E-commerce florist and gift retailer 1-800-FLOWERS (NASDAQ: FLWS) met Wall Street’s revenue expectations in Q1 CY2026, but sales fell by 11.6% year on year to $293 million. Its non-GAAP loss of $0.77 per share was 13.2% below analysts’ consensus estimates.

Is now the time to buy 1-800-FLOWERS? Find out by accessing our full research report, it’s free.

1-800-FLOWERS (FLWS) Q1 CY2026 Highlights:

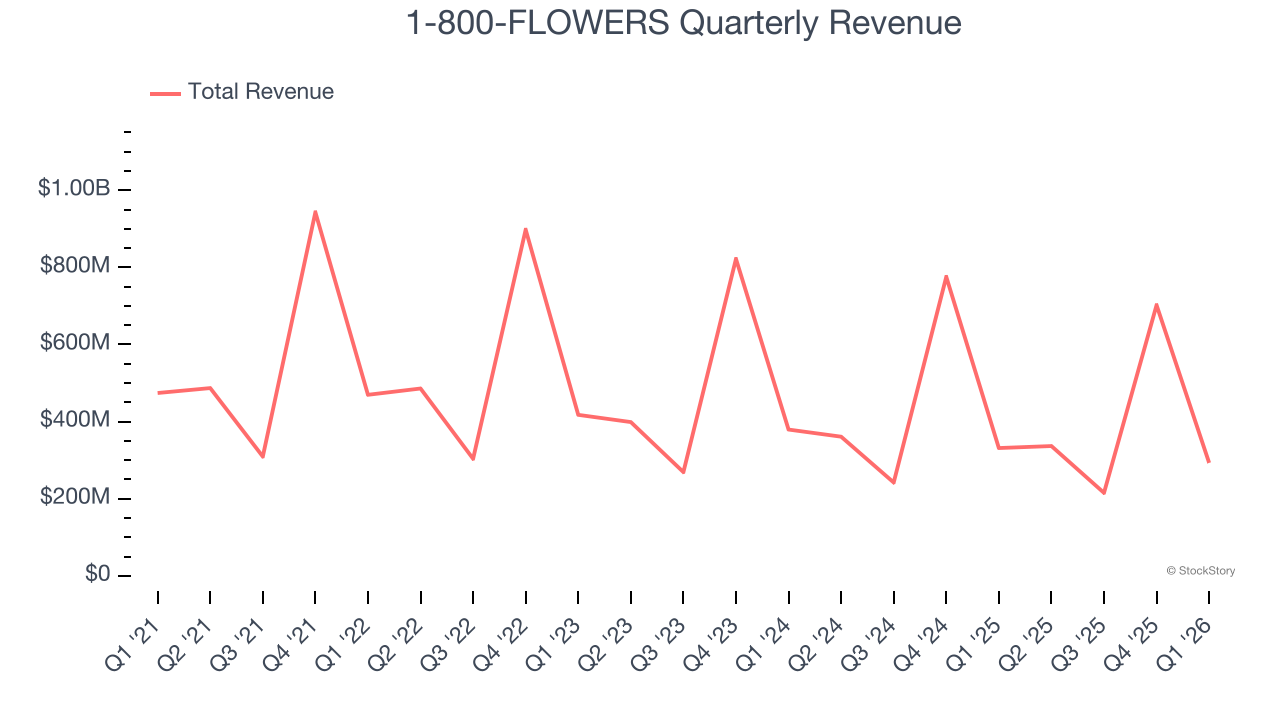

- Revenue: $293 million vs analyst estimates of $294 million (11.6% year-on-year decline, in line)

- Adjusted EPS: -$0.77 vs analyst expectations of -$0.68 (13.2% miss)

- Adjusted EBITDA: -$31.22 million (-10.7% margin, 10.6% year-on-year growth)

- Operating Margin: -32.3%, down from -17.2% in the same quarter last year

- Free Cash Flow was -$136.6 million compared to -$160 million in the same quarter last year

- Market Capitalization: $251.8 million

Company Overview

Founded in 1976, 1-800-FLOWERS (NASDAQ: FLWS) is an online retailer of flowers, gifts, and gourmet foods, serving customers globally.

