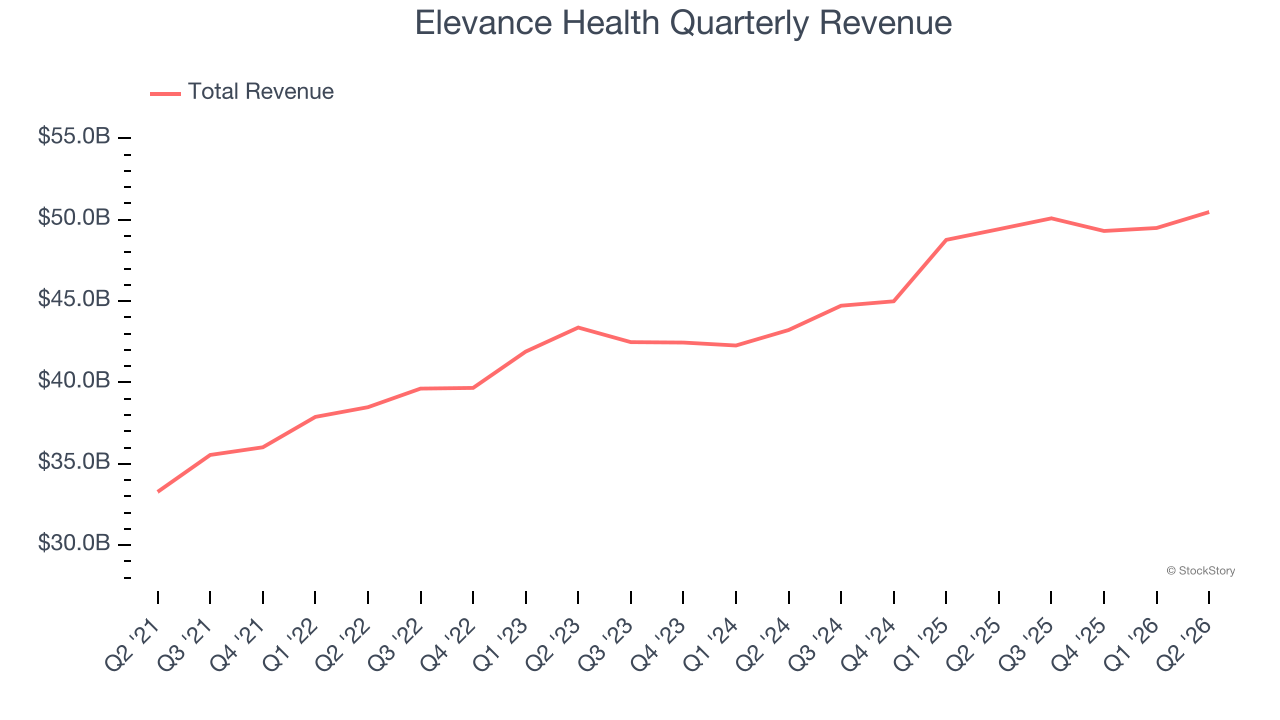

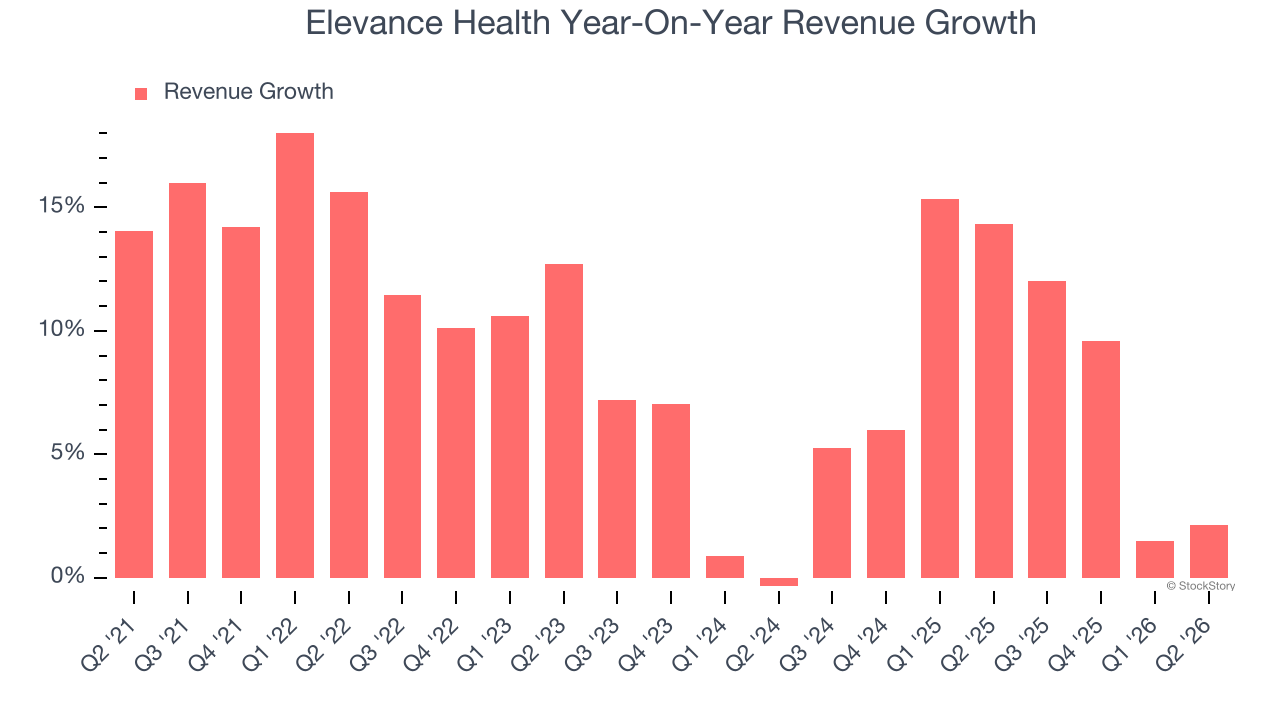

Health insurance provider Elevance Health (NYSE: ELV) reported Q2 CY2026 results beating Wall Street’s revenue expectations, with sales up 2.1% year on year to $50.47 billion. Its non-GAAP profit of $7.45 per share was 20% above analysts’ consensus estimates.

Is now the time to buy Elevance Health? Find out by accessing our full research report, it’s free.

Elevance Health (ELV) Q2 CY2026 Highlights:

- Revenue: $50.47 billion vs analyst estimates of $48.6 billion (2.1% year-on-year growth, 3.9% beat)

- Adjusted EPS: $7.45 vs analyst estimates of $6.21 (20% beat)

- Management slightly raised its full-year Adjusted EPS guidance to $27 at the midpoint

