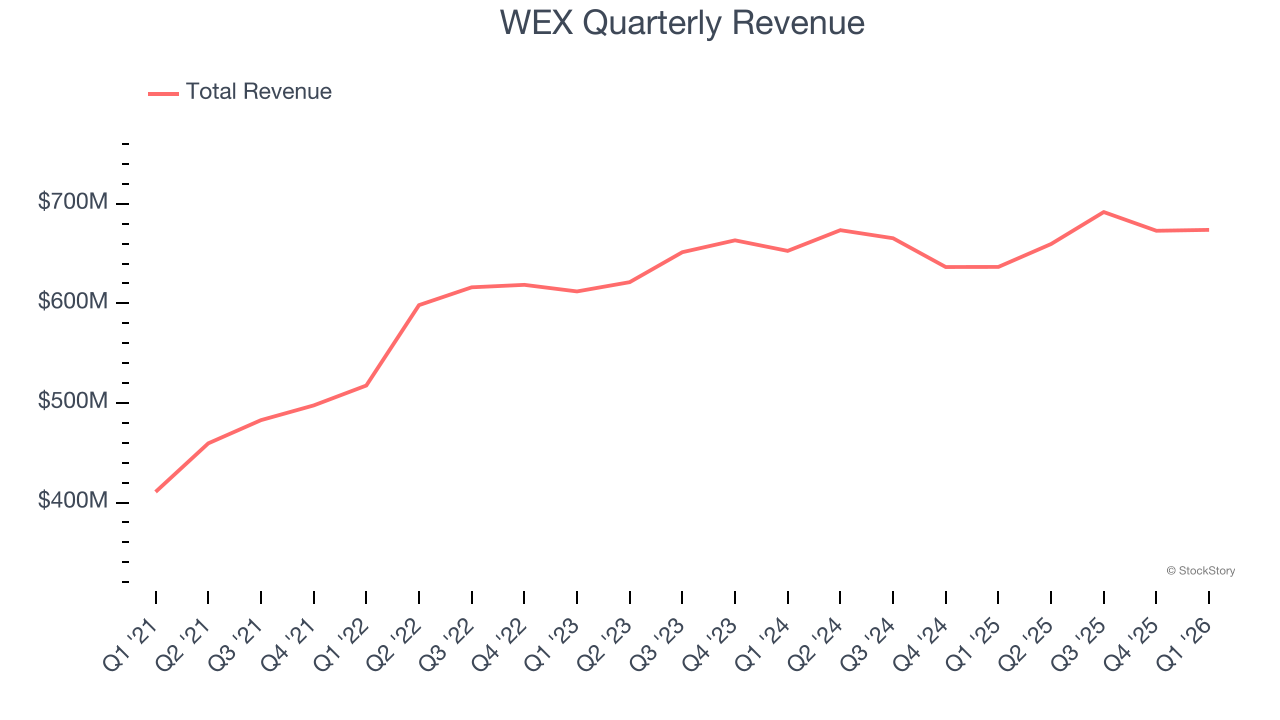

Payment solutions provider WEX (NYSE: WEX) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 5.8% year on year to $673.8 million. The company’s full-year revenue guidance of $2.85 billion at the midpoint came in 1.5% above analysts’ estimates. Its non-GAAP profit of $4.15 per share was 1.4% above analysts’ consensus estimates.

Is now the time to buy WEX? Find out by accessing our full research report, it’s free.

WEX (WEX) Q1 CY2026 Highlights:

- Revenue: $673.8 million vs analyst estimates of $675.5 million (5.8% year-on-year growth, in line although Mobility segment revenue missed)

- Pre-tax Profit: $108.5 million (16.1% margin)

- Adjusted EPS: $4.15 vs analyst estimates of $4.09 (1.4% beat)

- The company lifted its revenue guidance for the full year to $2.85 billion at the midpoint from $2.73 billion, a 4.4% increase

- Management raised its full-year Adjusted EPS guidance to $19.25 at the midpoint, a 9.7% increase

- Market Capitalization: $6.15 billion

“Our momentum continues to build with a strong start to 2026, as revenue and adjusted net income in the first quarter both exceeded the high end of guidance ranges,” said Melissa Smith, WEX’s Chair, Chief Executive Officer, and President.

