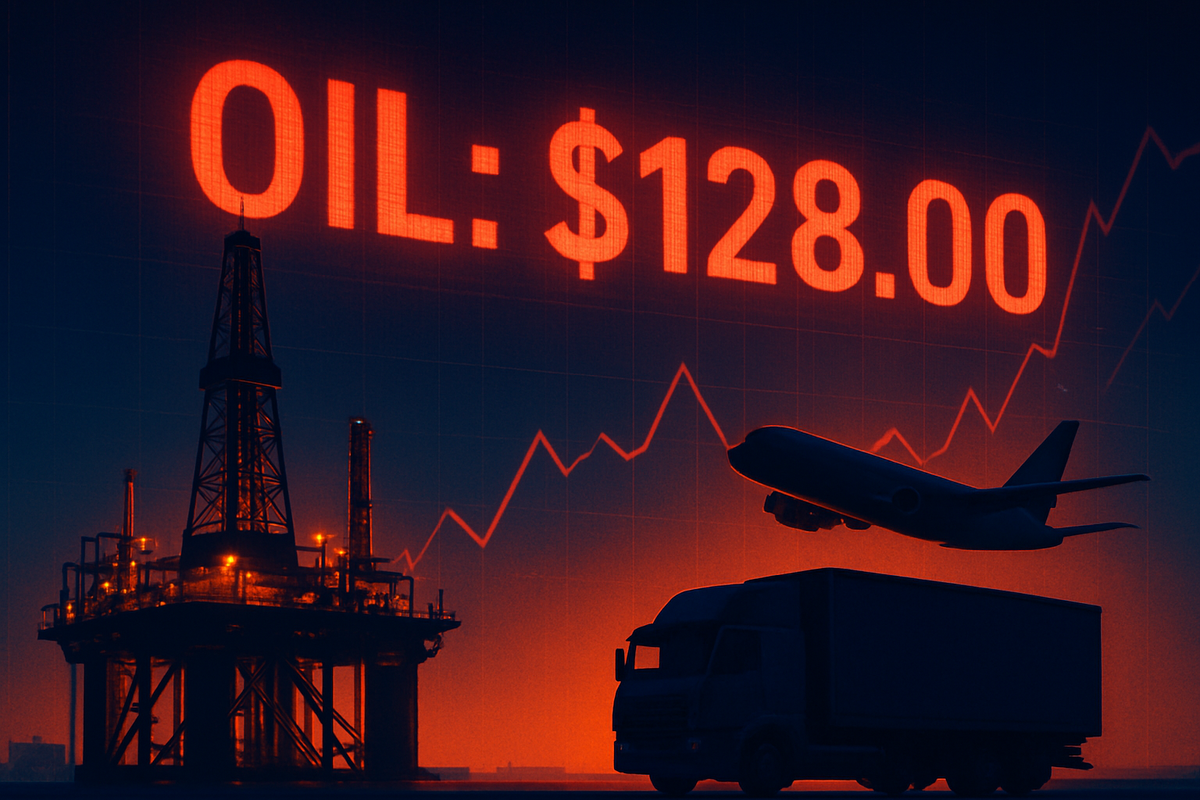

As of April 13, 2026, the global economy is grappling with a relentless energy shock that has sent Brent crude oil soaring to $128 per barrel, its highest level in years. This sustained surge, fueled by a perfect storm of geopolitical conflict and production bottlenecks, is fundamentally redrawing the map for equity investors. While the energy sector is entering a new "golden age" of profitability, the ripple effects are being felt across every corner of the market, reigniting fears of stagflation and forcing a dramatic reassessment of inflation expectations.

The immediate implications are stark: headline inflation in the United States is currently tracking toward 4.0%, effectively silencing any talk of interest rate cuts from the Federal Reserve until at least mid-2027. For the average consumer, the "energy tax" is manifesting at the pump and in grocery aisles, leading to a visible softening in discretionary spending. However, the market's reaction has not been uniform; a distinct bifurcation has emerged, with "safe-haven" defensive sectors like utilities outperforming, while high-cost sectors like consumer staples and transportation struggle to keep their heads above water.

The Perfect Storm: Geopolitical Gridlock and Supply Squeezes

The road to $100 oil began in late 2025, following a series of escalations in the Middle East that culminated in the effective closure of the Strait of Hormuz. By early April 2026, military actions involving the U.S., Israel, and Iran had obstructed roughly 20% of the world’s seaborne oil supply. This geopolitical bottleneck has resulted in a staggering global inventory draw of approximately 5.1 million barrels per day. The sudden disappearance of 9.1 million barrels per day of export capacity from heavyweights like Saudi Arabia and Kuwait has left the market in a state of chronic deficit.

While the United States has reached a record production level of 13.51 million barrels per day, domestic output has proven insufficient to fill the void. The situation was further exacerbated by a strategic decision by OPEC+ to pause planned production increases during the first quarter of 2026, citing seasonal demand uncertainty. Though the cartel began a gradual unwinding of voluntary cuts this month, the market remains skeptical that the additional supply will arrive quickly enough to cool the $115-per-barrel average projected for the second quarter.

The initial market reaction has been one of flight-to-safety, though with a modern twist. Investors are no longer simply buying "the market"; they are aggressively rotating into companies with "zero fuel risk" or those with the pricing power to pass through astronomical energy costs. The result is a volatile trading environment where energy-sensitive indices are seeing daily swings of 2% to 3% as the world awaits any sign of a diplomatic breakthrough in the Gulf.

