Over the past six months, Custom Truck One Source has been a great trade, beating the S&P 500 by 8.5%. Its stock price has climbed to $7.27, representing a healthy 13.9% increase. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Custom Truck One Source, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Custom Truck One Source Will Underperform?

Despite the momentum, we don't have much confidence in Custom Truck One Source. Here are three reasons you should be careful with CTOS and a stock we'd rather own.

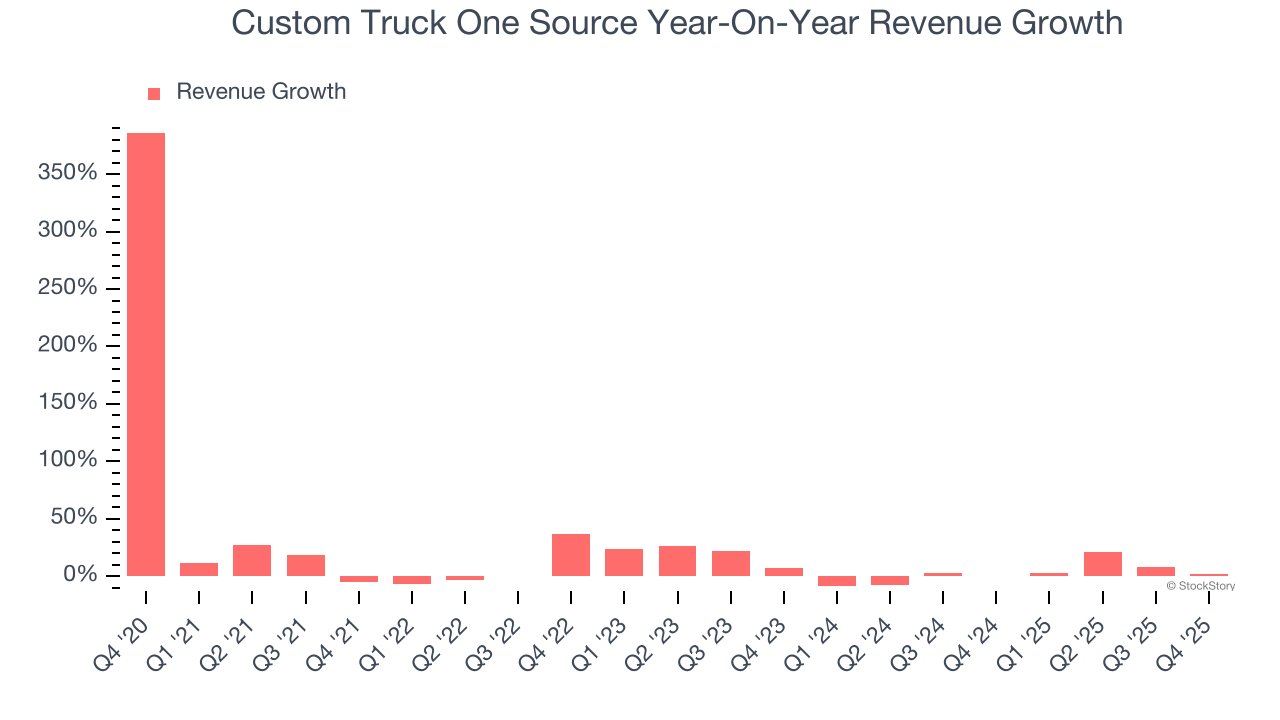

1. Lackluster Revenue Growth

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Custom Truck One Source’s recent performance shows its demand has slowed as its annualized revenue growth of 2.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

