AdaptHealth has had an impressive run over the past six months as its shares have beaten the S&P 500 by 31.4%. The stock now trades at $12.50, marking a 36.8% gain. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in AdaptHealth, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is AdaptHealth Not Exciting?

We’re glad investors have benefited from the price increase, but we don't have much confidence in AdaptHealth. Here are three reasons you should be careful with AHCO and a stock we'd rather own.

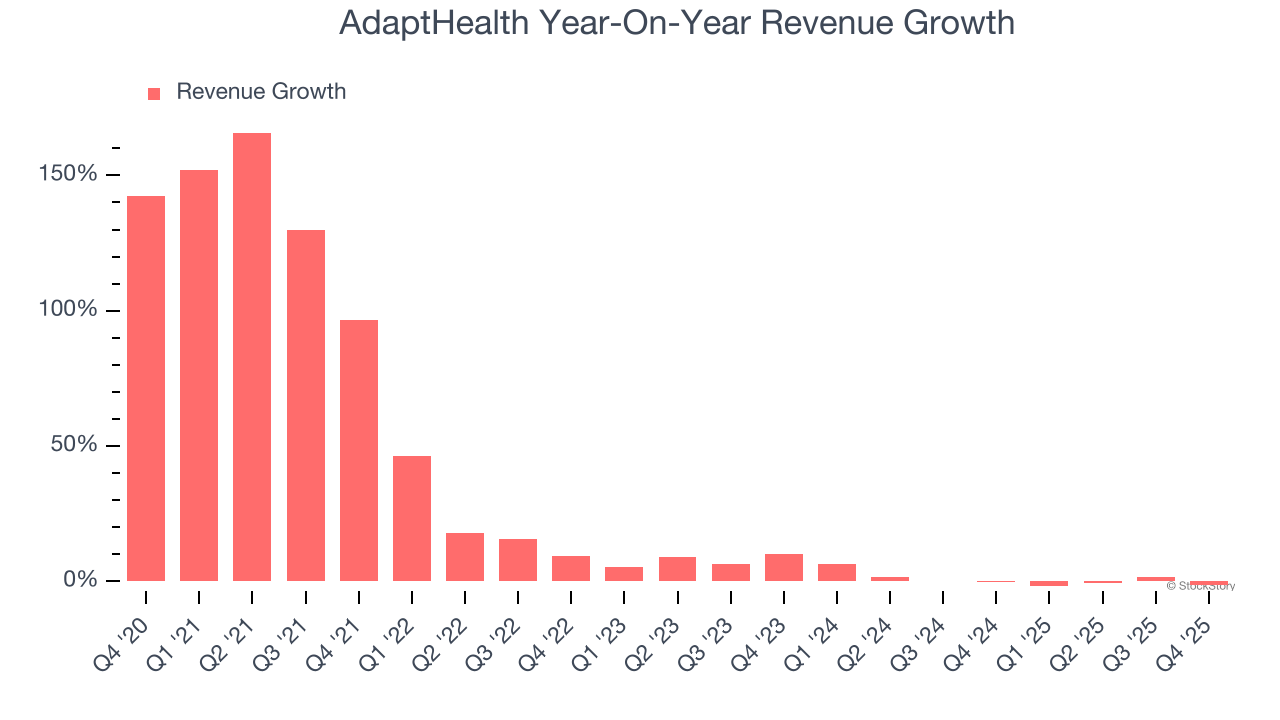

1. Revenue Growth Flatlining

Long-term growth is the most important, but within healthcare, a stretched historical view may miss new innovations or demand cycles. AdaptHealth’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