Revenue Growth

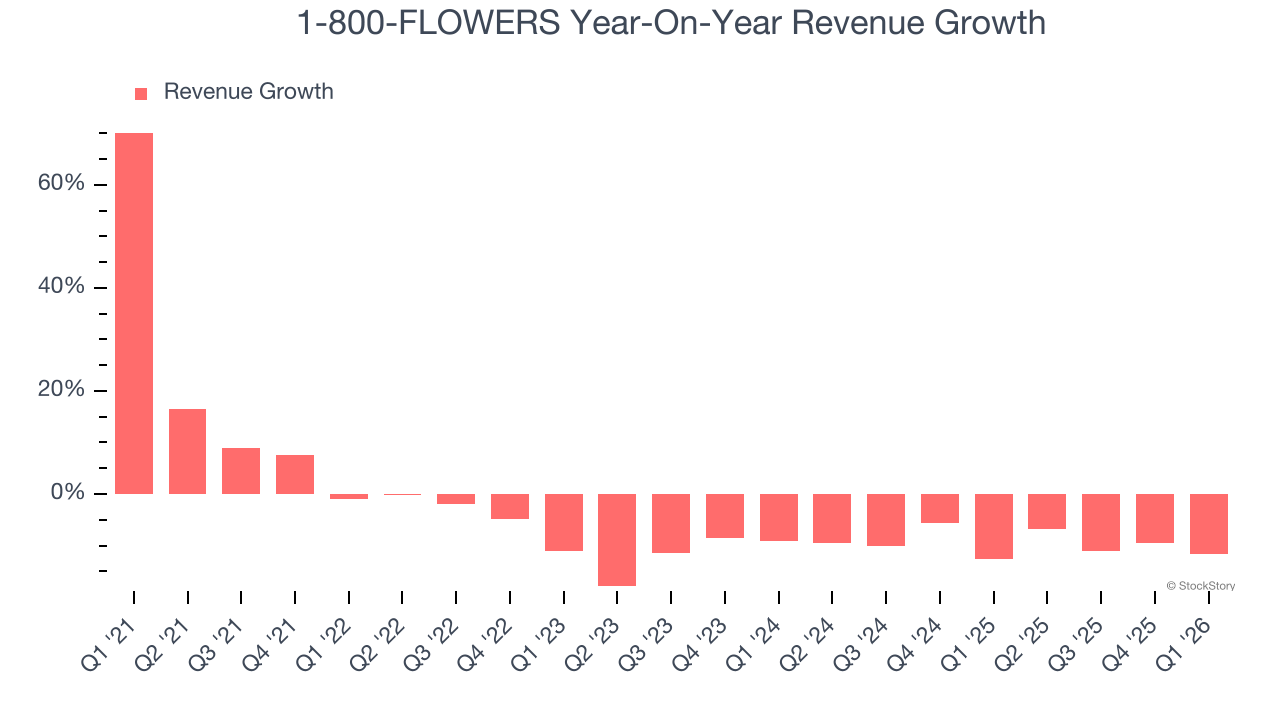

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. 1-800-FLOWERS’s demand was weak over the last five years as its sales fell at a 5.5% annual rate. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. 1-800-FLOWERS’s recent performance shows its demand remained suppressed as its revenue has declined by 9% annually over the last two years.

This quarter, 1-800-FLOWERS reported a rather uninspiring 11.6% year-on-year revenue decline to $293 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