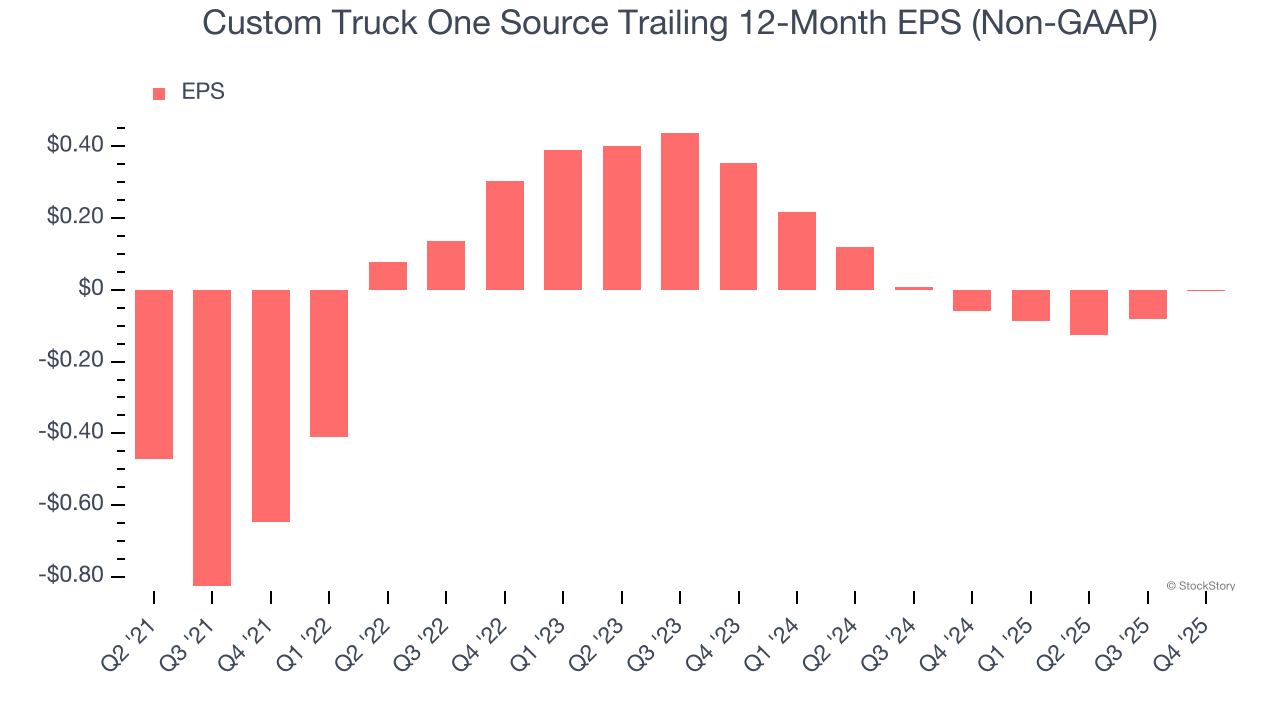

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Custom Truck One Source, its EPS declined by 6.8% annually over the last five years while its revenue grew by 7.9%. This tells us the company became less profitable on a per-share basis as it expanded.

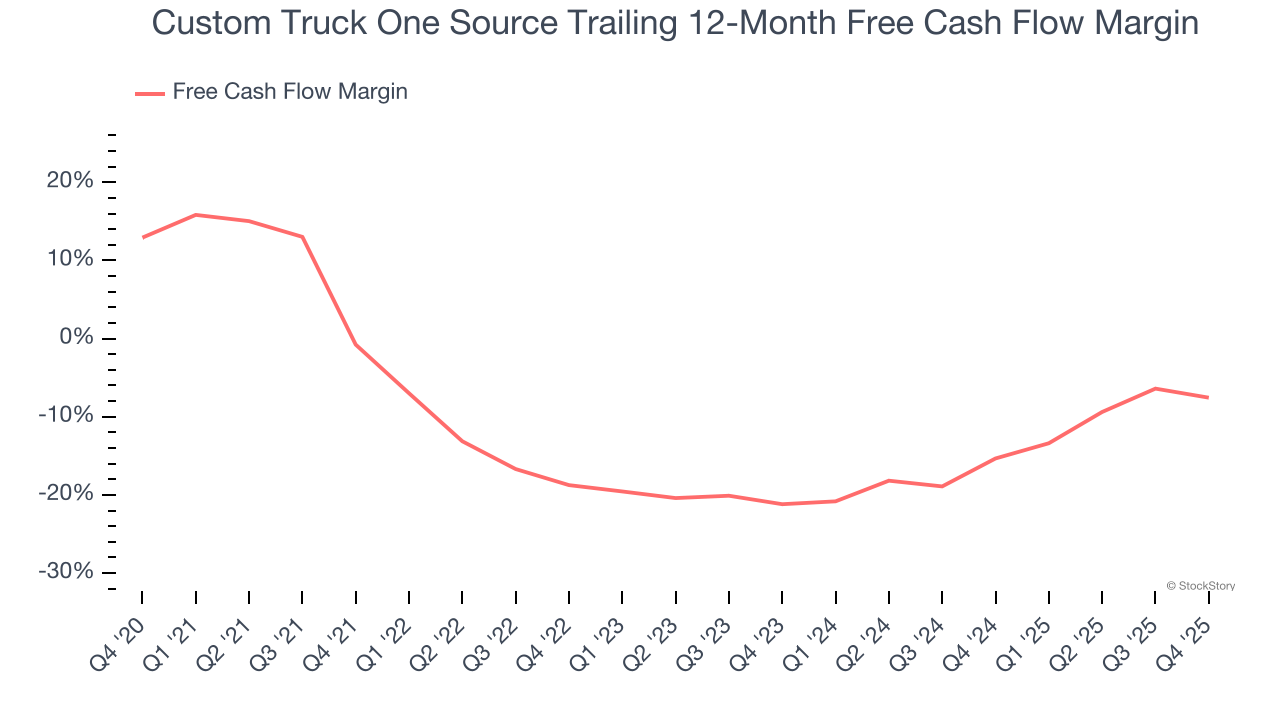

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Custom Truck One Source’s margin dropped by 6.8 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because it’s already burning cash. If the longer-term trend returns, it could signal it’s becoming a more capital-intensive business. Custom Truck One Source’s free cash flow margin for the trailing 12 months was negative 7.6%.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of Custom Truck One Source, we’ll be cheering from the sidelines. With its shares outperforming the market lately, the stock trades at 89.6× forward P/E (or $7.27 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of Custom Truck One Source

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.