Egg and butter company Vital Farms (NASDAQ: VITL) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 15.4% year on year to $187.2 million. On the other hand, the company’s full-year revenue guidance of $787.5 million at the midpoint came in 9.6% below analysts’ estimates. Its GAAP loss of $0.03 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Vital Farms? Find out by accessing our full research report, it’s free.

Vital Farms (VITL) Q1 CY2026 Highlights:

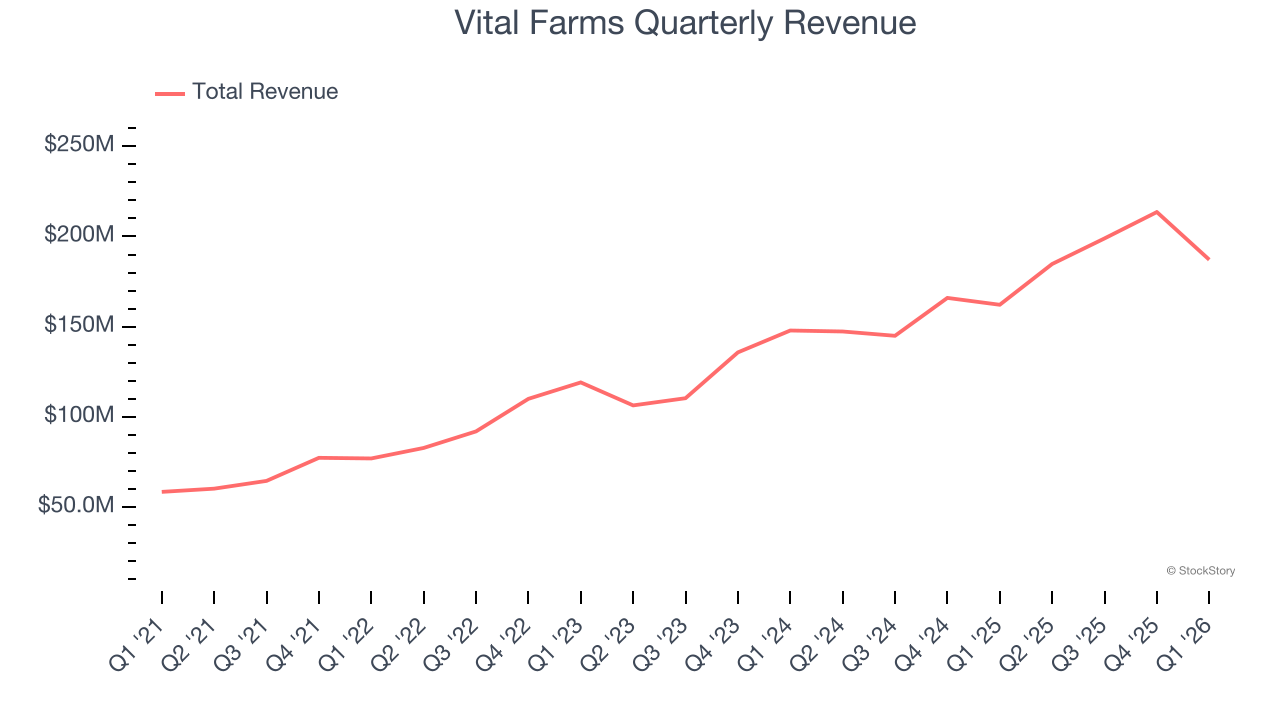

- Revenue: $187.2 million vs analyst estimates of $183.1 million (15.4% year-on-year growth, 2.2% beat)

- EPS (GAAP): -$0.03 vs analyst estimates of $0.05 (significant miss)

- Adjusted EBITDA: $5.02 million vs analyst estimates of $10.35 million (2.7% margin, 51.5% miss)

- The company dropped its revenue guidance for the full year to $787.5 million at the midpoint from $910 million, a 13.5% decrease

- EBITDA guidance for the full year is $5 million at the midpoint, below analyst estimates of $81.07 million

