Clothing company Kontoor Brands (NYSE: KTB) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 29.7% year on year to $808 million. The company expects the full year’s revenue to be around $3.44 billion, close to analysts’ estimates. Its non-GAAP profit of $1.06 per share was 7.1% below analysts’ consensus estimates.

Is now the time to buy Kontoor Brands? Find out by accessing our full research report, it’s free.

Kontoor Brands (KTB) Q1 CY2026 Highlights:

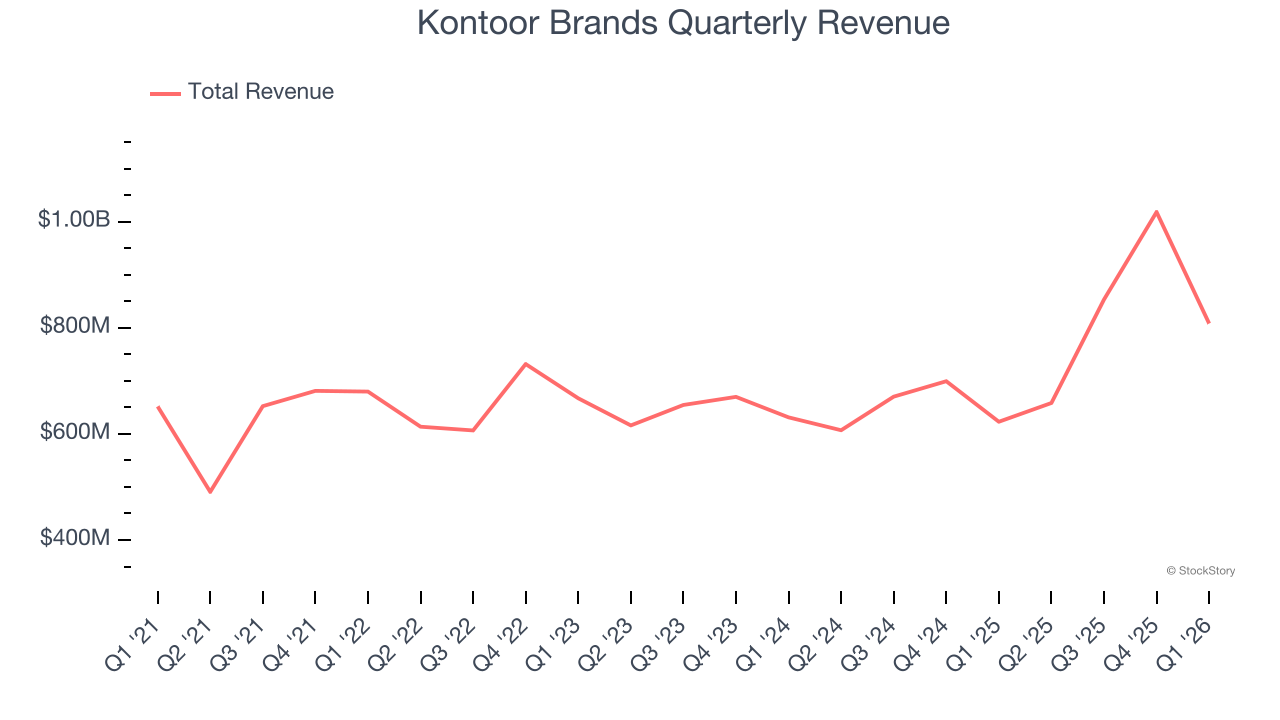

- Revenue: $808 million vs analyst estimates of $779 million (29.7% year-on-year growth, 3.7% beat)

- Adjusted EPS: $1.06 vs analyst expectations of $1.14 (7.1% miss)

- Adjusted EBITDA: $103.4 million vs analyst estimates of $114.2 million (12.8% margin, 9.4% miss)

- The company slightly lifted its revenue guidance for the full year to $3.44 billion at the midpoint from $3.43 billion

- Management raised its full-year Adjusted EPS guidance to $6.65 at the midpoint, a 3.1% increase