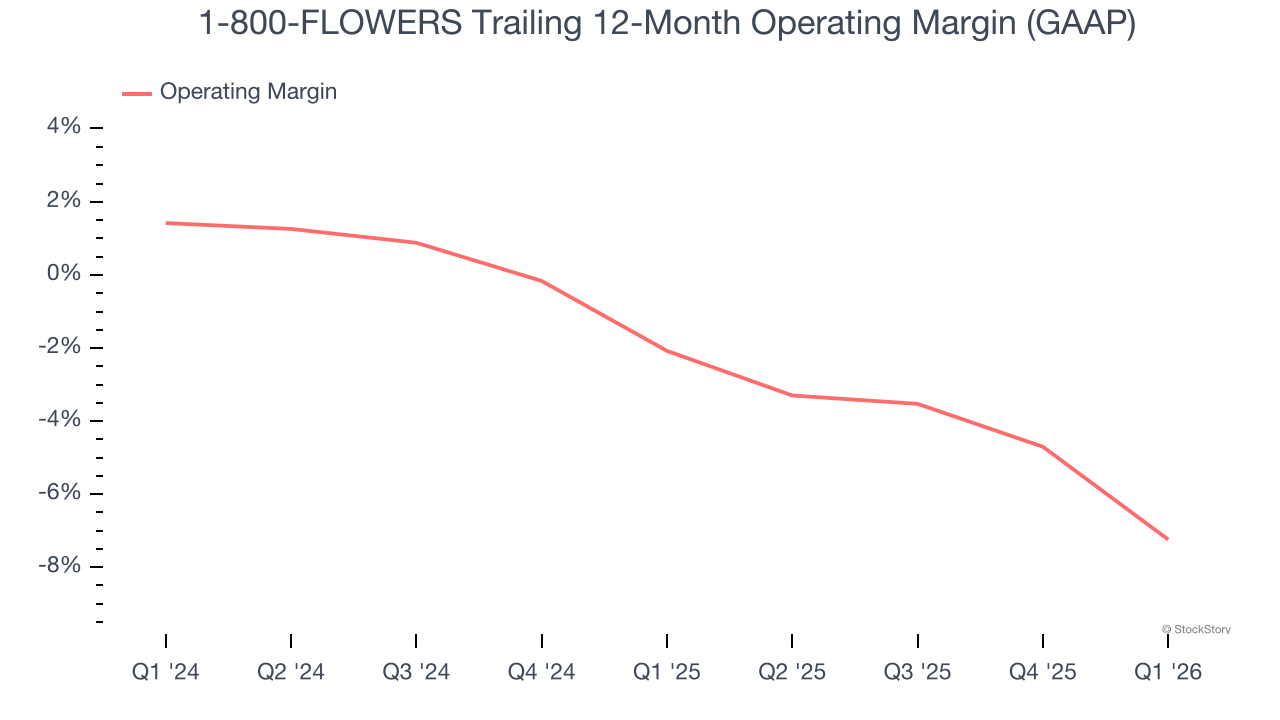

Operating Margin

1-800-FLOWERS’s operating margin has shrunk over the last 12 months and averaged negative 4.5% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

In Q1, 1-800-FLOWERS generated a negative 32.3% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

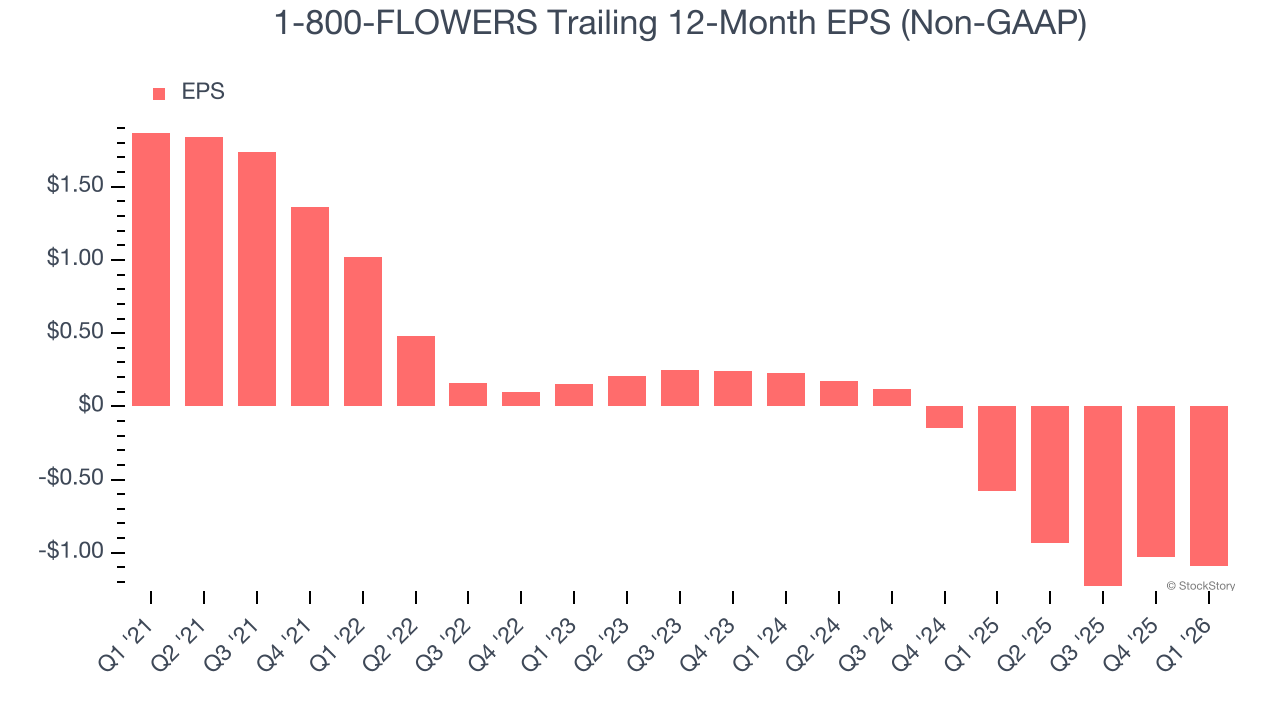

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for 1-800-FLOWERS, its EPS declined by 20.9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q1, 1-800-FLOWERS reported adjusted EPS of negative $0.77, down from negative $0.71 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects 1-800-FLOWERS to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.09 will advance to negative $0.38.

Key Takeaways from 1-800-FLOWERS’s Q1 Results

It was encouraging to see 1-800-FLOWERS beat analysts’ EBITDA expectations this quarter. On the other hand, its adjusted operating income missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 3.6% to $3.65 immediately following the results.

1-800-FLOWERS’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).