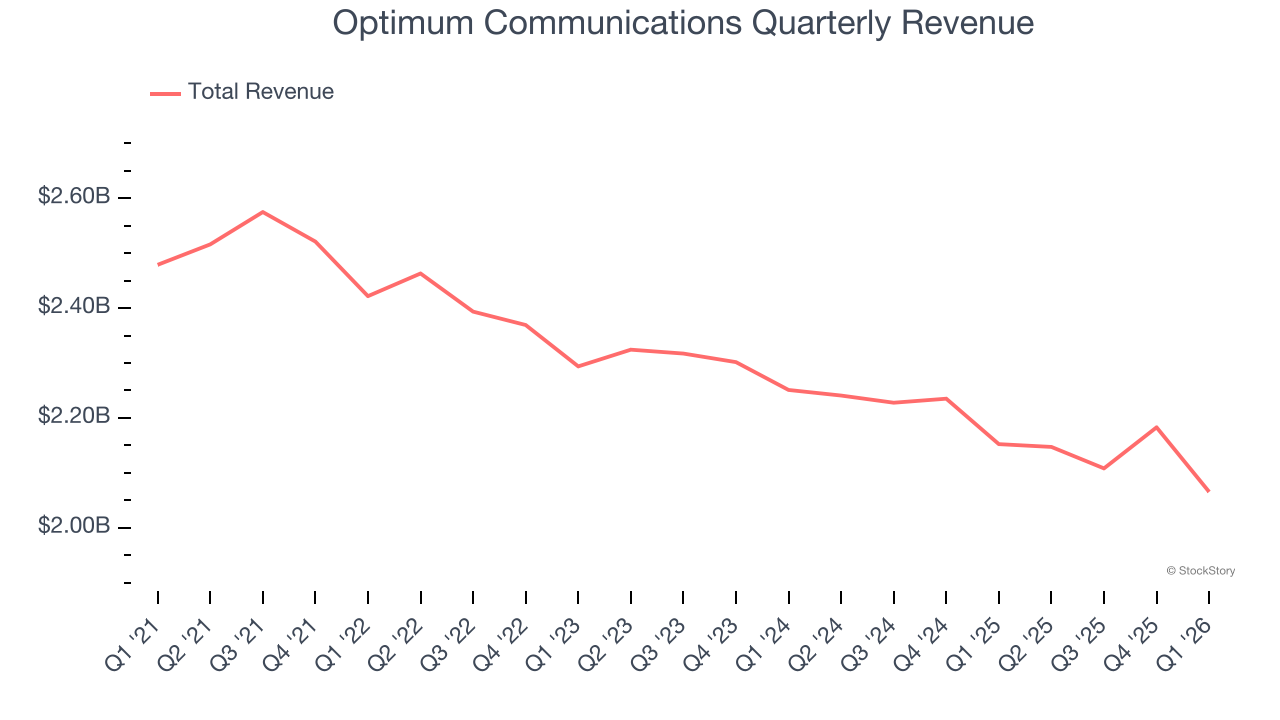

Telecommunications and cable services provider Optimum Communications (NYSE: OPTU) met Wall Street’s revenue expectations in Q1 CY2026, but sales fell by 4% year on year to $2.07 billion. Its GAAP loss of $6.10 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Optimum Communications? Find out by accessing our full research report, it’s free.

Optimum Communications (OPTU) Q1 CY2026 Highlights:

- Revenue: $2.07 billion vs analyst estimates of $2.07 billion (4% year-on-year decline, in line)

- EPS (GAAP): -$6.10 vs analyst estimates of -$0.14 (significant miss)

- Adjusted EBITDA: $789 million vs analyst estimates of $811.7 million (38.2% margin, 2.8% miss)

