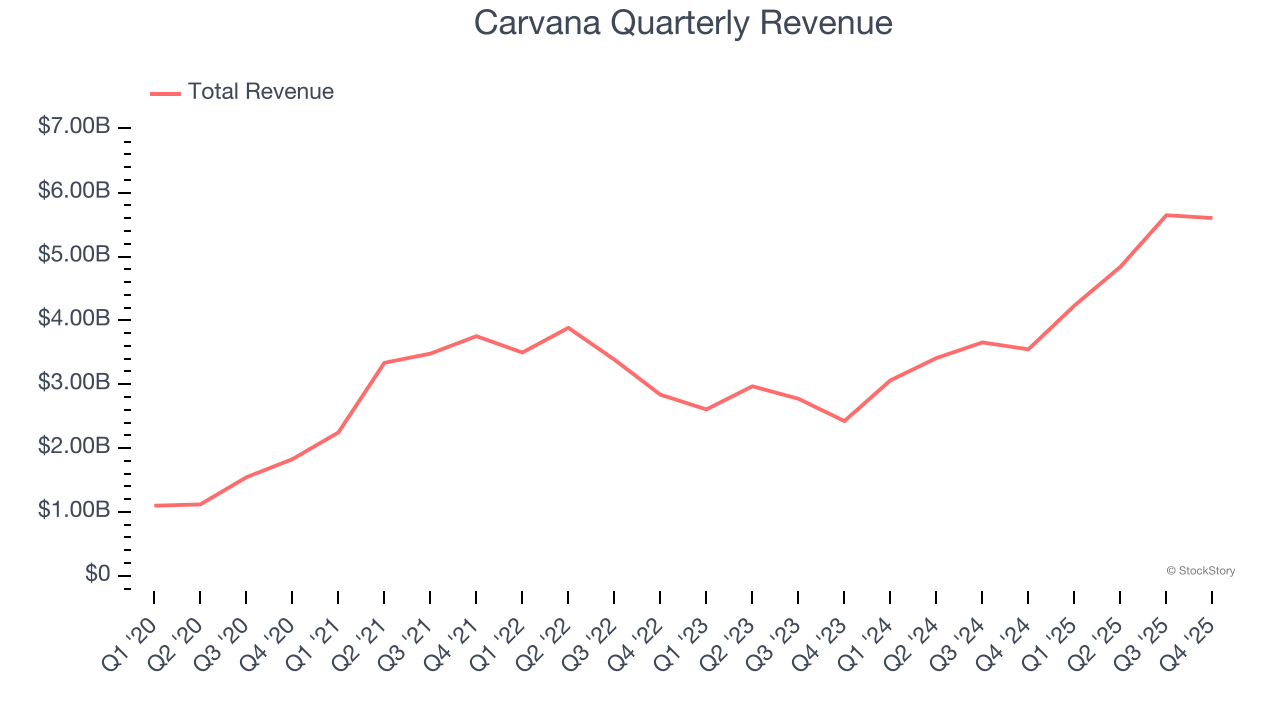

1. Long-Term Revenue Growth Shows Strong Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Carvana’s 14.3% annualized revenue growth over the last three years was solid. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers.

