Over the past six months, WD-40 has been a great trade, beating the S&P 500 by 14.3%. Its stock price has climbed to $245.90, representing a healthy 20.5% increase. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now still a good time to buy WDFC? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Does WDFC Stock Spark Debate?

Short for “Water Displacement perfected on the 40th try”, WD-40 (NASDAQ: WDFC) is a renowned American consumer goods company known for its iconic and versatile spray, WD-40 Multi-Use Product.

Two Things to Like:

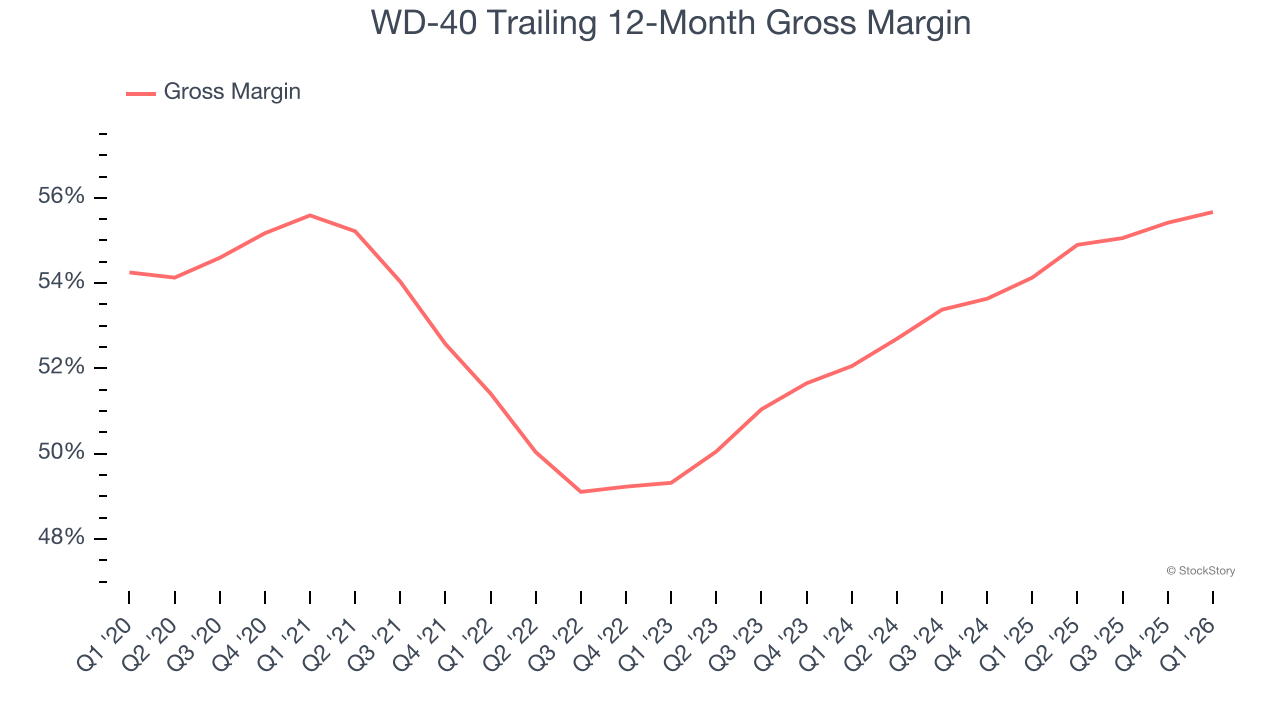

1. Elite Gross Margin Powers Best-In-Class Business Model

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

WD-40 has best-in-class unit economics for a consumer staples company, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 54.9% gross margin over the last two years. That means for every $100 in revenue, only $45.09 went towards paying for raw materials, production of goods, transportation, and distribution.

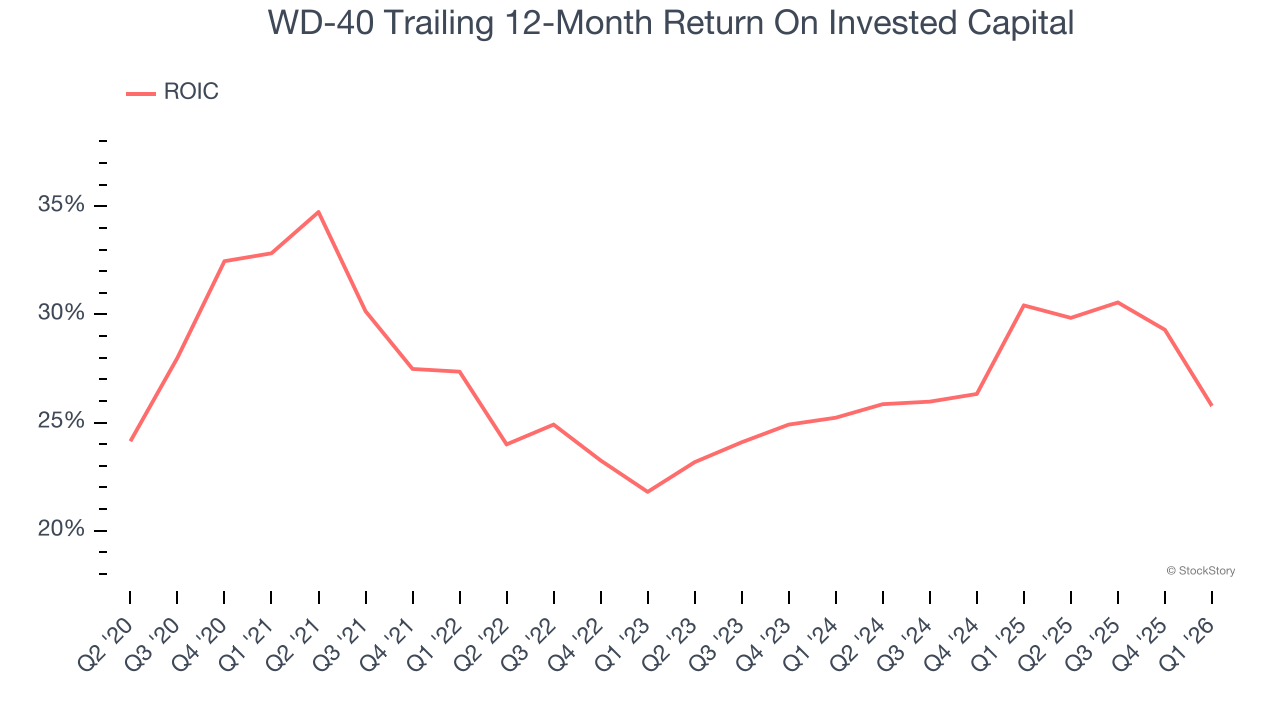

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

WD-40’s five-year average ROIC was 26.1%, placing it among the best consumer staples companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to Be Careful:

Fewer Distribution Channels Limit Its Ceiling

With $636.5 million in revenue over the past 12 months, WD-40 is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers. On the bright side, it can grow faster because it has a longer list of untapped store chains to sell into.

Final Judgment

WD-40’s merits more than compensate for its flaws, and with its shares outperforming the market lately, the stock trades at 39.8× forward P/E (or $245.90 per share). Is now the right time to buy? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.