First Bancorp has had an impressive run over the past six months as its shares have beaten the S&P 500 by 6%. The stock now trades at $60.76, marking a 15% gain. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in First Bancorp, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is First Bancorp Not Exciting?

Despite the momentum, we’re swiping left on First Bancorp for now. Here are three reasons why FBNC doesn’t excite us, plus one stock we’d rather own.

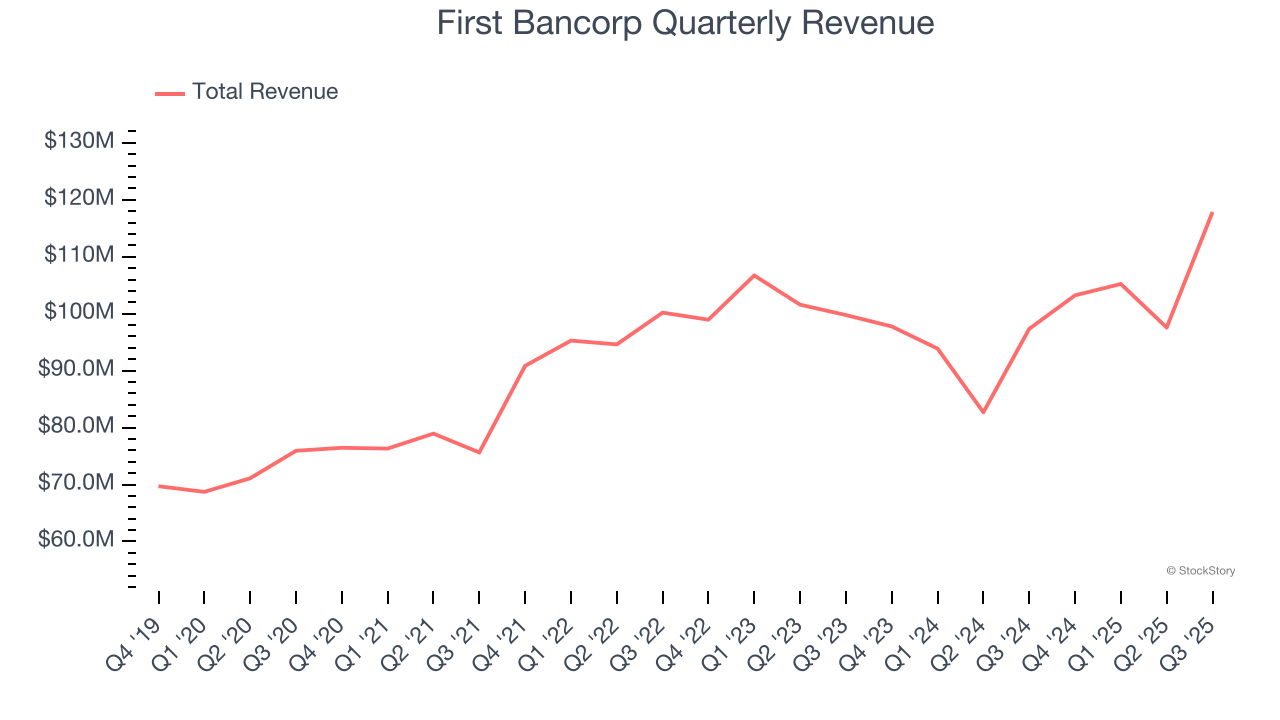

1. Long-Term Revenue Growth Disappoints

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

Regrettably, First Bancorp’s revenue grew at a mediocre 8.2% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector.

2. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect First Bancorp’s net interest income to rise by 4.4%, a deceleration versus its 9.9% annualized growth for the past two years. This projection is below its 9.9% annualized growth rate for the past two years.

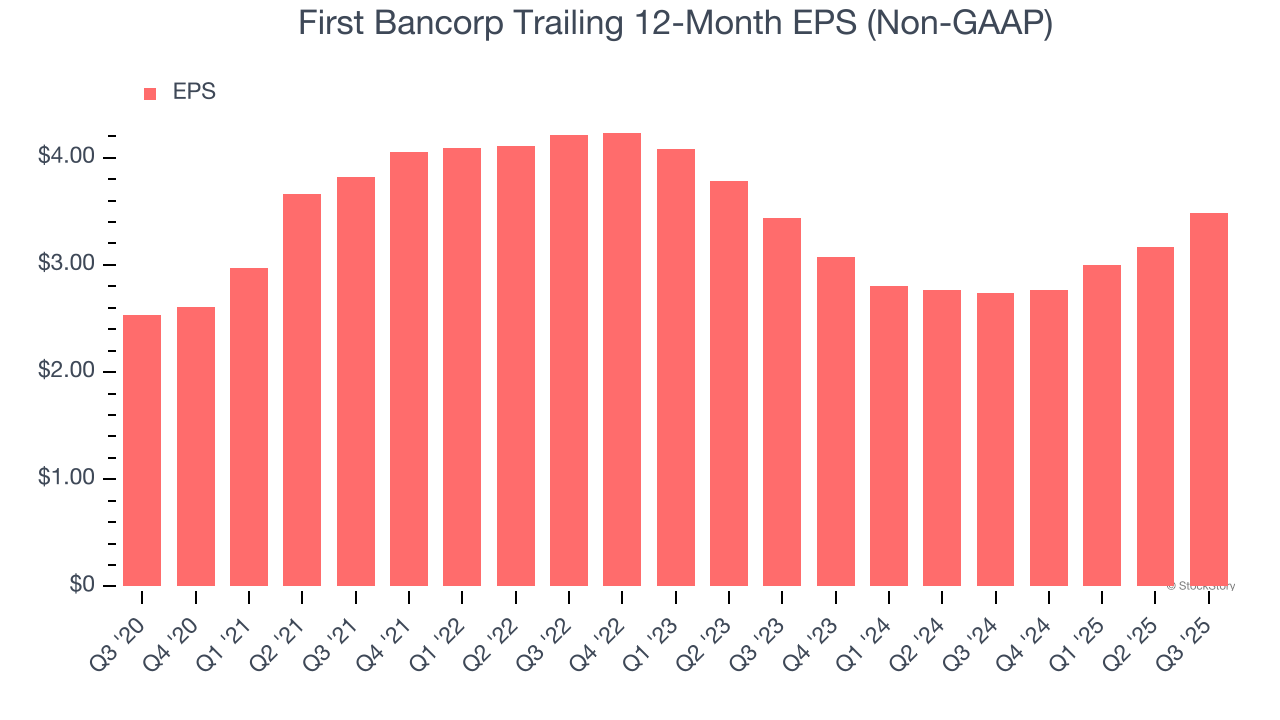

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

First Bancorp’s unimpressive 6.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Final Judgment

First Bancorp isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 1.5× forward P/B (or $60.76 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We’re fairly confident there are better investments elsewhere. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.