Company Overview

Originally founded in 1983 as Wright Express to serve the fleet card market, WEX (NYSE: WEX) provides payment processing and business solutions across fleet management, employee benefits, and corporate payments sectors.

Revenue Growth

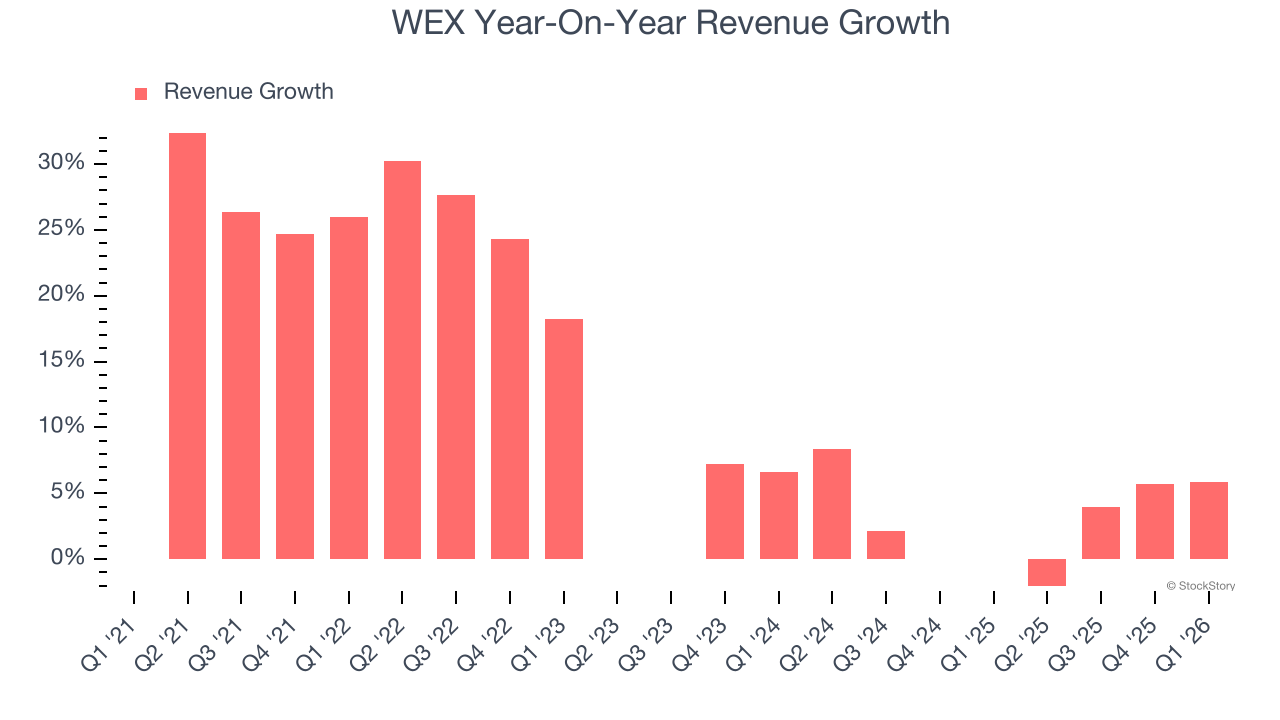

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, WEX’s 11.9% annualized revenue growth over the last five years was solid. Its growth beat the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. WEX’s recent performance shows its demand has slowed as its annualized revenue growth of 2.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, WEX grew its revenue by 5.8% year on year, and its $673.8 million of revenue was in line with Wall Street’s estimates.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Key Takeaways from WEX’s Q1 Results

Revenue was just in line, with Mobility segment revenue missing expectations. On the other hand, it was great to see WEX’s full-year revenue and EPS guidance top analysts’ expectations. Overall, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 2.5% to $180.52 immediately after reporting.

Big picture, is WEX a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).