The tech-heavy Nasdaq Composite has officially entered a period of technical distress, closing decisively below its 200-day moving average (DMA) for the first time in over eighteen months. As of March 20, 2026, the index sits at approximately 21,831, a sharp decline from its February peaks, signaling a potential shift from a long-standing bull market into a defensive, high-volatility regime. This breach of the 200-day line, often considered the "line in the sand" for long-term health, has sent ripples through Silicon Valley and Wall Street alike.

The downturn is being fueled by a "perfect storm" of geopolitical instability and a cooling of the artificial intelligence (AI) hype cycle. While the primary catalysts involve a sudden spike in global energy costs and a hawkish pivot by the Federal Reserve, the technical breakdown is exacerbated by underwhelming performance and cautious guidance from the very "corporate bigwigs" that led the charge upward in 2024 and 2025. For tech investors, the signal is clear: the era of "growth at any cost" is facing its most rigorous stress test in years.

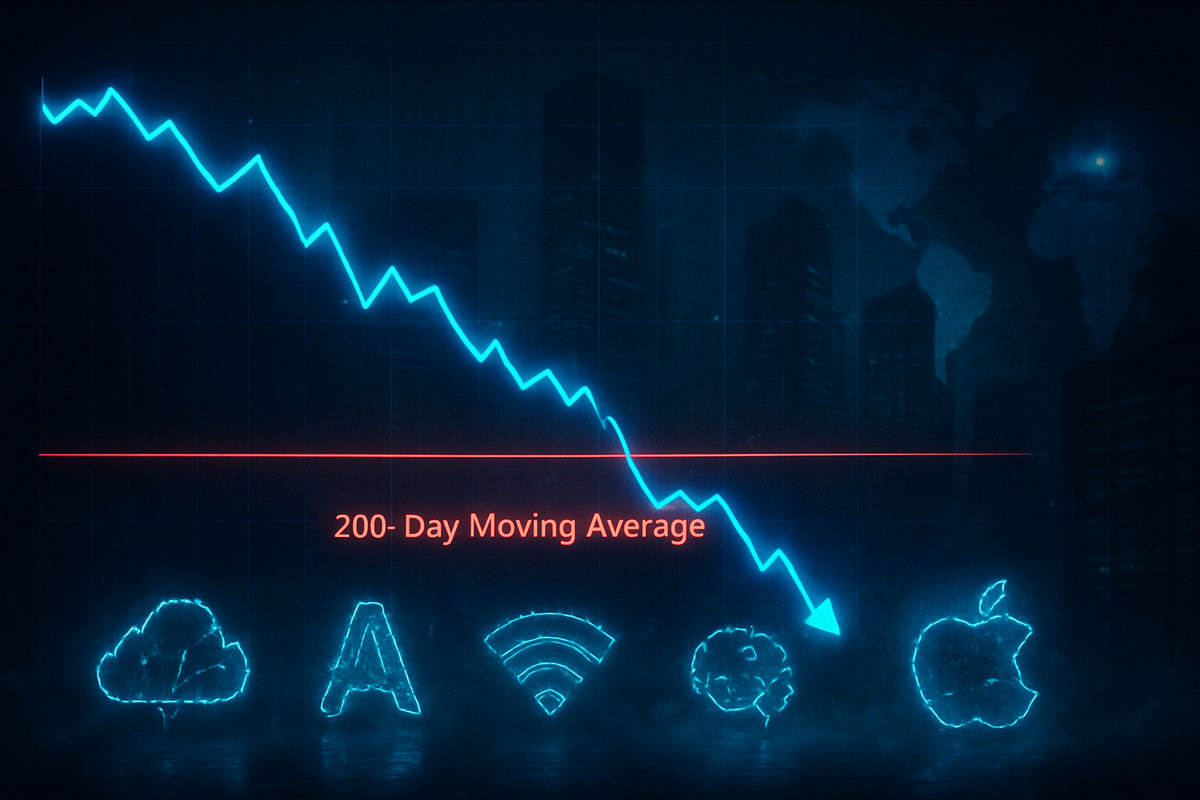

Technical Breakdown: The Fall Below 22,237

The technical deterioration of the Nasdaq Composite reached a critical inflection point during the trading sessions of March 18 and 19, 2026. After weeks of flirting with support levels, the index finally succumbed to selling pressure, slicing through its 200-day moving average of 22,237. By the closing bell on March 19, the index had settled near 21,831, representing a roughly 14% drawdown from the all-time highs recorded just a month prior. This "synchronized breakdown"—which also saw the S&P 500 and Dow Jones Industrial Average (DJIA) breach their respective long-term averages—marks a rare moment of broad market fragility.

