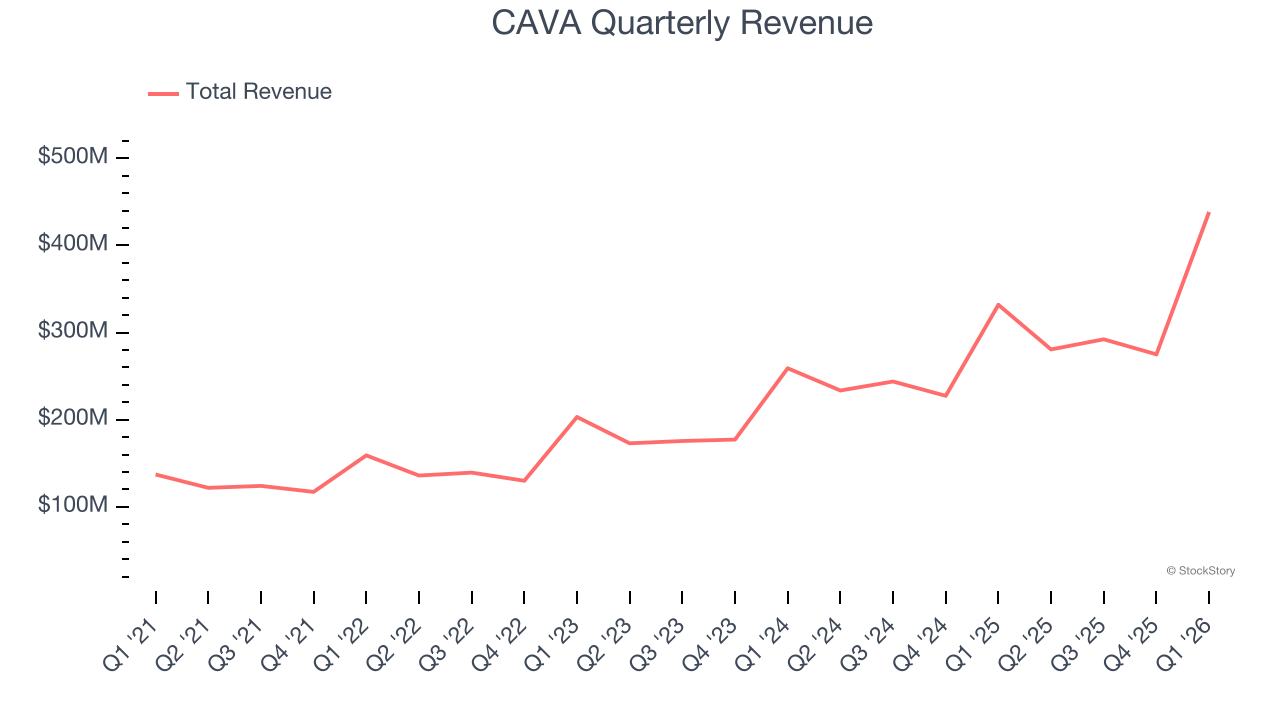

Mediterranean fast-casual restaurant chain CAVA (NYSE: CAVA) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 32.1% year on year to $438.3 million. Its GAAP profit of $0.20 per share was 14% above analysts’ consensus estimates.

Is now the time to buy CAVA? Find out by accessing our full research report, it’s free.

CAVA (CAVA) Q1 CY2026 Highlights:

- Revenue: $438.3 million vs analyst estimates of $418.4 million (32.1% year-on-year growth, 4.7% beat)

- EPS (GAAP): $0.20 vs analyst estimates of $0.18 (14% beat)

- Adjusted EBITDA: $61.73 million vs analyst estimates of $57.31 million (14.1% margin, 7.7% beat)

- EBITDA guidance for the full year is $186 million at the midpoint, in line with analyst expectations