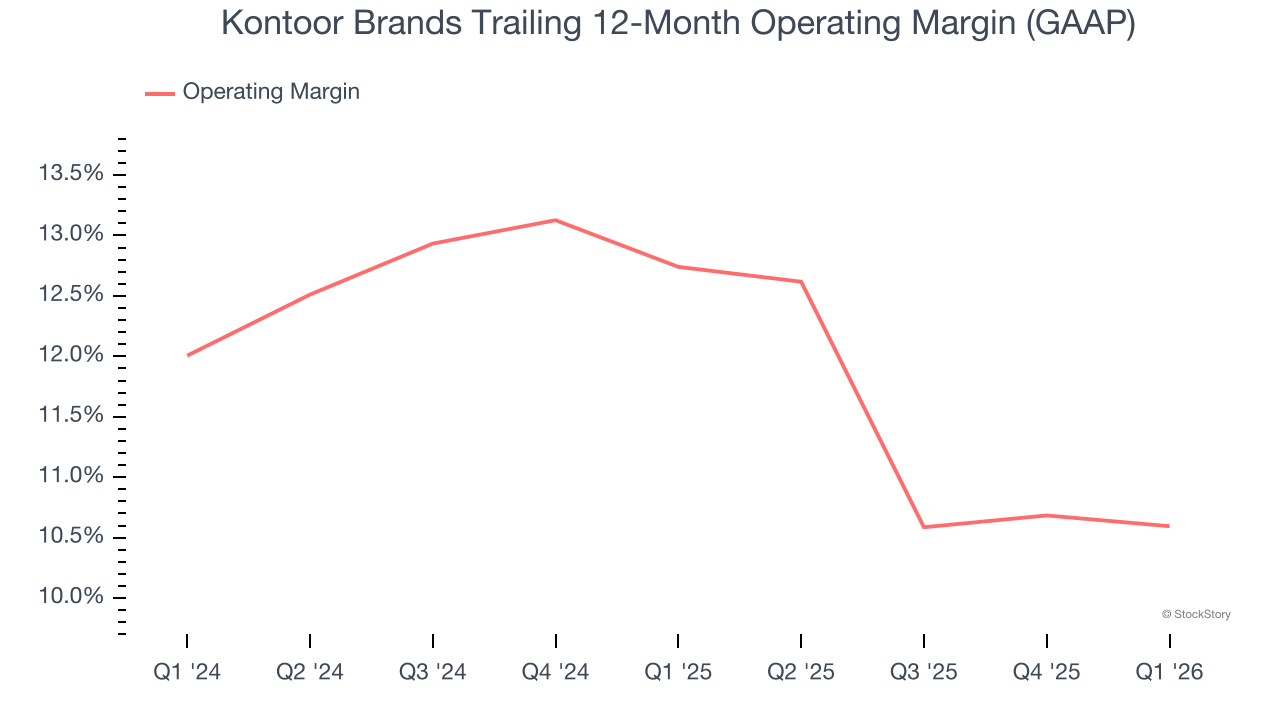

- Operating Margin: 11.2%, in line with the same quarter last year

- Free Cash Flow Margin: 4.7%, down from 12% in the same quarter last year

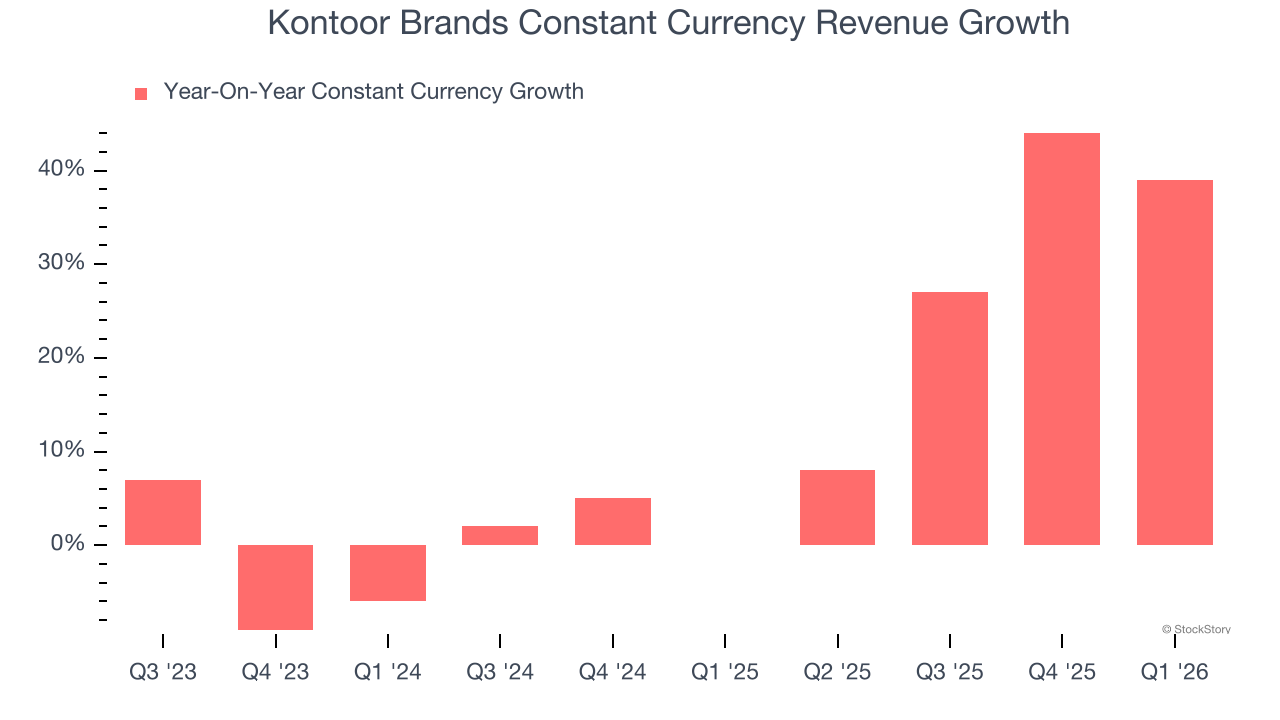

- Constant Currency Revenue rose 39% year on year (0% in the same quarter last year)

- Market Capitalization: $4.14 billion

Company Overview

Founded in 2019 after separating from VF Corporation, Kontoor Brands (NYSE: KTB) is a clothing company known for its high-quality denim products.