The timeline leading to this moment was accelerated by an escalation of conflict in the Middle East, specifically involving the closure of the Strait of Hormuz. This geopolitical shock sent Brent crude oil prices skyrocketing to a range of $116–$126 per barrel, immediately raising the "tax" on data center operations and global logistics. Simultaneously, the Federal Reserve’s March meeting delivered a sobering blow: Chairman Jerome Powell signaled a "zero rate cut" path for the remainder of 2026, maintaining the federal funds rate at a restrictive 3.5%–3.75%.

Market participants had spent the early part of 2026 betting on a "soft landing," but the combination of high energy prices and sustained high interest rates has forced a revaluation of tech multiples. Technical analysts now describe the Nasdaq’s chart as a "broken MA stack," where the price currently resides below its 50-day, 100-day, and 200-day averages. This alignment typically indicates that the short-term, medium-term, and long-term trends have all turned bearish, inviting further algorithmic selling.

Initial market reactions have been characterized by a flight to safety, though even traditional "safe havens" in the tech sector are feeling the pinch. The CBOE Volatility Index (VIX) has surged, reflecting a market that is no longer willing to buy every dip. Instead, institutional investors appear to be de-risking, waiting for signs of a "washout" bottom or a stabilization in the geopolitical landscape before re-entering the fray.

Corporate Bigwigs Under the Microscope

The "weak performance" cited by analysts refers less to a lack of revenue and more to a lack of vision for sustainable margins in a high-cost environment. Adobe Inc. (NASDAQ: ADBE) became a focal point for investor anxiety this month after reporting record Q1 2026 revenue of $6.4 billion. Despite the 12% year-over-year growth, the stock plummeted as the company grappled with the departure of long-time CEO Shantanu Narayen and offered tepid guidance regarding the pace of its AI monetization. Investors are increasingly skeptical of "AI-first" narratives that do not immediately translate into improved bottom-line efficiencies.

Similarly, Micron Technology, Inc. (NASDAQ: MU) highlighted the paradox of the current market. The chipmaker reported a staggering 196% surge in revenue to $23.86 billion, driven by insatiable demand for high-bandwidth memory. However, the stock was sold off following the report, as investors focused on the ballooning capital expenditure (CapEx) requirements. The market is beginning to punish companies that must spend record amounts of cash just to maintain their competitive position in the AI arms race.

The "Hyperscalers"—including Microsoft Corp. (NASDAQ: MSFT), Alphabet Inc. (NASDAQ: GOOGL), and Amazon.com, Inc. (NASDAQ: AMZN)—are also facing a "show me the money" moment. These giants have collectively committed over $200 billion to AI infrastructure for 2026. With energy costs for massive GPU clusters doubling due to the oil shock, the return on investment (ROI) for these projects is being pushed further into the future. Meta Platforms, Inc. (NASDAQ: META), while still profitable, has seen its valuation multiple compressed as the market questions how long it can sustain its massive spending on the "Metaverse-AI" hybrid model in a 4% interest rate environment.

One surprising loser in this technical breakdown has been the private credit sector, which has become deeply intertwined with Nasdaq-listed firms. Blue Owl Capital Inc. (NYSE: OWL) and other alternative asset managers have faced selling pressure as private credit funds triggered "redemption gates." This liquidity squeeze in the private markets has forced some institutional holders to sell their liquid Nasdaq holdings to meet cash demands elsewhere, creating a secondary wave of selling pressure on tech stocks.

Broader Significance: The End of AI Exceptionalism?