- Operating Margin: 5.8%, up from 4.7% in the same quarter last year

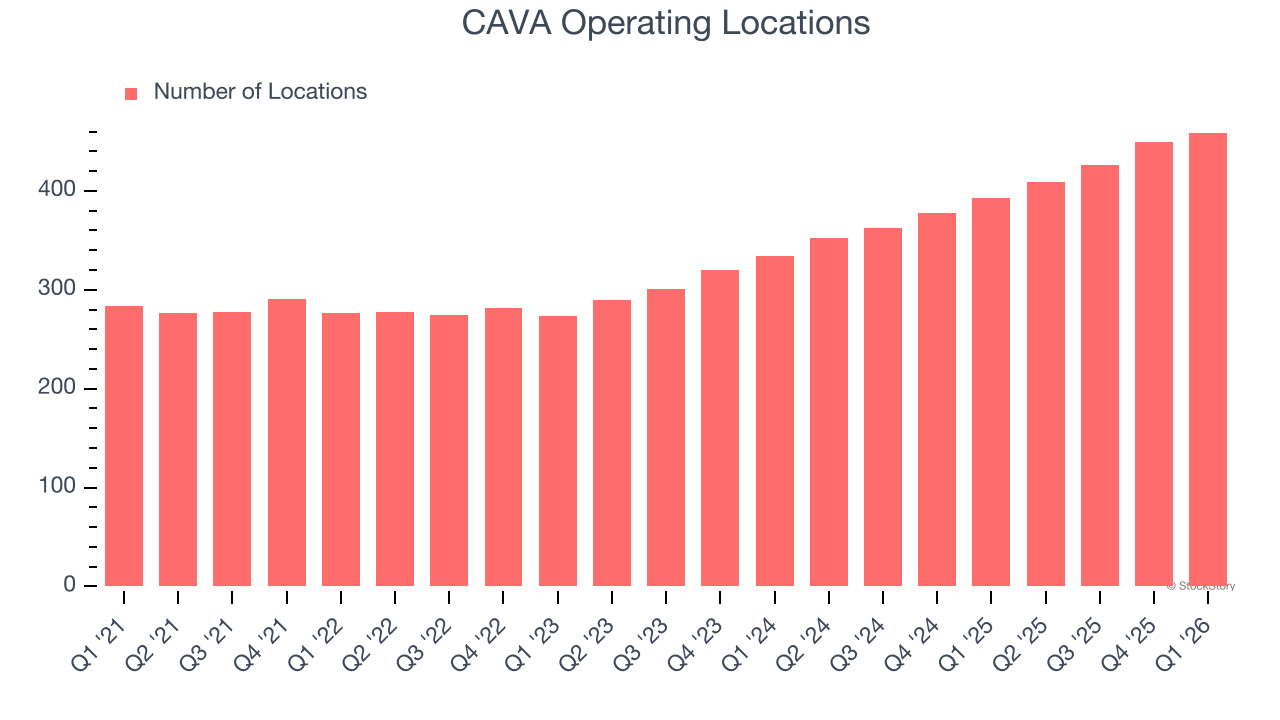

- Locations: 459 at quarter end, up from 393 in the same quarter last year

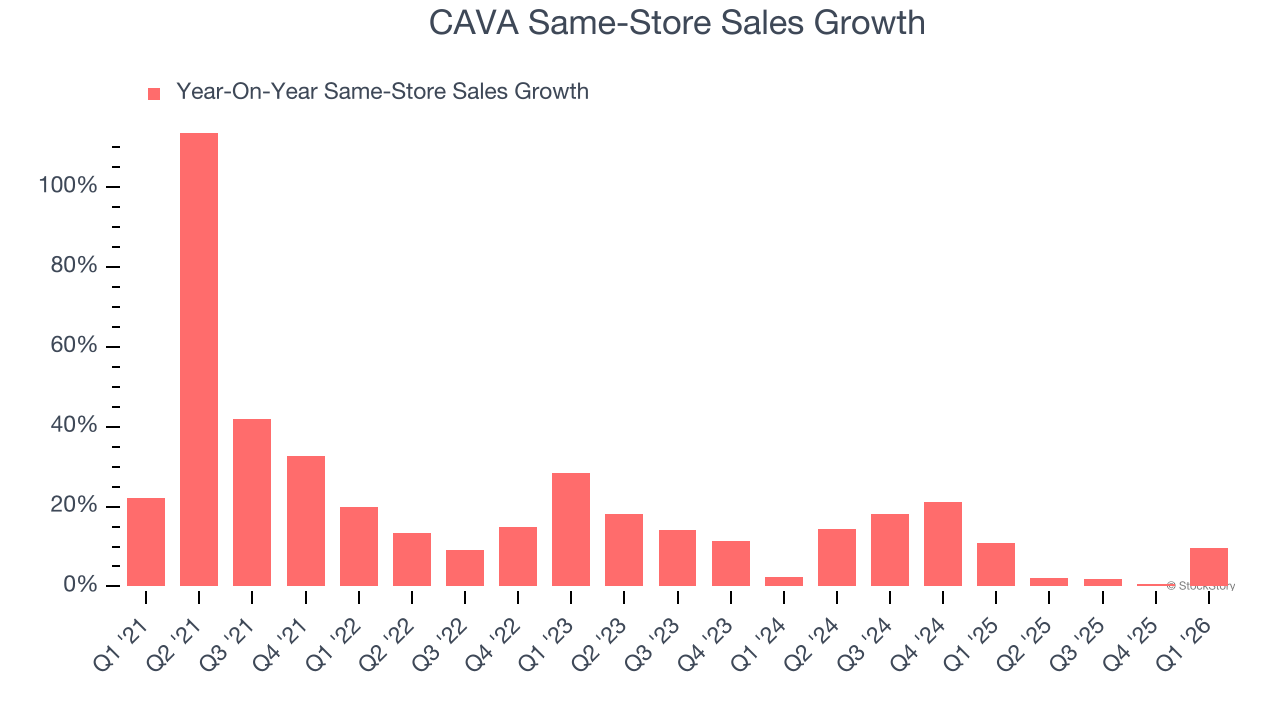

- Same-Store Sales rose 9.7% year on year (10.8% in the same quarter last year)

- Market Capitalization: $9.3 billion

“Amid today's broader macroeconomic environment and geopolitical uncertainty, our first quarter results reflect our position as a clear industry leader and our ability to meet the moment for the modern consumer," said Brett Schulman, Co-Founder and CEO.

Company Overview

Starting from a single Washington, D.C. location, CAVA (NYSE: CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.29 billion in revenue over the past 12 months, CAVA is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, CAVA’s 25.3% annualized revenue growth over the last four years was incredible as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, CAVA reported wonderful year-on-year revenue growth of 32.1%, and its $438.3 million of revenue exceeded Wall Street’s estimates by 4.7%.

Looking ahead, sell-side analysts expect revenue to grow 20.5% over the next 12 months, a deceleration versus the last four years. Still, this projection is admirable and suggests the market is baking in success for its menu offerings.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Restaurant Performance

Number of Restaurants

A restaurant chain’s total number of dining locations influences how much it can sell and how quickly revenue can grow.

CAVA operated 459 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 18.4% annual growth, much faster than the broader restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth at restaurants open for at least a year.

CAVA has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 9.8%. This performance along with its meaningful buildout of new restaurants suggest it’s playing some aggressive offense.

In the latest quarter, CAVA’s same-store sales rose 9.7% year on year. This performance was more or less in line with its historical levels.

Key Takeaways from CAVA’s Q1 Results

We were impressed by how significantly CAVA blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 5.7% to $82.58 immediately following the results.

CAVA had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).