Over the past six months, Commerce Bancshares’s stock price fell to $53.68. Shareholders have lost 9.1% of their capital, which is disappointing considering the S&P 500 has climbed by 7.6%. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Commerce Bancshares, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Commerce Bancshares Not Exciting?

Even with the cheaper entry price, we're cautious about Commerce Bancshares. Here are three reasons we avoid CBSH and a stock we'd rather own.

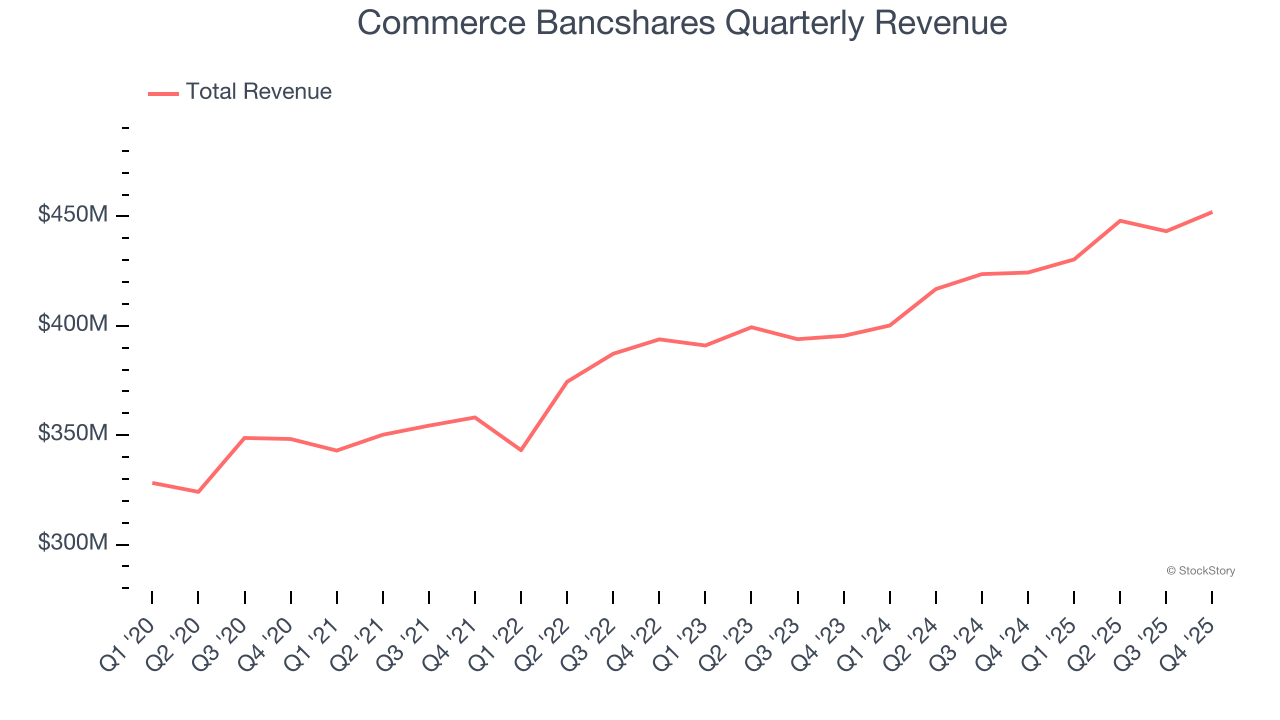

1. Long-Term Revenue Growth Disappoints

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income.

Unfortunately, Commerce Bancshares’s 5.6% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the banking sector.

