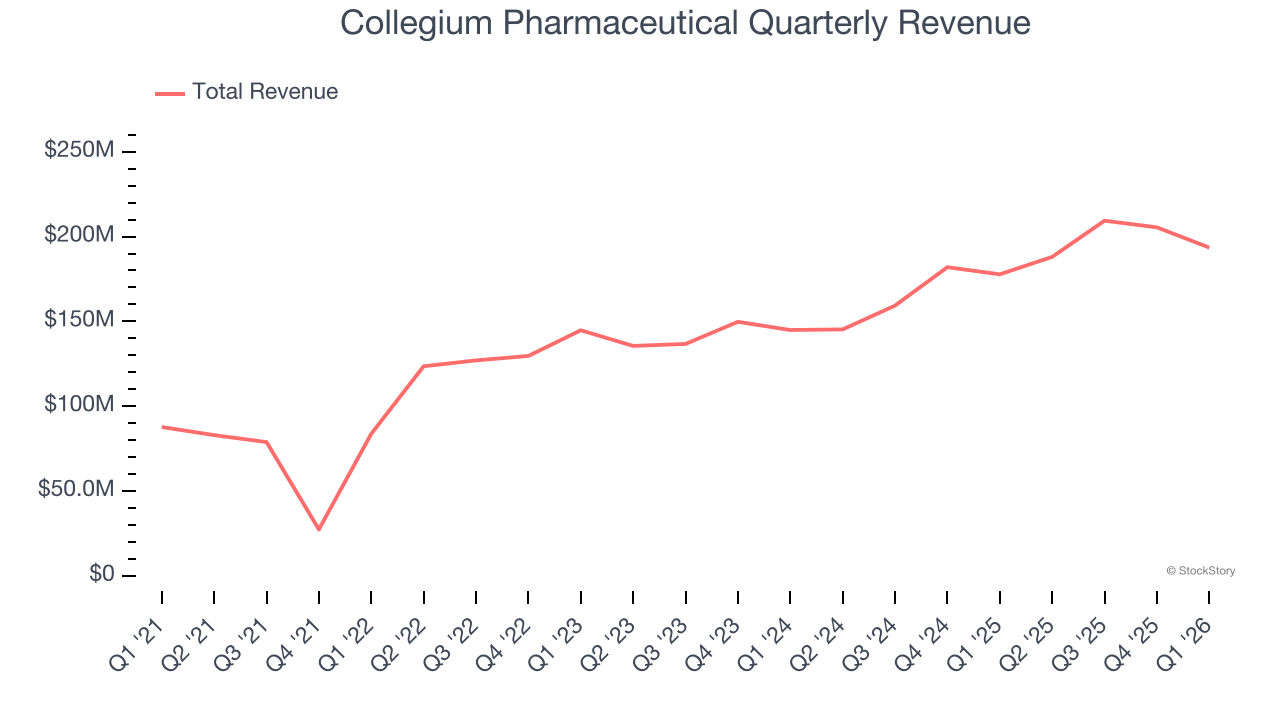

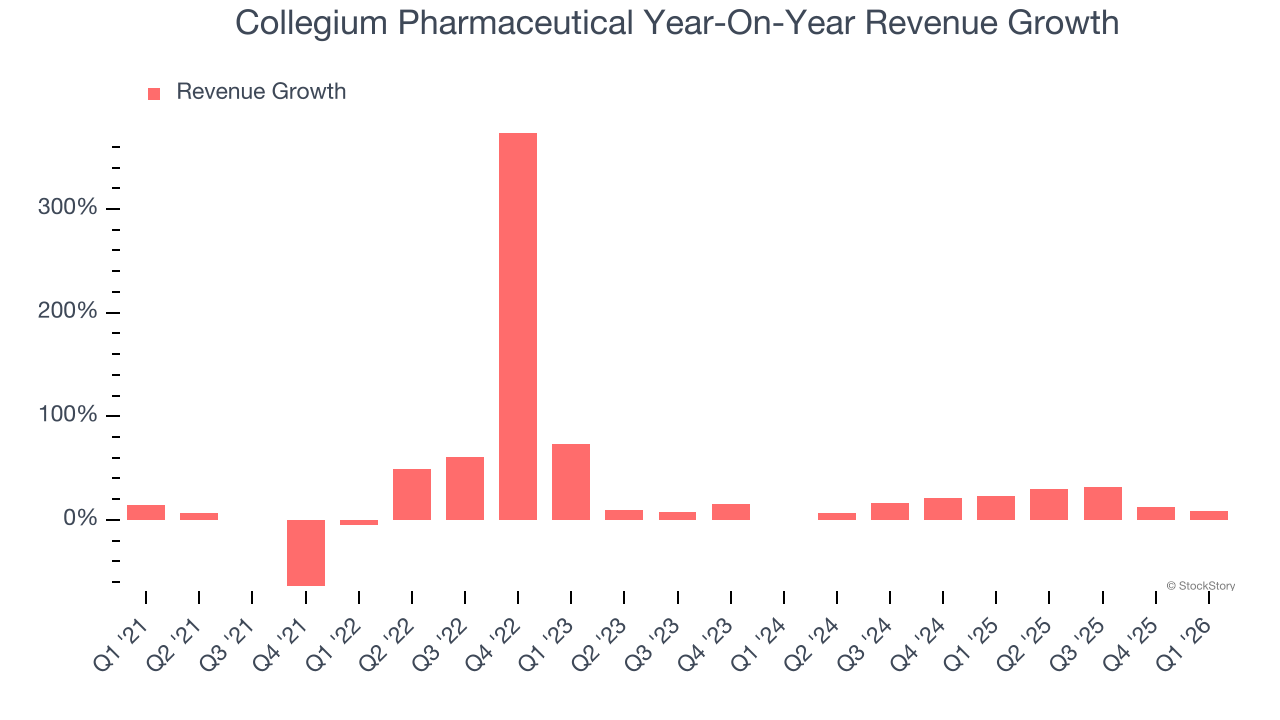

Pharmaceutical company Collegium Pharmaceutical (NASDAQ: COLL) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 8.9% year on year to $193.5 million. On the other hand, the company’s full-year revenue guidance of $815 million at the midpoint came in 2.9% below analysts’ estimates. Its non-GAAP profit of $1.76 per share was 15.5% above analysts’ consensus estimates.

Is now the time to buy Collegium Pharmaceutical? Find out by accessing our full research report, it’s free.

Collegium Pharmaceutical (COLL) Q1 CY2026 Highlights:

- Revenue: $193.5 million vs analyst estimates of $184.5 million (8.9% year-on-year growth, 4.9% beat)

- Adjusted EPS: $1.76 vs analyst estimates of $1.52 (15.5% beat)

- Adjusted EBITDA: $103.9 million vs analyst estimates of $101.7 million (53.7% margin, 2.1% beat)

- The company reconfirmed its revenue guidance for the full year of $815 million at the midpoint

- EBITDA guidance for the full year is $465 million at the midpoint, in line with analyst expectations

- Operating Margin: 16%, up from 12.2% in the same quarter last year

- Market Capitalization: $1.18 billion

“In the first quarter, we made meaningful progress on our 2026 strategic priorities, including delivering strong performance for JORNAY PM and continued durability from our pain portfolio” said Vikram Karnani, President and Chief Executive Officer.

Company Overview

Pioneering abuse-deterrent technology in a field plagued by addiction concerns, Collegium Pharmaceutical (NASDAQ: COLL) develops and markets specialty medications for treating moderate to severe pain, including abuse-deterrent opioid formulations.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Collegium Pharmaceutical grew its sales at an impressive 19.9% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Collegium Pharmaceutical’s annualized revenue growth of 18.5% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Collegium Pharmaceutical reported year-on-year revenue growth of 8.9%, and its $193.5 million of revenue exceeded Wall Street’s estimates by 4.9%.

Looking ahead, sell-side analysts expect revenue to grow 6.1% over the next 12 months, a deceleration versus the last two years. Still, this projection is above the sector average and implies the market sees some success for its newer products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