- Operating Margin: -1.2%, down from 13.4% in the same quarter last year

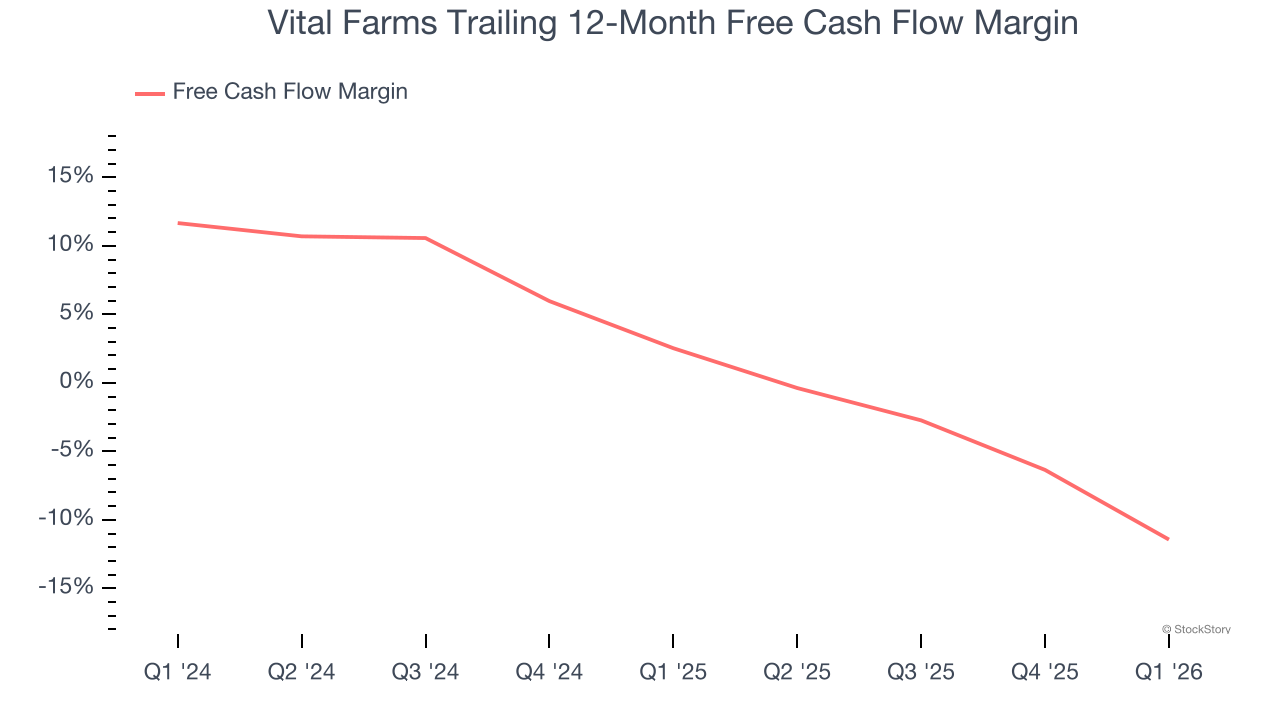

- Free Cash Flow was -$39.31 million, down from $2.15 million in the same quarter last year

- Market Capitalization: $514.2 million

Company Overview

With an emphasis on ethically produced products, Vital Farms (NASDAQ: VITL) specializes in pasture-raised eggs and butter.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $784.4 million in revenue over the past 12 months, Vital Farms is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

As you can see below, Vital Farms’s sales grew at an excellent 24.7% compounded annual growth rate over the last three years. This shows it had high demand, a useful starting point for our analysis.

This quarter, Vital Farms reported year-on-year revenue growth of 15.4%, and its $187.2 million of revenue exceeded Wall Street’s estimates by 2.2%.

Looking ahead, sell-side analysts expect revenue to grow 14.8% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is noteworthy and indicates the market is forecasting success for its products.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Vital Farms’s demanding reinvestments have consumed many resources over the last two years, contributing to an average free cash flow margin of negative 5.3%. This means it lit $5.27 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Vital Farms’s margin dropped by 14 percentage points over the last year. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Vital Farms burned through $39.31 million of cash in Q1, equivalent to a negative 21% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

Key Takeaways from Vital Farms’s Q1 Results

It was encouraging to see Vital Farms beat analysts’ revenue expectations this quarter. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 24.2% to $9.11 immediately following the results.

Vital Farms didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).