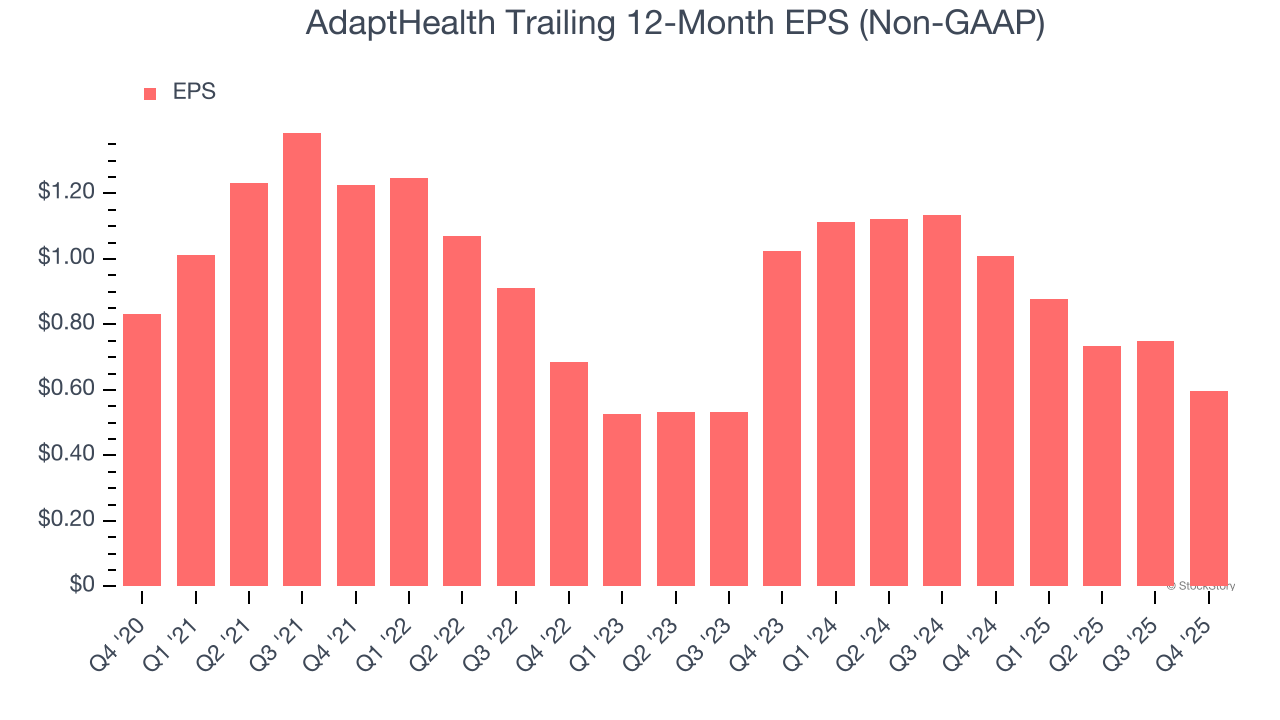

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for AdaptHealth, its EPS declined by 6.4% annually over the last five years while its revenue grew by 24.8%. This tells us the company became less profitable on a per-share basis as it expanded.

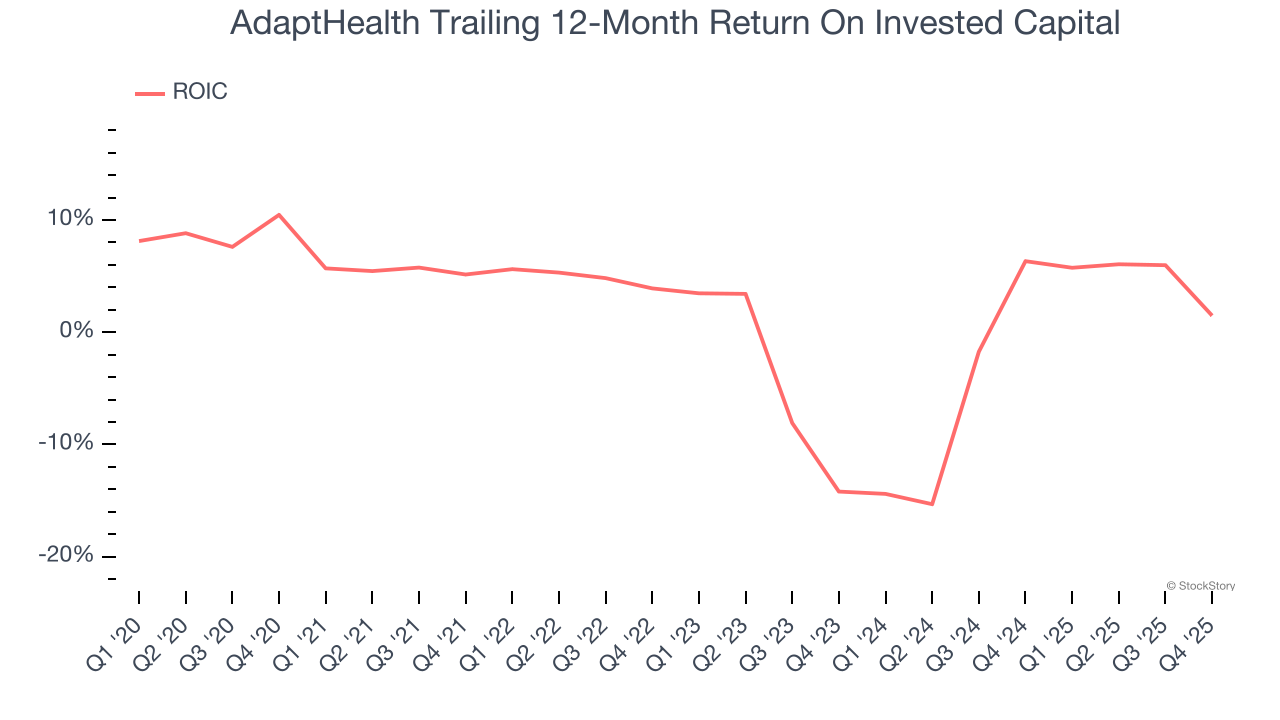

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

AdaptHealth historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 0.5%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

Final Judgment

AdaptHealth’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 12.6× forward P/E (or $12.50 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of AdaptHealth

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.