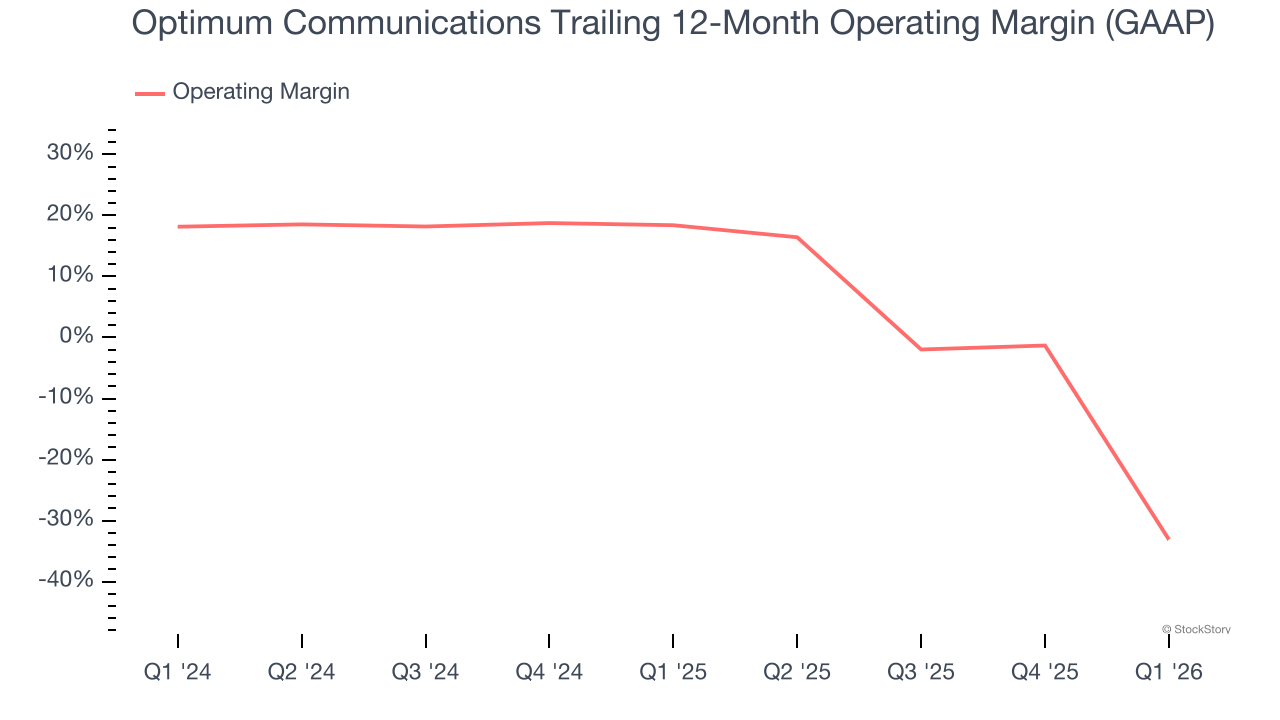

- Operating Margin: -114%, down from 16% in the same quarter last year

- Free Cash Flow was -$137.4 million compared to -$168.6 million in the same quarter last year