The breach of the 200-day moving average is more than just a chart pattern; it represents a psychological shift in how the market views the tech sector’s "exceptionalism." For much of 2023 through 2025, tech stocks were treated as a hedge against inflation and economic stagnation. However, the current energy-driven "stagflation" threat has exposed the vulnerability of the sector. High-growth tech stocks are "long-duration assets," meaning their valuations are highly sensitive to the discount rates used in financial models. With the Fed refusing to budge on rates, those valuations are being systematically downsized.

Historically, this event draws comparisons to the "post-hype" corrections seen in 2001 and 2022. Much like the transition from the internet build-out to the era of internet profitability, 2026 appears to be the year where the "AI Build-out" must transition to "AI Efficiency." The ripple effects are already being felt by partners and competitors; smaller AI startups that rely on the Hyperscalers for credits or venture funding are seeing their runways shorten as their corporate patrons tighten their belts.

On the regulatory front, the downturn may provide a temporary reprieve from antitrust scrutiny, as policymakers focus more on economic stability than on breaking up big tech. However, the long-term trend remains one of increased oversight. The European Union’s latest AI implementation acts are adding compliance costs just as margins are being squeezed by energy prices. This "double squeeze"—regulatory costs plus operational costs—is forcing a consolidation within the industry that could favor only the most well-capitalized players.

Ultimately, this event signals a transition in the industry trend from "expansion at all costs" to "resilience and energy efficiency." Companies that can demonstrate a path to AI profitability without a total reliance on cheap energy or cheap capital are likely to emerge as the next generation of leaders, while those stuck in the "spending for the sake of growth" cycle may see their stock prices remain below their 200-day averages for an extended period.

The Road Ahead: Potential Scenarios and Strategic Pivots

In the short term, the Nasdaq Composite is looking for a "floor," with many technical analysts eyeing the 21,500 level as the next major area of support. If this level fails to hold, the index could officially enter a bear market, defined as a 20% drop from the highs. Investors should expect continued volatility as the market digests upcoming earnings reports from the remaining semiconductor players and cloud providers. A strategic pivot toward "Energy-Efficient AI" and "Edge Computing" is likely to become the new mantra for 2027, as companies seek to reduce their reliance on massive, energy-hungry data centers.

A potential "upside" scenario involves a de-escalation of the Strait of Hormuz conflict, which would lead to a rapid cooling of oil prices. Such a move would provide the Federal Reserve with the "inflationary cover" needed to finally cut rates, potentially sparking a "relief rally" that could carry the Nasdaq back above its moving averages. However, most strategists are currently advising a cautious "wait-and-see" approach, noting that technical damage of this magnitude often takes months, not weeks, to repair.

For investors, the challenge will be distinguishing between companies that are temporarily hindered by macro factors and those whose fundamental business models are broken by the higher-for-longer interest rate environment. The market is likely to remain bifurcated; "value-tech" companies with strong cash flows and low debt will likely outperform the "moonshot" AI companies that have yet to turn a profit.

Closing Thoughts: A Market in Transition

The Nasdaq Composite's slide below its 200-day moving average on March 20, 2026, marks a somber milestone in the post-pandemic tech cycle. It serves as a stark reminder that even the most transformative technologies, like generative AI, are not immune to the gravity of macroeconomic forces and geopolitical reality. The "weak performance" of corporate leaders like Adobe and the margin pressures on Micron and the Hyperscalers suggest that the market is now demanding a higher standard of fiscal discipline.

Moving forward, the health of the tech sector will depend on its ability to adapt to a world where energy is expensive and capital is no longer free. The "AI-fever" of the past three years is giving way to a more mature, albeit more painful, phase of corporate evolution. This transition, while difficult for portfolios in the near term, is often a necessary precursor to the next sustainable leg of growth.

Investors should closely watch the $110/barrel oil level and the Fed’s commentary in the coming months. A sustained break below 21,500 on the Nasdaq could signal a deeper structural bear market, while a recovery above the 200-day average would require a significant improvement in both corporate guidance and global stability. For now, caution remains the order of the day as the tech world recalibrates its expectations for the late 2020s.

This content is intended for informational purposes only and is not financial advice.