Looking back on consumer discretionary - home furnishings stocks’ Q1 earnings, we examine this quarter’s best and worst performers, including Somnigroup (NYSE: SGI) and its peers.

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare. Home furnishings companies design, manufacture, and sell furniture, décor, bedding, and related household products for residential and commercial spaces. Tailwinds include e-commerce expansion enabling broader distribution, continued remote-work trends sustaining home improvement interest, and premiumization as consumers invest in living spaces. However, headwinds are considerable: demand is closely tied to housing market activity, and rising mortgage rates have slowed home sales—a key purchase trigger. Bulky products carry high shipping costs and complex logistics. Intense competition from low-cost imports and mass-market retailers compresses margins, while consumer spending on furnishings is among the first categories deferred during economic downturns.

The 5 consumer discretionary - home furnishings stocks we track reported a slower Q1. As a group, revenues missed analysts’ consensus estimates by 2% while next quarter’s revenue guidance was 2.8% below.

While some consumer discretionary - home furnishings stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.7% since the latest earnings results.

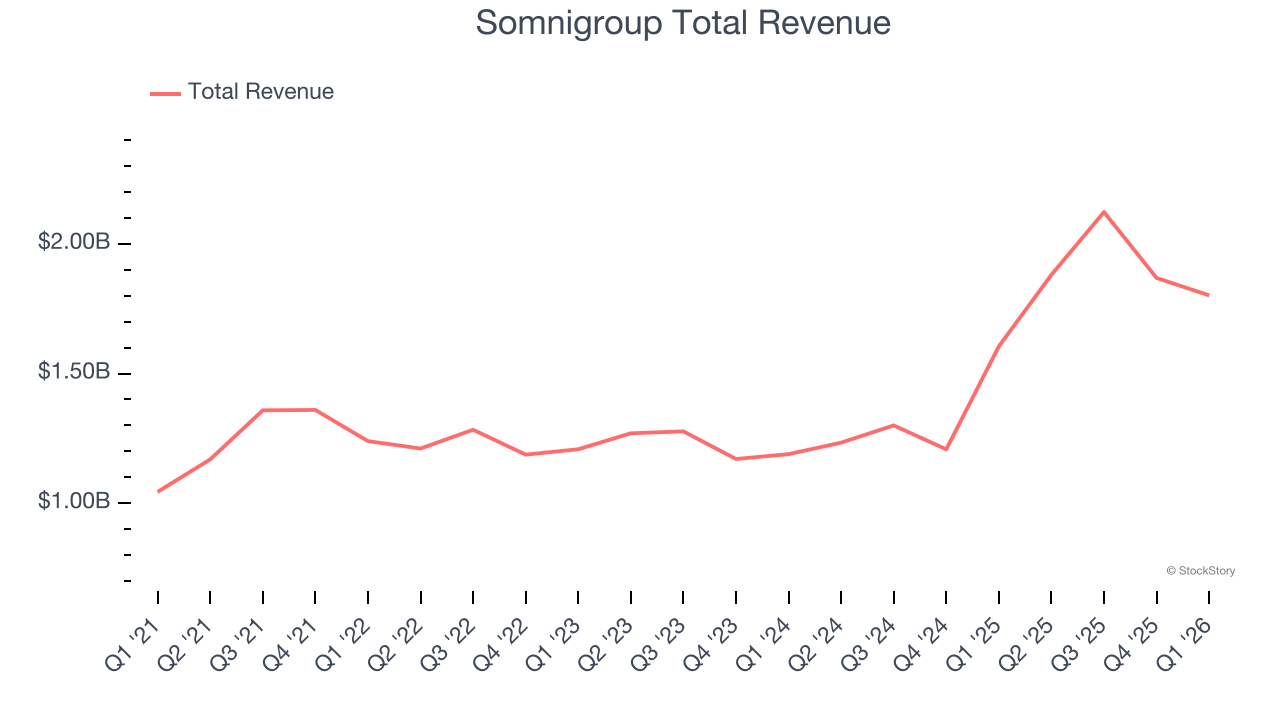

Somnigroup (NYSE: SGI)

Established through the merger of Tempur-Pedic and Sealy in 2012, Somnigroup (NYSE: SGI) is a bedding manufacturer known for its innovative memory foam mattresses and sleep products

Somnigroup reported revenues of $1.80 billion, up 12.3% year on year. This print fell short of analysts’ expectations by 1.6%. Overall, it was a slower quarter for the company with a miss of analysts’ adjusted operating income estimates and full-year EPS guidance slightly missing analysts’ expectations.

Company Chairman and CEO Scott Thompson commented, "While navigating challenging market conditions, we delivered solid financial results this quarter, including a robust 20% increase in adjusted EPS. Our performance in this muted market environment reflects the strength of our business and our continued focus on operational discipline and supporting our customers. Our scale, trusted brands, and omnichannel capabilities provide a solid foundation to succeed and support long–term value creation."

Somnigroup scored the fastest revenue growth of the whole group. The results were likely priced in, however, and the stock is flat since reporting. It currently trades at $78.43.

Read our full report on Somnigroup here, it’s free.

