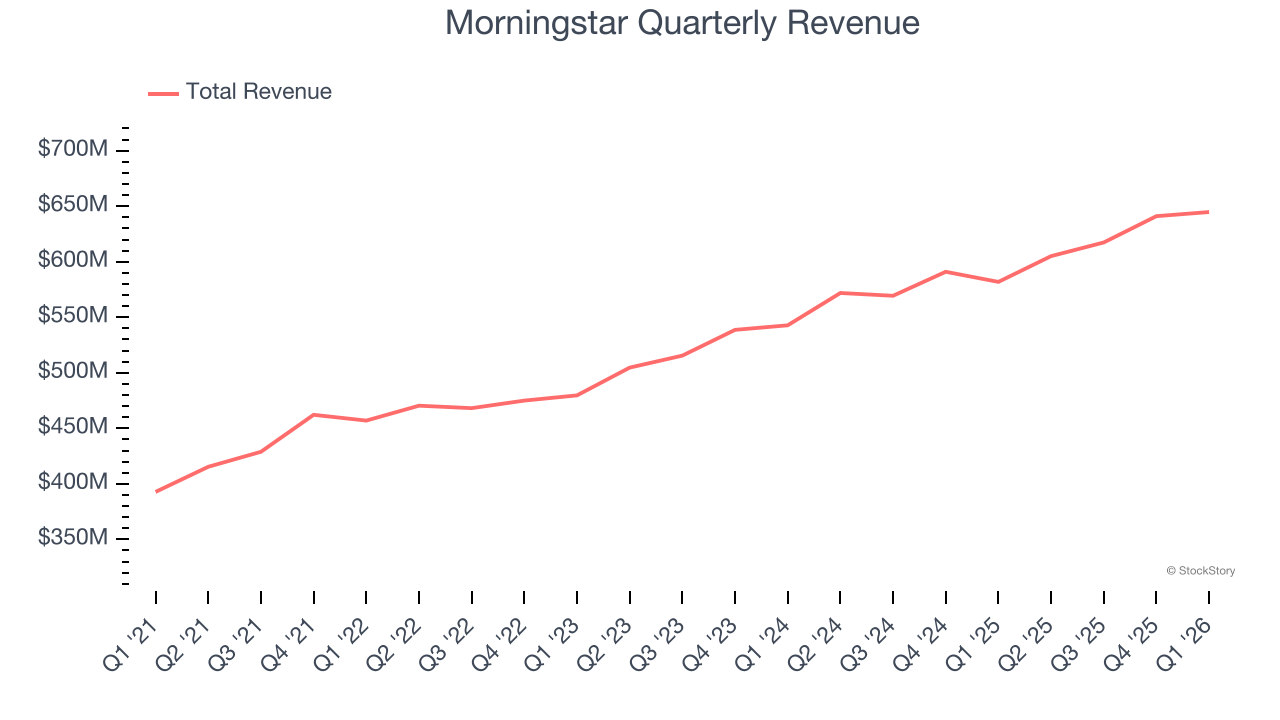

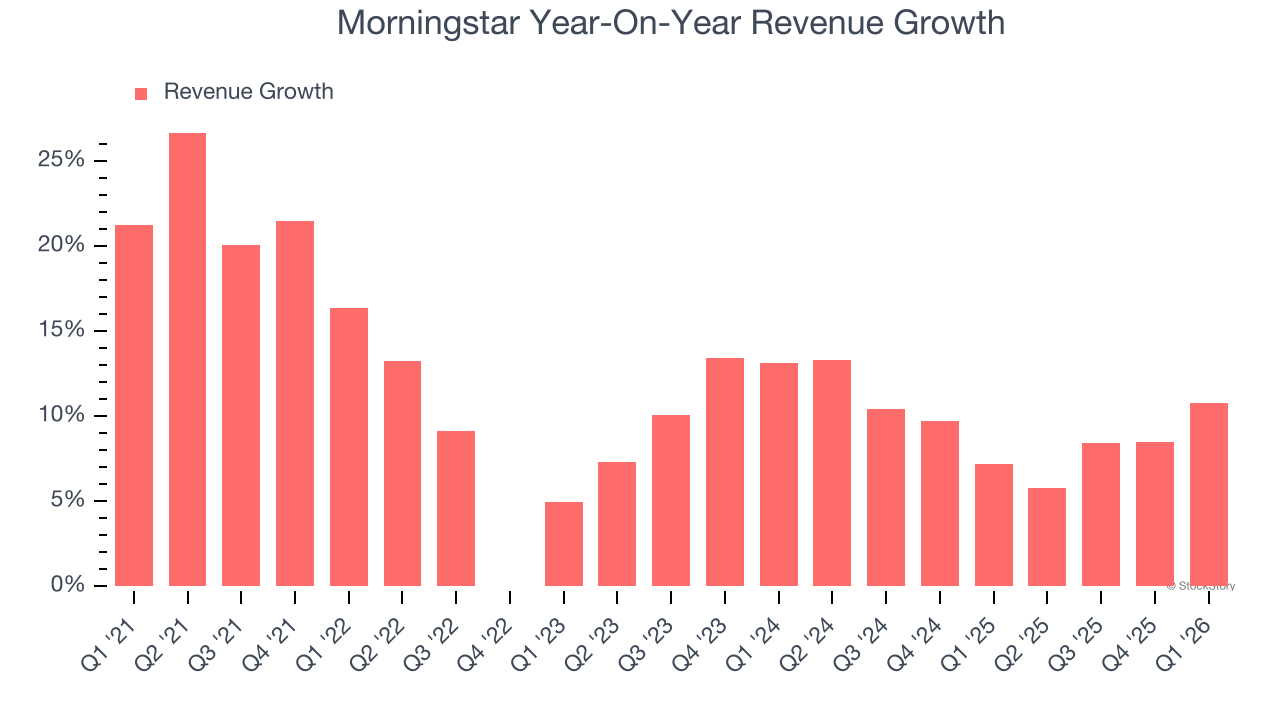

Investment research firm Morningstar (NASDAQ: MORN) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 10.8% year on year to $644.8 million. Its GAAP profit of $2.73 per share was 14.5% above analysts’ consensus estimates.

Is now the time to buy Morningstar? Find out by accessing our full research report, it’s free.

Morningstar (MORN) Q1 CY2026 Highlights:

- Revenue: $644.8 million vs analyst estimates of $626.9 million (10.8% year-on-year growth, 2.9% beat)

- Pre-tax Profit: $141.8 million (22% margin)

- EPS (GAAP): $2.73 vs analyst estimates of $2.38 (14.5% beat)

- Market Capitalization: $7.08 billion

“In the first quarter, we created significant value, growing operating and adjusted operating income by more than 30%, while reducing shares outstanding by roughly 4% for a total of more than 10% over the past 12 months,” said Kunal Kapoor, Morningstar’s CEO.

Company Overview

Founded in 1984 by Joe Mansueto with just $80,000 in personal savings, Morningstar (NASDAQ: MORN) provides independent investment data, research, and analysis tools that help investors, advisors, and institutions make informed financial decisions.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Morningstar grew its revenue at a solid 11.5% compounded annual growth rate. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Morningstar’s annualized revenue growth of 9.2% over the last two years is below its five-year trend, but we still think the results were respectable.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Morningstar reported year-on-year revenue growth of 10.8%, and its $644.8 million of revenue exceeded Wall Street’s estimates by 2.9%.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Key Takeaways from Morningstar’s Q1 Results

It was good to see Morningstar beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $185.77 immediately following the results.

So do we think Morningstar is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).