What a time it’s been for Kodiak Gas Services. In the past six months alone, the company’s stock price has increased by a massive 82.7%, setting a new 52-week high of $64.40 per share. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Kodiak Gas Services, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Kodiak Gas Services Not Exciting?

We’re happy investors have made money, but we don't have much confidence in Kodiak Gas Services. Here are three reasons we avoid KGS and a stock we'd rather own.

1. Fewer Distribution Channels Limit its Ceiling

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program.

Kodiak Gas Services’s $1.31 billion of revenue in the last year is pretty small for the industry, suggesting the company is subscale business in an industry where scale matters.

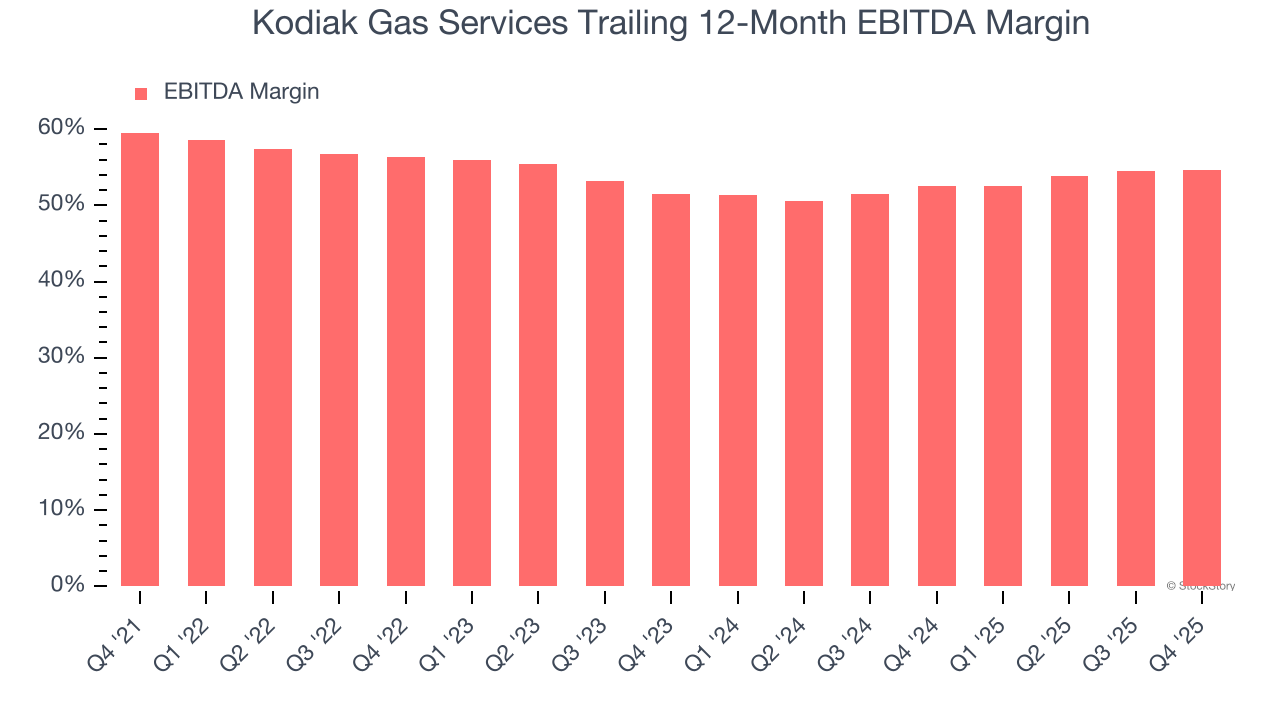

2. Shrinking EBITDA Margin

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Looking at the trend in its profitability, Kodiak Gas Services’s EBITDA margin decreased by 4.9 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Kodiak Gas Services become more profitable in the future. Its EBITDA margin for the trailing 12 months was 54.7%.

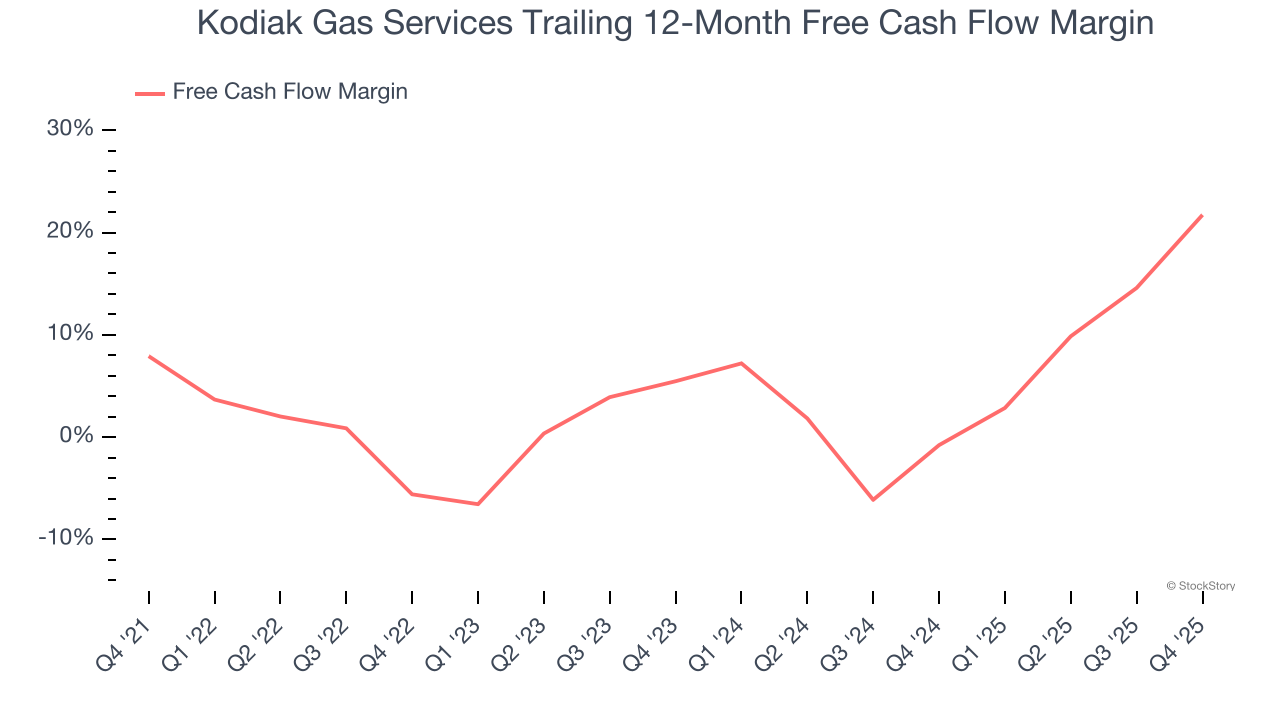

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Kodiak Gas Services has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 7.1%, below what we’d expect for an upstream and integrated energy business.

Final Judgment

Kodiak Gas Services’s business quality ultimately falls short of our standards. Following the recent rally, the stock trades at 23.5× forward P/E (or $64.40 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d recommend looking at the most dominant software business in the world.

Stocks We Like More Than Kodiak Gas Services

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.