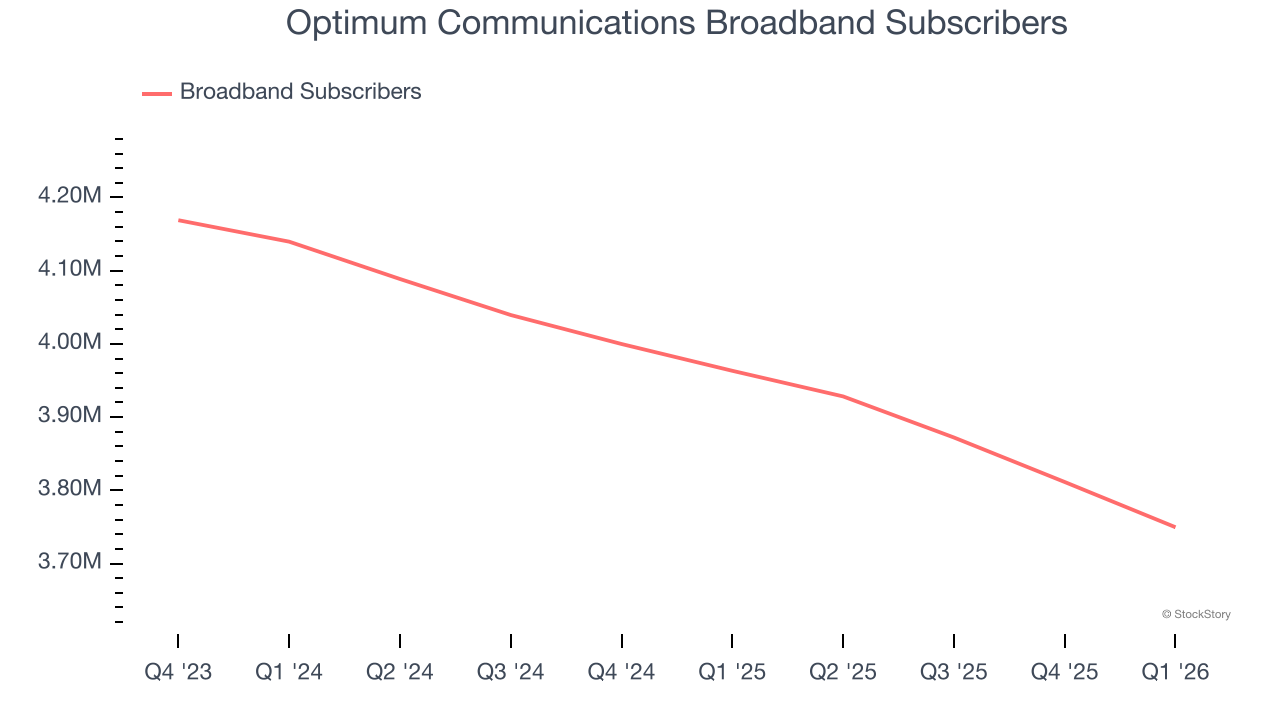

- Broadband Subscribers: down 213,700 year on year

- Market Capitalization: $649.2 million

Company Overview

Based in Long Island City, Optimum Communications (NYSE: OPTU) is a telecommunications company offering cable, internet, telephone, and television services across the United States.

Revenue Growth

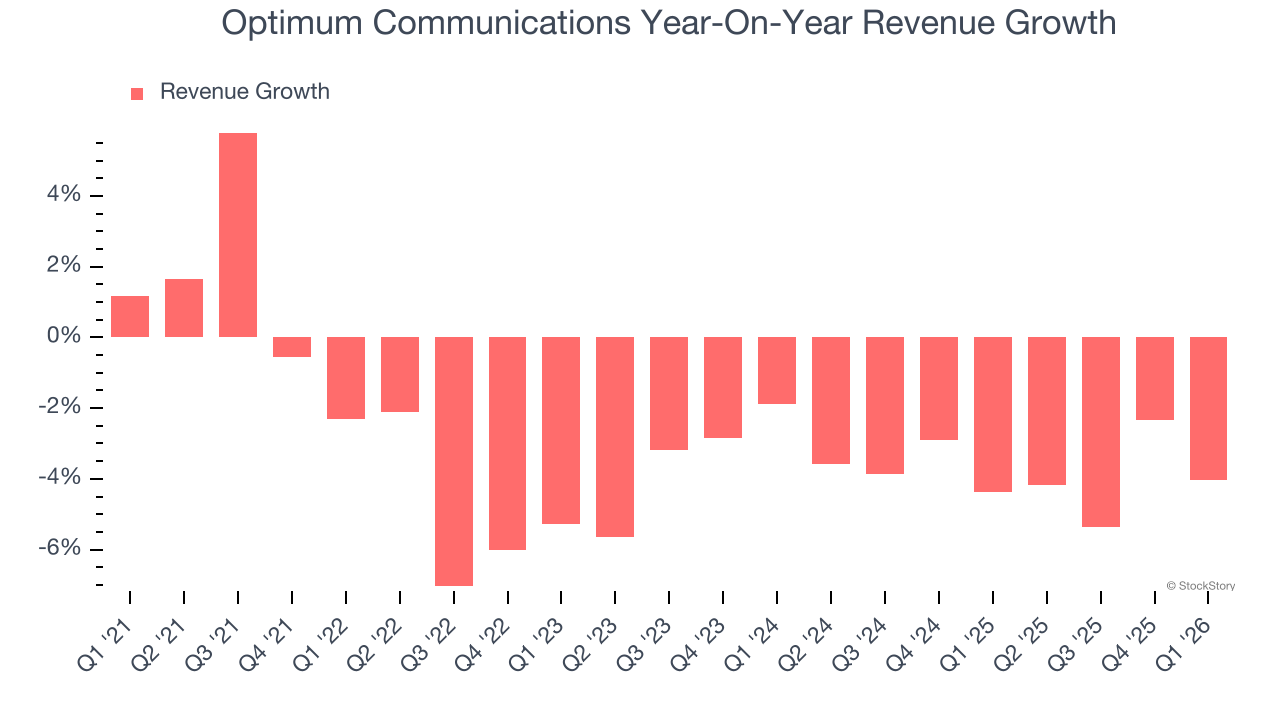

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Optimum Communications struggled to consistently generate demand over the last five years as its sales dropped at a 3% annual rate. This wasn’t a great result and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Optimum Communications’s annualized revenue declines of 3.8% over the last two years align with its five-year trend, suggesting its demand has consistently shrunk.