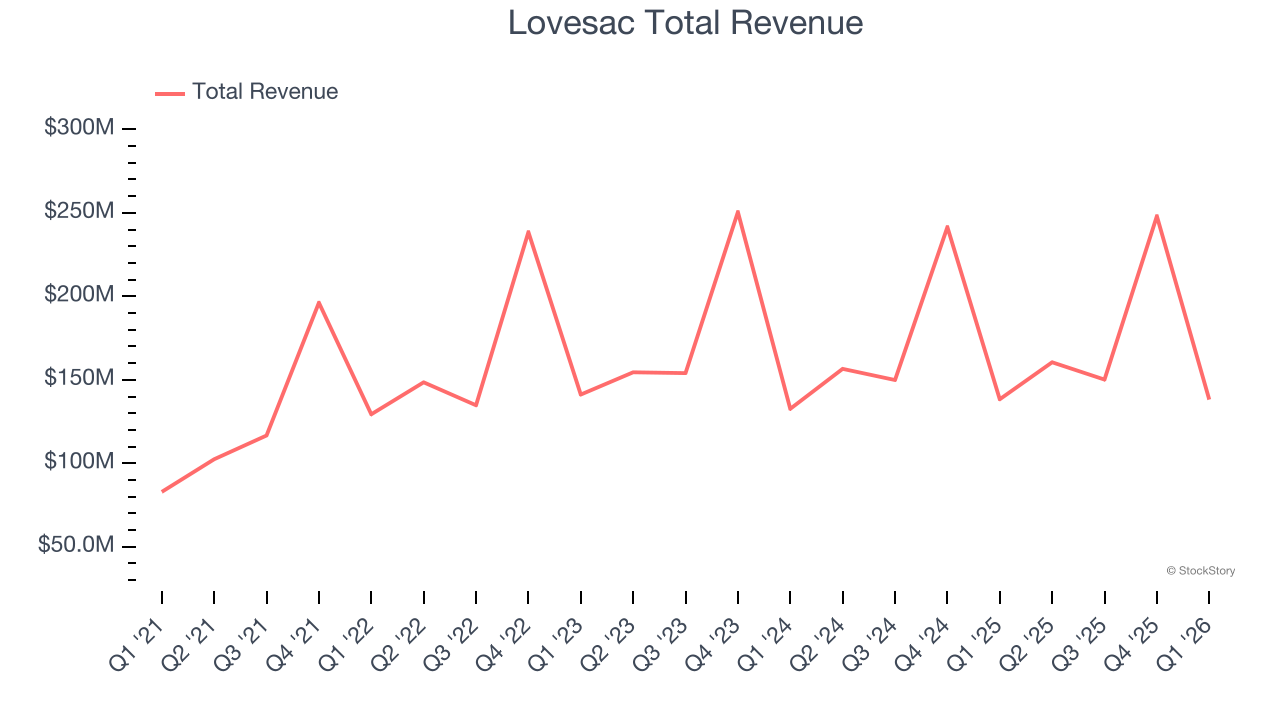

Best Q1: Lovesac (NASDAQ: LOVE)

Known for its oversized, premium beanbags, Lovesac (NASDAQ: LOVE) is a specialty furniture brand selling modular furniture.

Lovesac reported revenues of $138.2 million, flat year on year, outperforming analysts’ expectations by 1.2%. The business had a strong quarter with an impressive beat of analysts’ EBITDA estimates.

Lovesac achieved the biggest analyst estimate beat and highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 6.1% since reporting. It currently trades at $17.49.

Is now the time to buy Lovesac? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Leggett & Platt (NYSE: LEG)

Founded in 1883, Leggett & Platt (NYSE: LEG) is a diversified manufacturer of products and components for various industries.

Leggett & Platt reported revenues of $918.2 million, down 10.2% year on year, falling short of analysts’ expectations by 3.3%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income and EPS estimates.

Leggett & Platt delivered the slowest revenue growth in the group. Interestingly, the stock is up 4.7% since the results and currently trades at $11.90.

Read our full analysis of Leggett & Platt’s results here.

Mohawk Industries (NYSE: MHK)

Established in 1878, Mohawk Industries (NYSE: MHK) is a leading producer of floor-covering products for both residential and commercial applications.

Mohawk Industries reported revenues of $2.73 billion, up 8% year on year. This result came in 0.5% below analysts’ expectations. More broadly, it was a mixed quarter as it also produced a decent beat of analysts’ adjusted operating income estimates but EPS guidance for next quarter missing analysts’ expectations.

The stock is up 13.8% since reporting and currently trades at $120.10.

Read our full, actionable report on Mohawk Industries here, it’s free.

Purple (NASDAQ: PRPL)

Founded by two brothers, Purple (NASDAQ: PRPL) creates sleep and home comfort products such as mattresses, pillows, and bedding accessories.

Purple reported revenues of $95.73 million, down 8.1% year on year. This print lagged analysts’ expectations by 5.9%. Zooming out, it was a mixed quarter as it also logged a solid beat of analysts’ adjusted operating income estimates but full-year revenue guidance missing analysts’ expectations significantly.

Purple had the weakest performance against analyst estimates and weakest full-year guidance update among its peers. The stock is down 43% since reporting and currently trades at $0.37.

Read our full, actionable report on Purple here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.