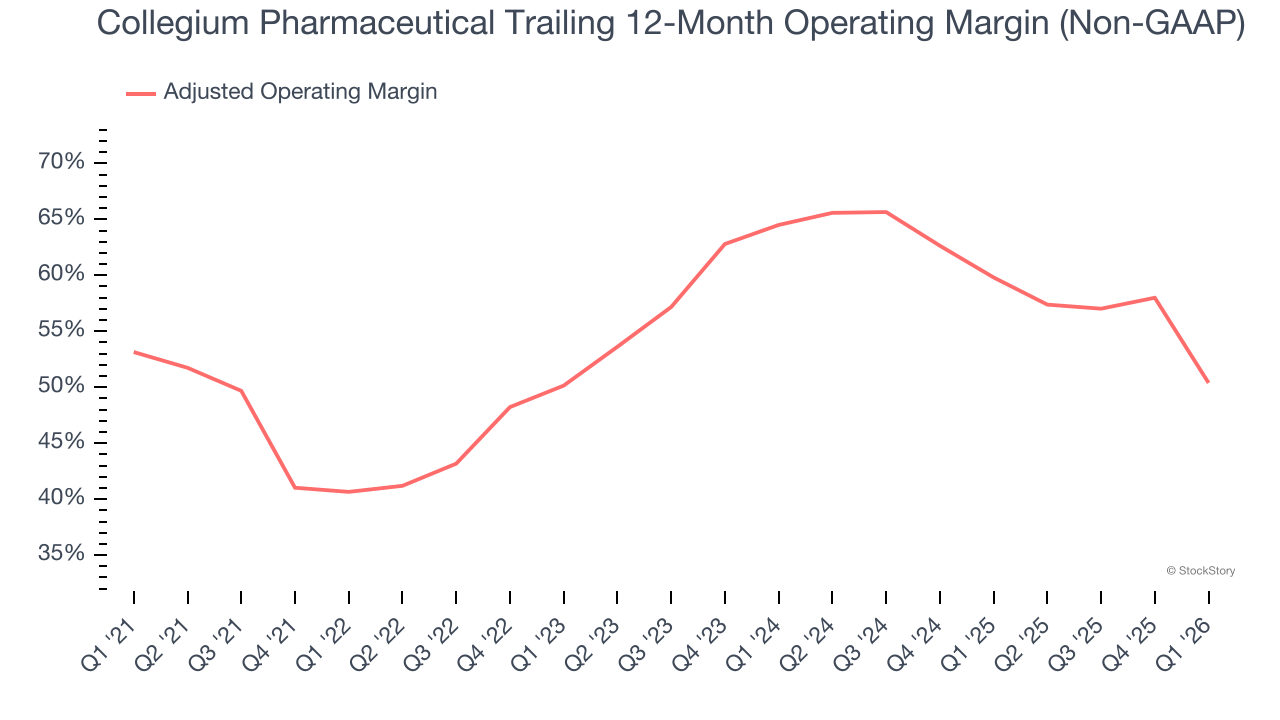

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Collegium Pharmaceutical has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 54.5%.

Looking at the trend in its profitability, Collegium Pharmaceutical’s adjusted operating margin rose by 9.7 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming into its more recent performance, however, we can see the company’s margin has decreased by 14.1 percentage points on a two-year basis. If Collegium Pharmaceutical wants to pass our bar, it must prove it can expand its profitability consistently.

This quarter, Collegium Pharmaceutical generated an adjusted operating margin profit margin of 21.6%, down 30.8 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

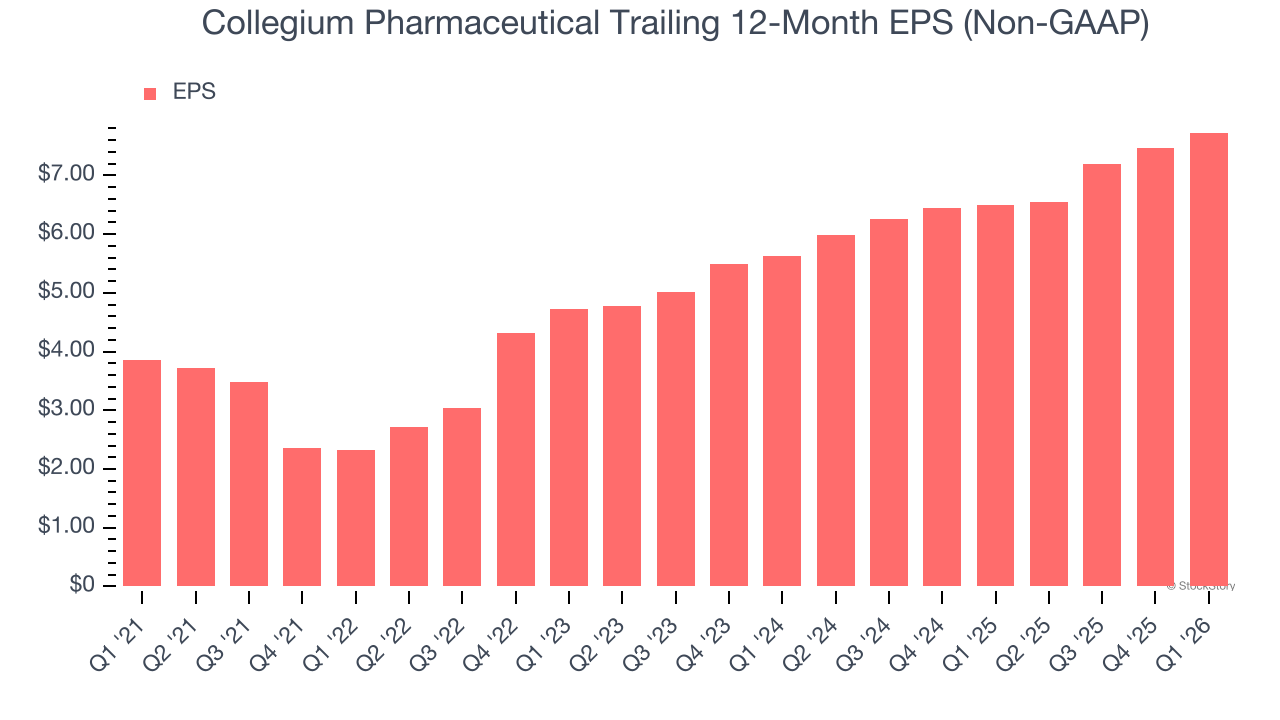

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Collegium Pharmaceutical’s EPS grew at a spectacular 14.9% compounded annual growth rate over the last five years. Despite its adjusted operating margin improvement and share repurchases during that time, this performance was lower than its 19.9% annualized revenue growth, telling us the delta came from reduced interest expenses or taxes.

In Q1, Collegium Pharmaceutical reported adjusted EPS of $1.76, up from $1.49 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Collegium Pharmaceutical’s Q1 Results

We enjoyed seeing Collegium Pharmaceutical beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed. Overall, this print had some key positives. The stock traded up 7.9% to $39.46 immediately after reporting.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).