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Kontoor Brands’s 8.3% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Kontoor Brands’s annualized revenue growth of 13.9% over the last two years is above its five-year trend, which is encouraging.

Kontoor Brands also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 17.9% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Kontoor Brands.

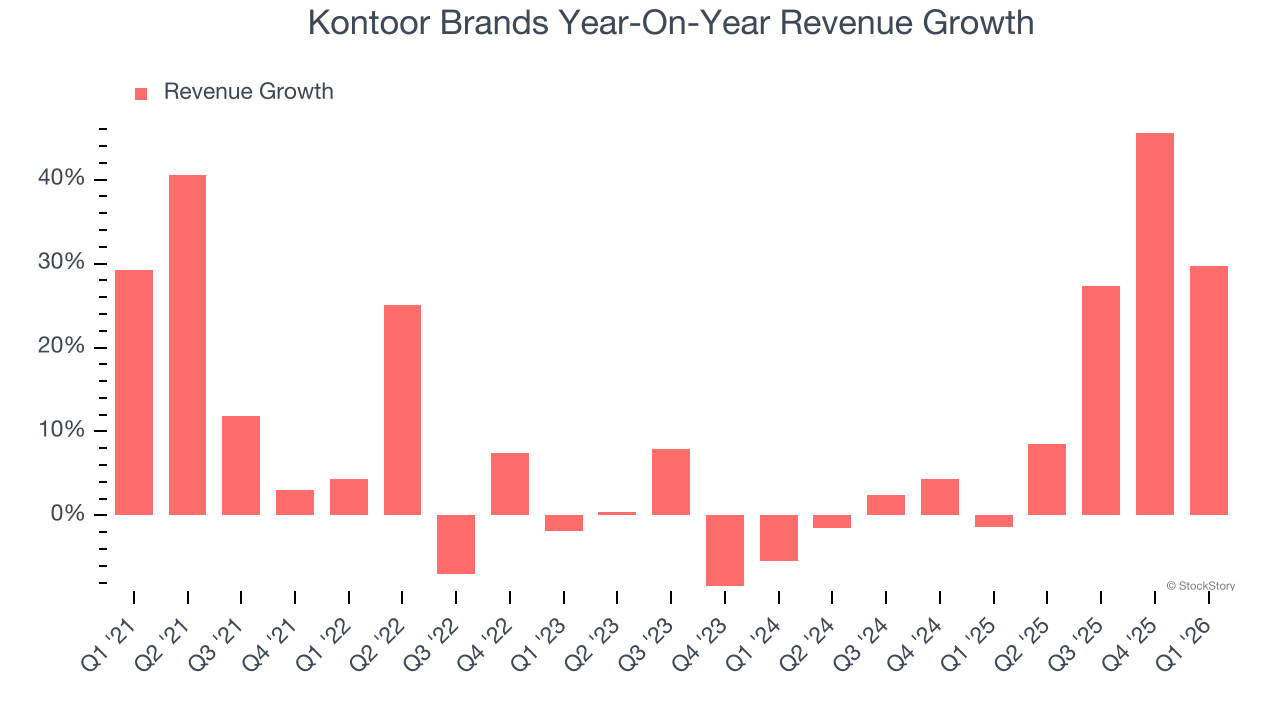

This quarter, Kontoor Brands reported robust year-on-year revenue growth of 29.7%, and its $808 million of revenue topped Wall Street estimates by 3.7%.

