What a fantastic six months it’s been for Urban Outfitters. Shares of the company have skyrocketed 40.8%, hitting $78.89. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is it too late to buy URBN? Find out in our full research report, it’s free.

Why Does URBN Stock Spark Debate?

Founded as a purveyor of vintage items, Urban Outfitters (NASDAQ: URBN) now largely sells new apparel and accessories to teens and young adults seeking on-trend fashion.

Two Positive Attributes:

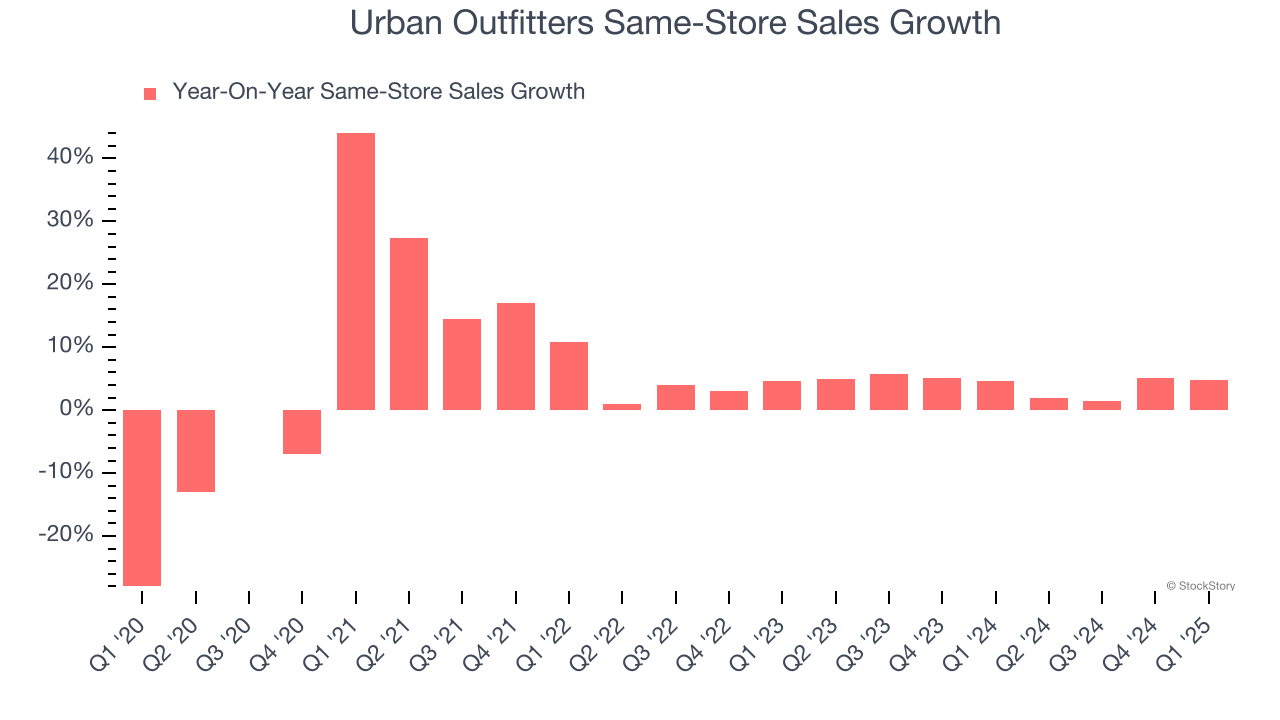

1. Surging Same-Store Sales Show Increasing Demand

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Urban Outfitters’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 4.2% per year.