Optimum Communications also discloses its number of broadband subscribers and pay tv subscribers, which clocked in at 3.75 million and 1.57 million in the latest quarter. Over the last two years, Optimum Communications’s broadband subscribers averaged 4.4% year-on-year declines while its pay tv subscribers averaged 13.6% year-on-year declines.

This quarter, Optimum Communications reported a rather uninspiring 4% year-on-year revenue decline to $2.07 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 4% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not catalyze better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Optimum Communications’s operating margin has been trending down over the last 12 months and averaged negative 6.8% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

Optimum Communications’s operating margin was negative 114% this quarter. The company's consistent lack of profits raise a flag.

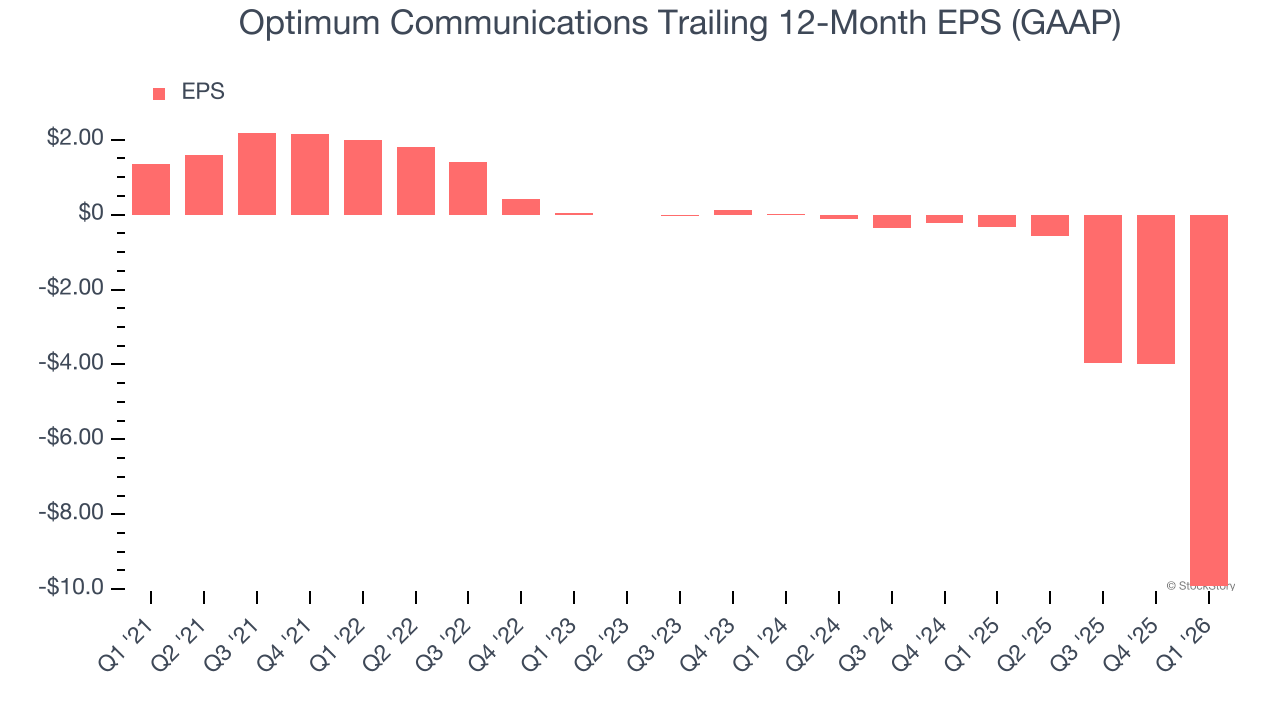

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Optimum Communications, its EPS declined by 56.2% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q1, Optimum Communications reported EPS of negative $6.10, down from negative $0.16 in the same quarter last year. This print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Optimum Communications’s Q1 Results

We struggled to find many positives in these results. Its adjusted operating income missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.5% to $1.35 immediately after reporting.

Optimum Communications’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).