Winners and Losers: A Tale of Two Tickers

The primary beneficiaries of this crisis are the integrated oil giants. ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) have seen their stock prices surge by nearly 28% year-to-date. ExxonMobil, in particular, has leveraged its 2024 acquisition of Pioneer Natural Resources and its booming operations in Guyana to generate record free cash flow. In a significant strategic pivot announced late last year, XOM reallocated $10 billion from its low-carbon initiatives back into high-margin Permian Basin drilling, a move that now looks prescient as it captures the $120+ spot prices.

In the defensive space, a clear winner has emerged in NextEra Energy (NYSE: NEE). The utility giant has gained over 46% in the last six months, driven by its dual identity as a safe-haven asset and a key beneficiary of the "AI power boom." Because of its massive portfolio of renewable assets, NextEra is shielded from the rising natural gas and oil prices that are currently squeezing its peers. Its 30 GW project backlog for data center power has made it a favorite for investors looking to hide from inflation while maintaining exposure to structural growth.

Conversely, the losers are found in the transportation and consumer staples sectors. Delta Air Lines (NYSE: DAL) is facing a projected $2 billion increase in fuel costs for the current quarter, forcing the airline to cut capacity and raise baggage fees to unprecedented levels. Similarly, consumer staples titan Procter & Gamble (NYSE: PG) has seen its shares slide 14% over the past year. Despite its brand strength, P&G is facing significant margin compression as the cost of plastic packaging and logistics—both heavily tied to oil prices—erodes its bottom line. Investors are increasingly worried that "price fatigue" among consumers will prevent the company from implementing further hikes to offset these costs.

Inflationary Repercussions and the Death of the Pivot

The broader significance of this oil spike cannot be overstated. It has effectively reset the "higher-for-longer" interest rate narrative. With the Consumer Price Index (CPI) stubbornly stuck near 4%, the Federal Reserve’s previous roadmap for 2026 has been discarded. The "energy tax" is acting as a natural brake on economic growth, but because it is supply-driven rather than demand-driven, the Fed is trapped in a policy corner—unable to cut rates to support growth for fear of further embedding inflation expectations.

This event also signals a major shift in corporate energy policy. For the past five years, the trend was toward aggressive "green" transitions. However, the reality of 2026 has forced a "Great Re-calibration." Companies like United Parcel Service (NYSE: UPS) are accelerating their move into Renewable Natural Gas (RNG) and hybrid-electric fleets, not just for sustainability, but as a survival mechanism against petroleum volatility. UPS’s implementation of dynamic weekly fuel surcharges, which reached 22.75% this month, reflects a new era where logistics costs are treated as a volatile commodity rather than a fixed expense.

Historically, this period draws comparisons to the 1970s oil shocks, yet the integration of technology and the dominance of the U.S. as a producer create a more complex dynamic. The "ripple effects" are now global and digital; the high cost of energy is even impacting the expansion of the digital economy, as the massive energy requirements for AI training become significantly more expensive for firms that do not have long-term power purchase agreements in place.

The Road Ahead: Potential Scenarios

In the short term, the market will remain hyper-fixated on the Strait of Hormuz and any signals from the OPEC+ monitoring committee. A de-escalation in Middle Eastern tensions could see $20 to $30 of "geopolitical premium" evaporate from oil prices almost overnight, potentially sparking a massive relief rally in consumer-facing stocks. However, if the blockade persists through the summer travel season, Brent could realistically test $140, a level that most analysts believe would trigger significant "demand destruction."

Longer-term, this crisis is likely to accelerate the structural shift toward energy independence and alternative fuels. We are already seeing a strategic pivot from companies that previously relied on "just-in-time" logistics to "just-in-case" inventory management, further increasing the demand for warehousing and localized manufacturing. The winners of the next 24 months will be those who successfully "de-link" their operations from the global crude market.

The ultimate outcome depends on whether the global economy can absorb these prices without falling into a deep recession. A "soft landing" now depends entirely on the resilience of the U.S. consumer and the ability of the energy sector to maintain supply levels. Market participants should prepare for a period of "rolling volatility" where sector selection becomes far more important than broad market exposure.

Summary and Investor Takeaways

The sustained triple-digit oil prices of April 2026 have proven to be a watershed moment for the markets. The primary takeaway for investors is that inflation is no longer a "transitory" ghost of the pandemic era but a persistent feature of the current geopolitical landscape. The traditional defensive playbook has been rewritten: while utilities like NextEra Energy (NYSE: NEE) offer a refuge, consumer staples like Procter & Gamble (NYSE: PG) are no longer the safe bets they once were in an era of high-input inflation.

Moving forward, the market is likely to remain in a defensive crouch. Investors should keep a close watch on two key indicators: the monthly CPI reports and the weekly U.S. oil inventory data. Any sustained break below $100 for WTI would be a signal that the worst of the inflationary pressure is easing, but until then, the "Energy First" strategy remains the dominant trade on Wall Street. The lasting impact of this period will be a permanent shift in how companies and investors value energy security, moving it from a peripheral concern to the very center of strategic planning.

This content is intended for informational purposes only and is not financial advice.