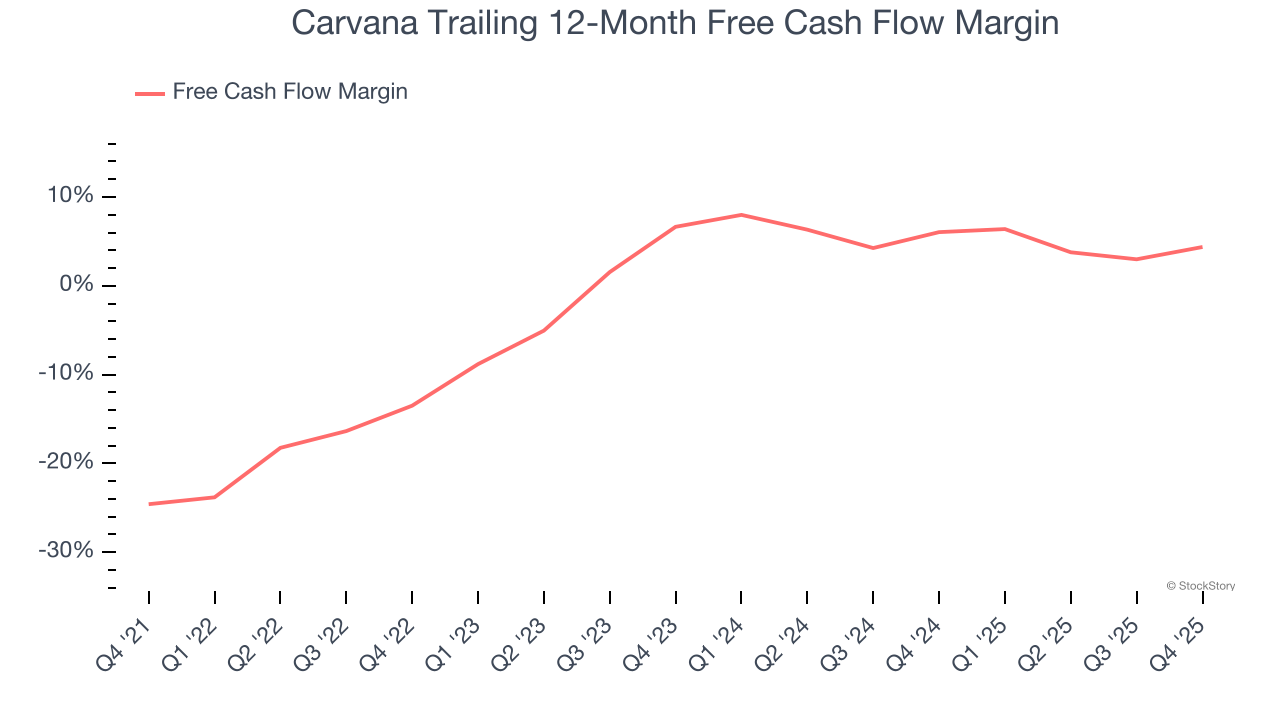

2. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Carvana’s margin expanded by 17.9 percentage points over the last few years. This is encouraging because it gives the company more optionality. Carvana’s free cash flow margin for the trailing 12 months was 4.4%.

One Reason to be Careful:

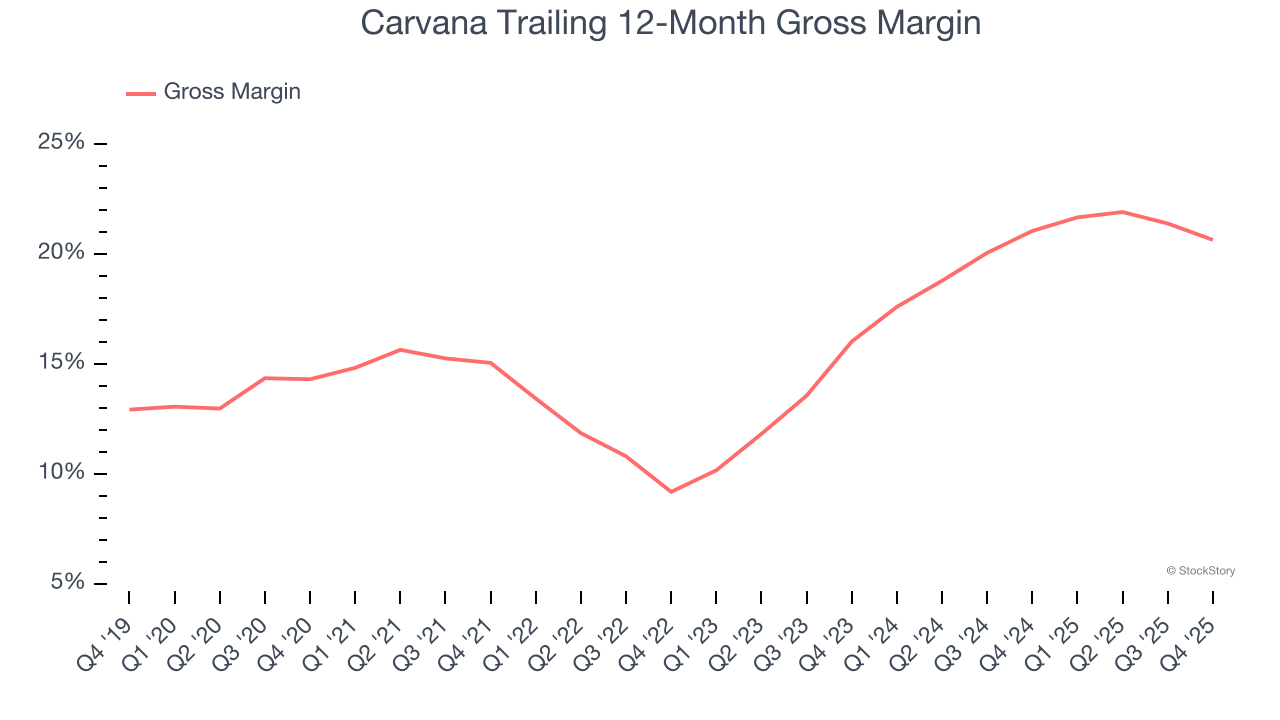

Low Gross Margin Reveals Weak Structural Profitability

For online retail (separate from online marketplaces) businesses like Carvana, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include the cost of acquiring the products sold, shipping and fulfillment, customer service, and digital infrastructure.

Carvana’s unit economics are far below other consumer internet companies because it must carry inventories as an online retailer. This means it has relatively higher capital intensity than a pure software business like Meta or Airbnb and signals it operates in a competitive market. As you can see below, it averaged a 20.8% gross margin over the last two years. Said differently, Carvana had to pay a chunky $79.21 to its service providers for every $100 in revenue.

Final Judgment

Carvana has huge potential even though it has some open questions. With the recent decline, the stock trades at 24.6× forward EV/EBITDA (or $301.32 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.