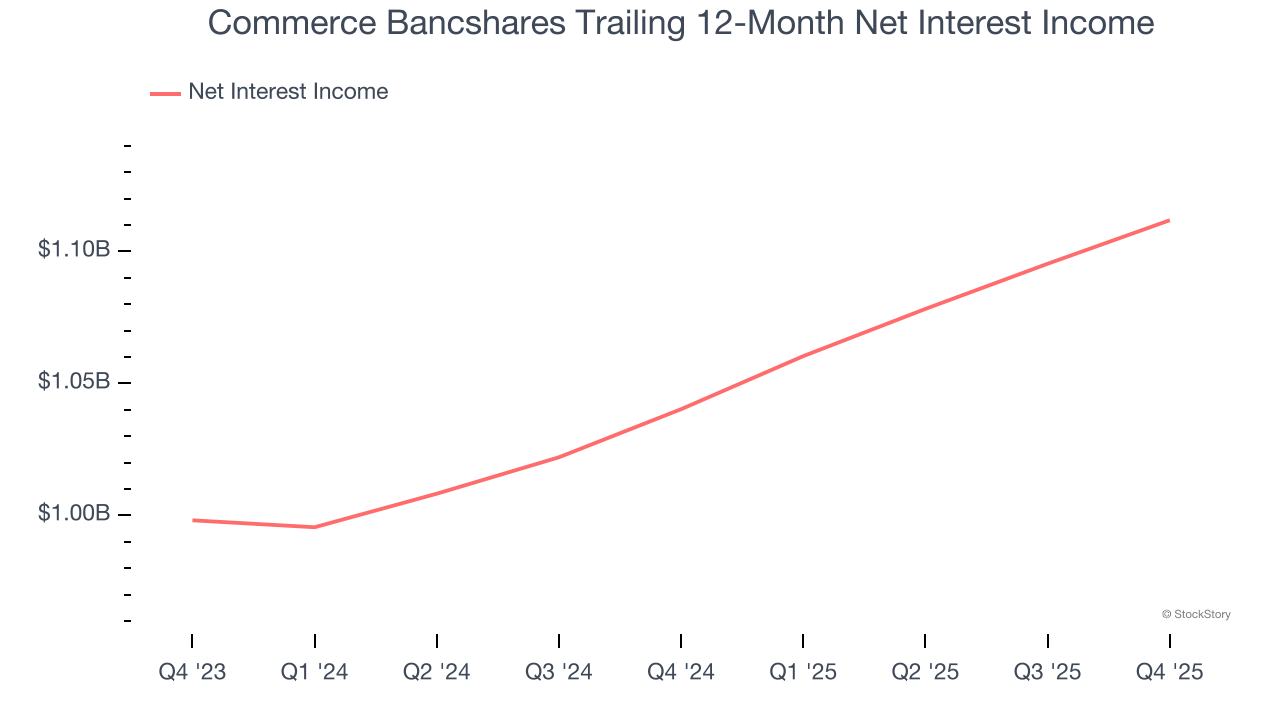

2. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Commerce Bancshares’s net interest income has grown at a 6% annualized rate over the last five years, worse than the broader banking industry and in line with its total revenue.

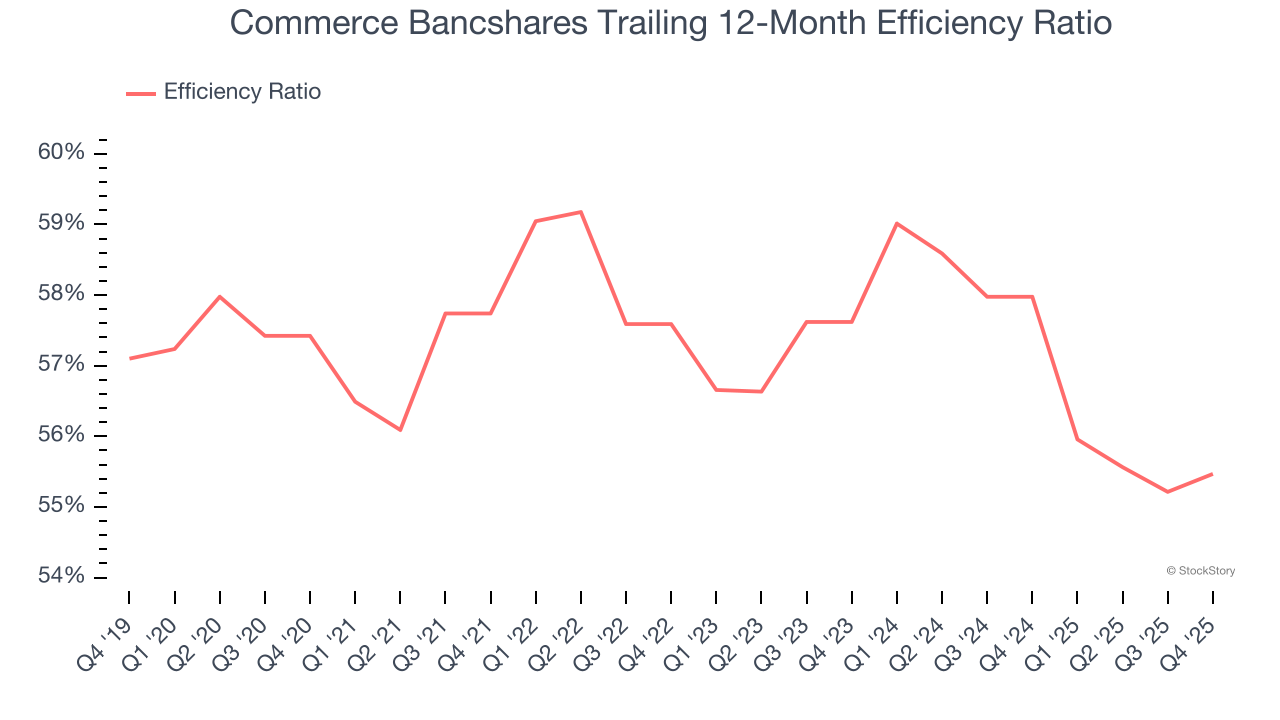

3. Efficiency Ratio Expected to Falter

Topline growth alone doesn't tell the complete story - the profitability of that growth shapes actual earnings impact. Banks track this dynamic through efficiency ratios, which compare non-interest expenses such as personnel, rent, IT, and marketing costs to total revenue streams.

Markets understand that a bank’s expense base depends on its revenue mix and what mostly drives share price performance is the change in this ratio, rather than its absolute value. It’s somewhat counterintuitive, but a lower efficiency ratio is better.

For the next 12 months, Wall Street expects Commerce Bancshares to become less profitable as it anticipates an efficiency ratio of 56.9% compared to 55.5% over the past year.

Final Judgment

Commerce Bancshares’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 1.7× forward P/B (or $53.68 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. Let us point you toward one of our top digital advertising picks.

Stocks We Like More Than Commerce Bancshares

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.