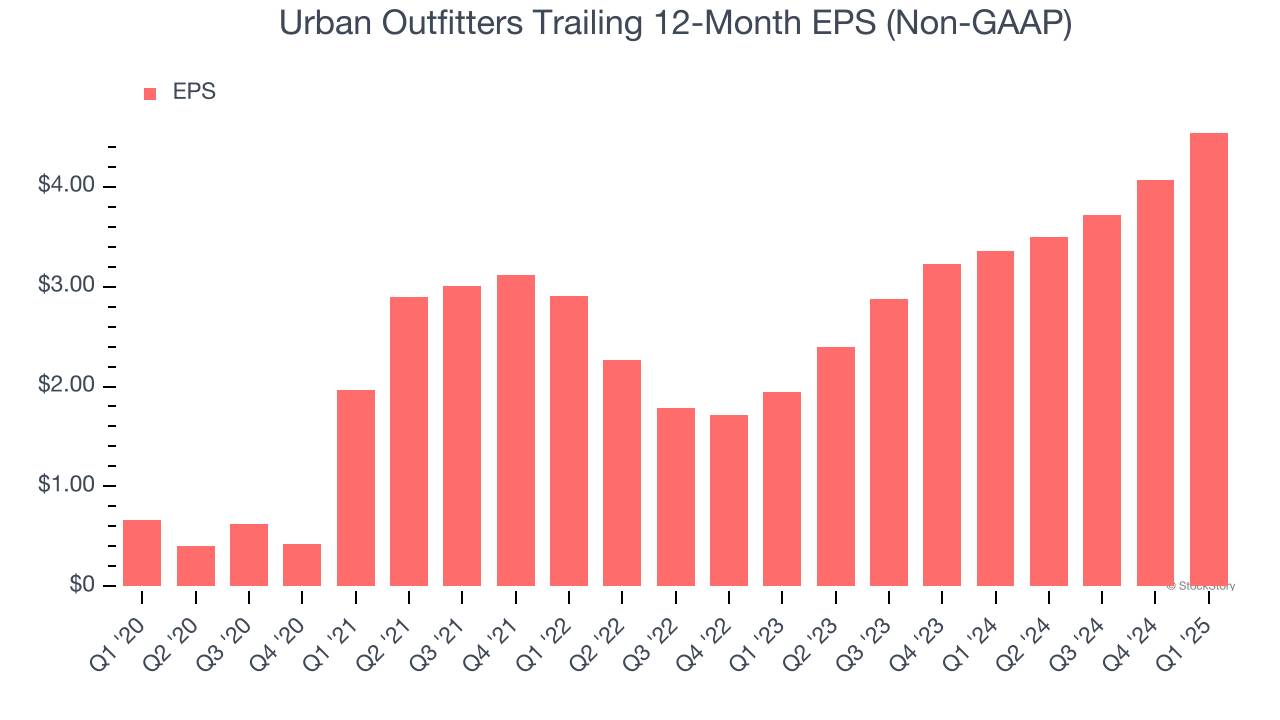

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Urban Outfitters’s full-year EPS grew at a spectacular 46.7% compounded annual growth rate over the last five years, better than the broader consumer retail sector.

One Reason to be Careful:

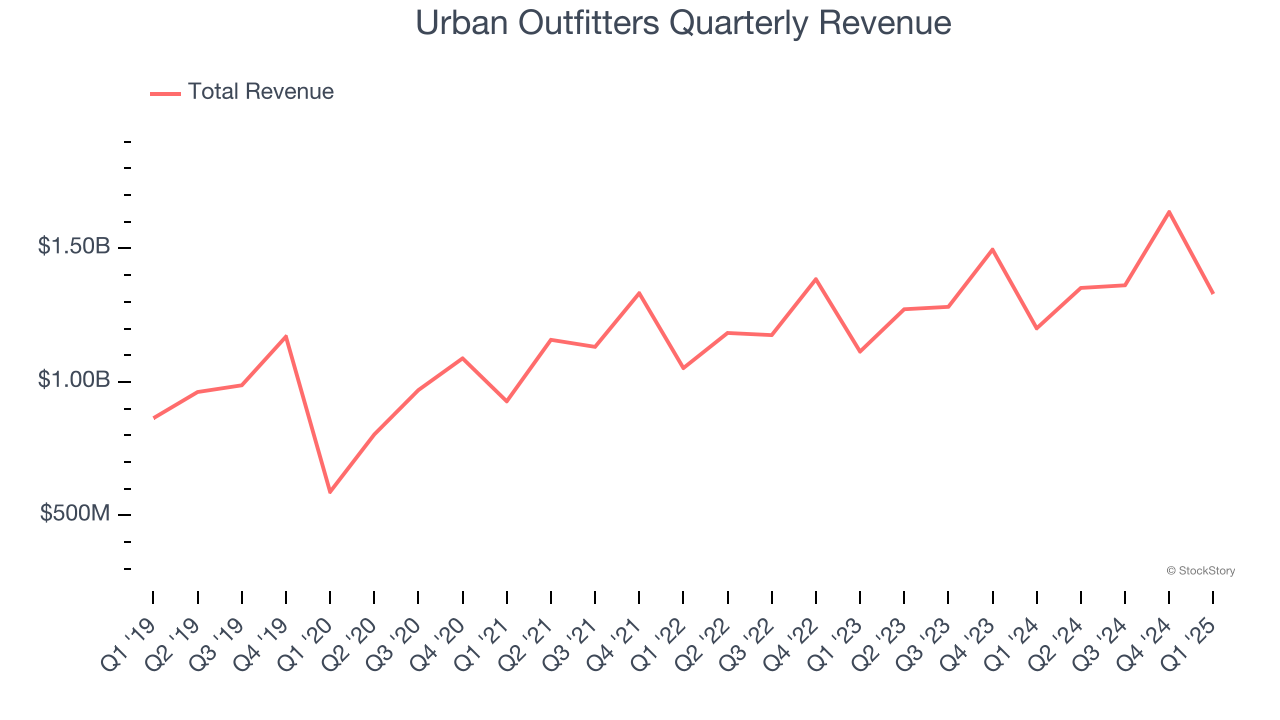

Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Urban Outfitters’s 6.2% annualized revenue growth over the last six years was tepid. This wasn’t a great result compared to the rest of the consumer retail sector, but there are still things to like about Urban Outfitters.

Final Judgment

Urban Outfitters has huge potential even though it has some open questions, and with the recent surge, the stock trades at 17.4× forward P/E (or $78.89 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Urban Outfitters

Donald Trump’s April 2024 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.