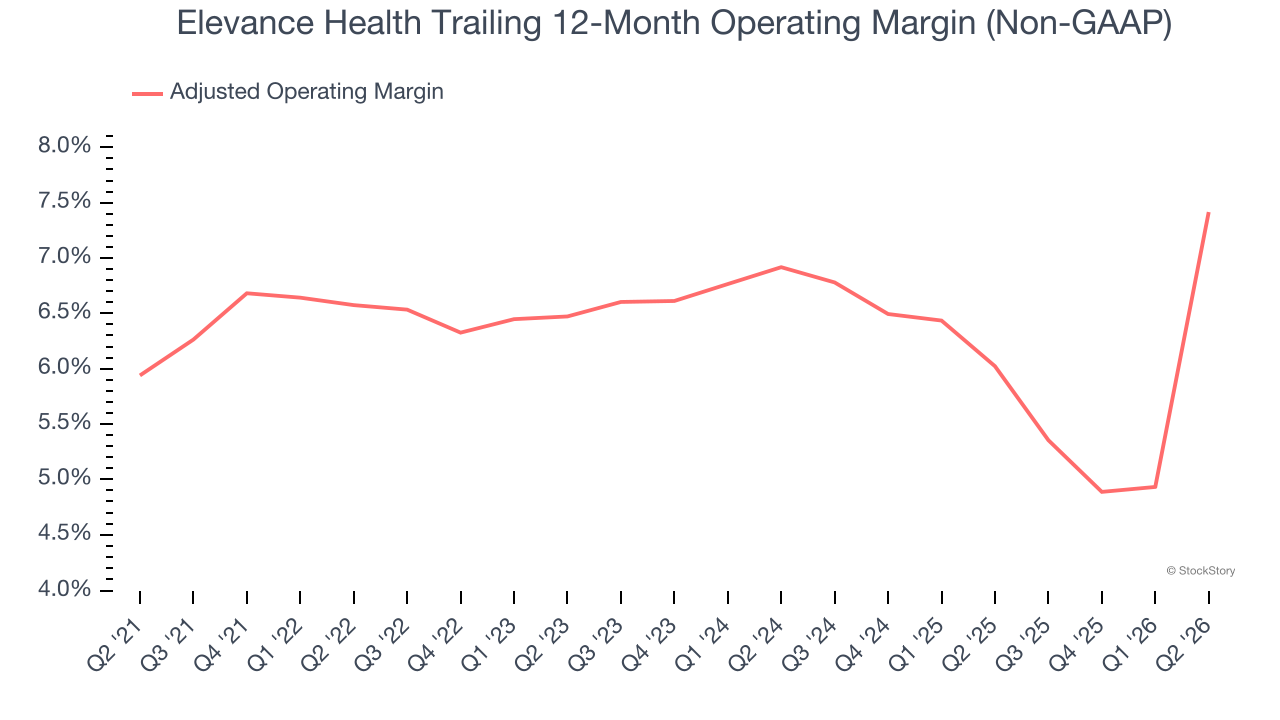

- Operating Margin: 15.7%, up from 5.3% in the same quarter last year

- Free Cash Flow Margin: 3.2%, similar to the same quarter last year

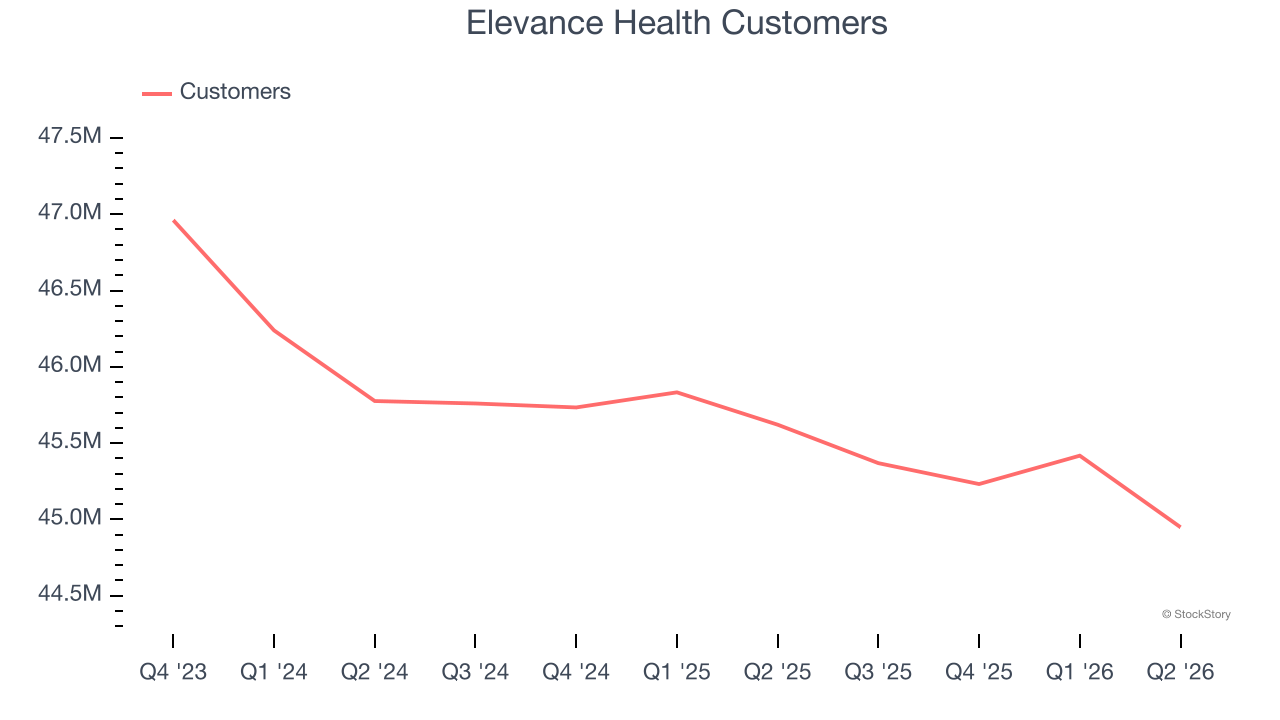

- Customers: 44.95 million, down from 45.42 million in the previous quarter

- Market Capitalization: $92.68 billion

Company Overview

Formerly known as Anthem until its 2022 rebranding, Elevance Health (NYSE: ELV) is one of America's largest health insurers, serving approximately 47 million medical members through its network-based managed care plans.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Elevance Health grew its sales at a decent 9.3% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Elevance Health’s annualized revenue growth of 8.2% over the last two years is below its five-year trend, but we still think the results were respectable.