Looking ahead, sell-side analysts expect revenue to grow 4.3% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Kontoor Brands’s operating margin has been trending down over the last 12 months and averaged 11.5% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Kontoor Brands generated an operating margin profit margin of 11.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

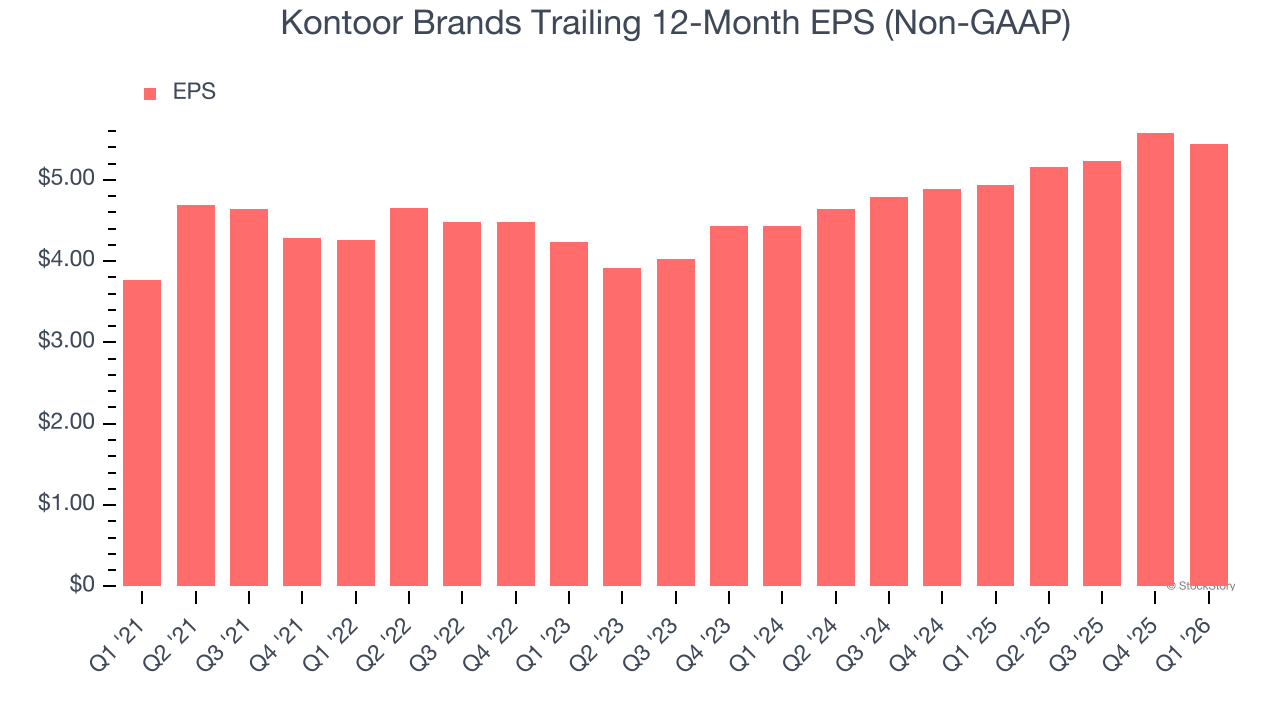

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Kontoor Brands’s weak 7.6% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Kontoor Brands reported adjusted EPS of $1.06, down from $1.20 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Kontoor Brands’s full-year EPS of $5.44 to grow 22.5%.

Key Takeaways from Kontoor Brands’s Q1 Results

It was encouraging to see Kontoor Brands beat analysts’ revenue expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. On the other hand, its EPS missed. Overall, this was still a solid quarter. The stock traded up 6.7% to $80.04 immediately following the results.

Is Kontoor Brands an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).