Elevance Health also reports its number of customers, which reached 44.95 million in the latest quarter. Over the last two years, Elevance Health’s customer base averaged 1.2% year-on-year declines. Because this number is lower than its revenue growth, we can see the average customer spent more money each year on the company’s products and services.

This quarter, Elevance Health reported modest year-on-year revenue growth of 2.1% but beat Wall Street’s estimates by 3.9%.

Looking ahead, sell-side analysts expect revenue to decline by 2.3% over the next 12 months, a deceleration versus the last two years. This projection doesn’t excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses — everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Elevance Health’s adjusted operating margin has been trending up over the last 12 months and averaged 6.7% over the last five years. Although its profitability is still mediocre, we can see its decent revenue growth is giving it operating leverage as it scales. This gives it a shot at higher long-term profits if it can keep expanding.

Analyzing the trend in its profitability, Elevance Health’s adjusted operating margin might have fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Elevance Health generated an adjusted operating margin profit margin of 15.8%, up 9.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

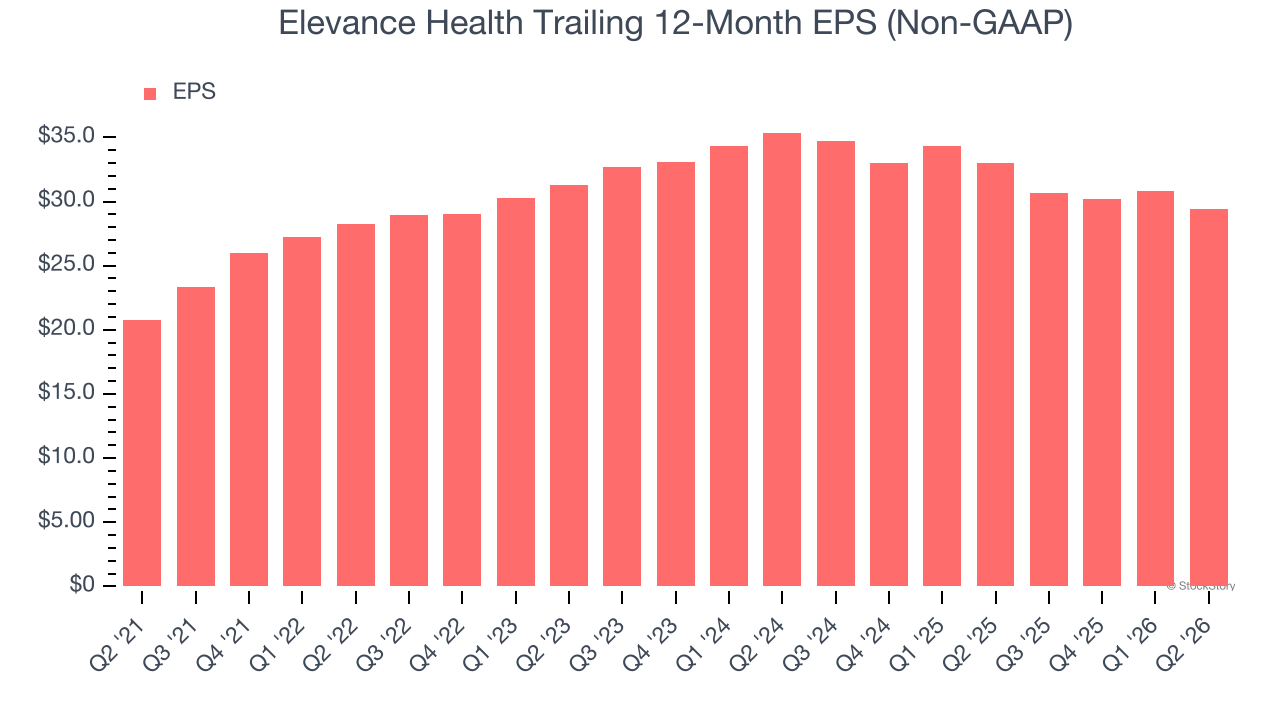

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Elevance Health’s EPS grew at a solid 7.2% compounded annual growth rate over the last five years. Despite its adjusted operating margin improvement and share repurchases during that time, this performance was lower than its 9.3% annualized revenue growth, telling us the delta came from reduced interest expenses or taxes.

In Q2, Elevance Health reported adjusted EPS of $7.45, down from $8.84 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Elevance Health’s full-year EPS to shrink by 7.9% from $29.39 to $27.06.

Key Takeaways from Elevance Health’s Q2 Results

It was good to see Elevance Health beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $428 immediately after reporting.

Sure, Elevance Health had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).