Over the past six months, Progressive’s stock price fell to $203.13. Shareholders have lost 7.9% of their capital, which is disappointing considering the S&P 500 has climbed by 4.8%. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Following the drawdown, is this a buying opportunity for PGR? Find out in our full research report, it’s free.

Why Are We Positive On Progressive?

Starting as a small auto insurance company in 1937 with a pioneering focus on high-risk drivers, Progressive (NYSE: PGR) is a major auto, property, and commercial insurance provider that offers policies through independent agents, online platforms, and over the phone.

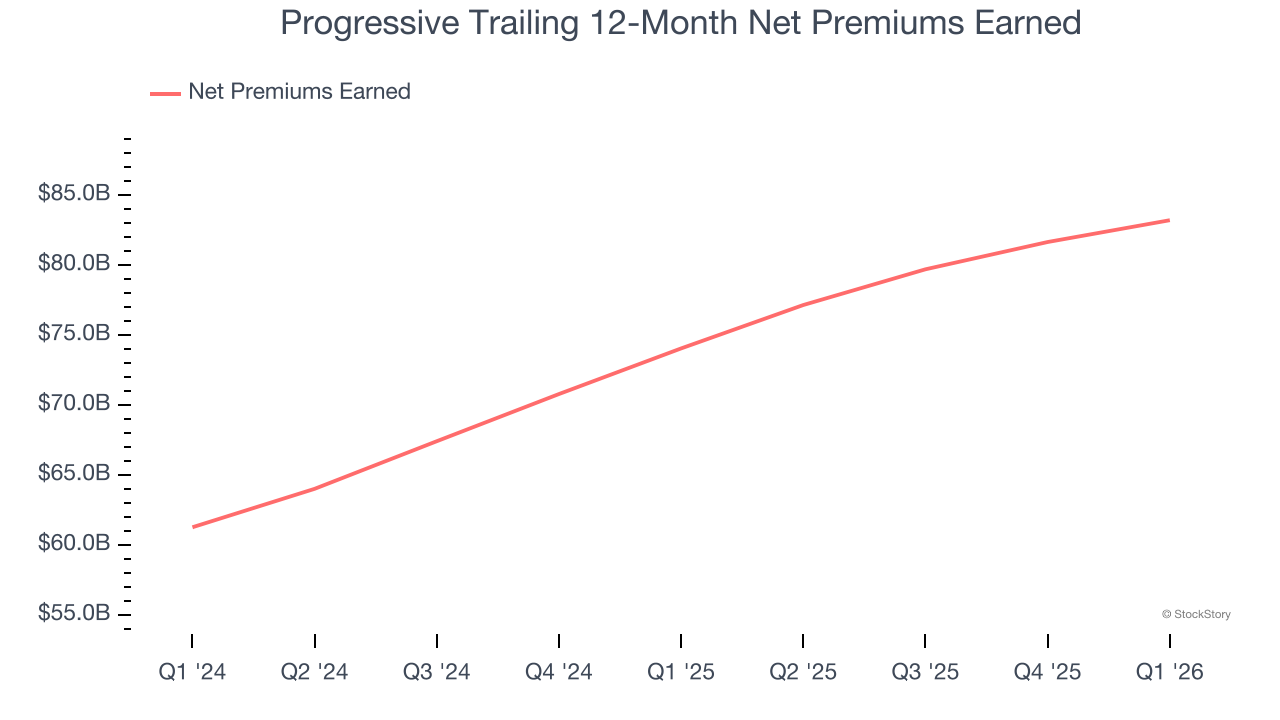

1. Net Premiums Earned Skyrocket, Fueling Growth Opportunities

Insurers sell policies then use reinsurance (insurance for insurance companies) to protect themselves from large losses. Net premiums earned are therefore what's collected from selling policies less what’s paid to reinsurers as a risk mitigation tool.

Progressive’s net premiums earned has grown at a 16.5% annualized rate over the last two years, much better than the broader insurance industry and in line with its total revenue.

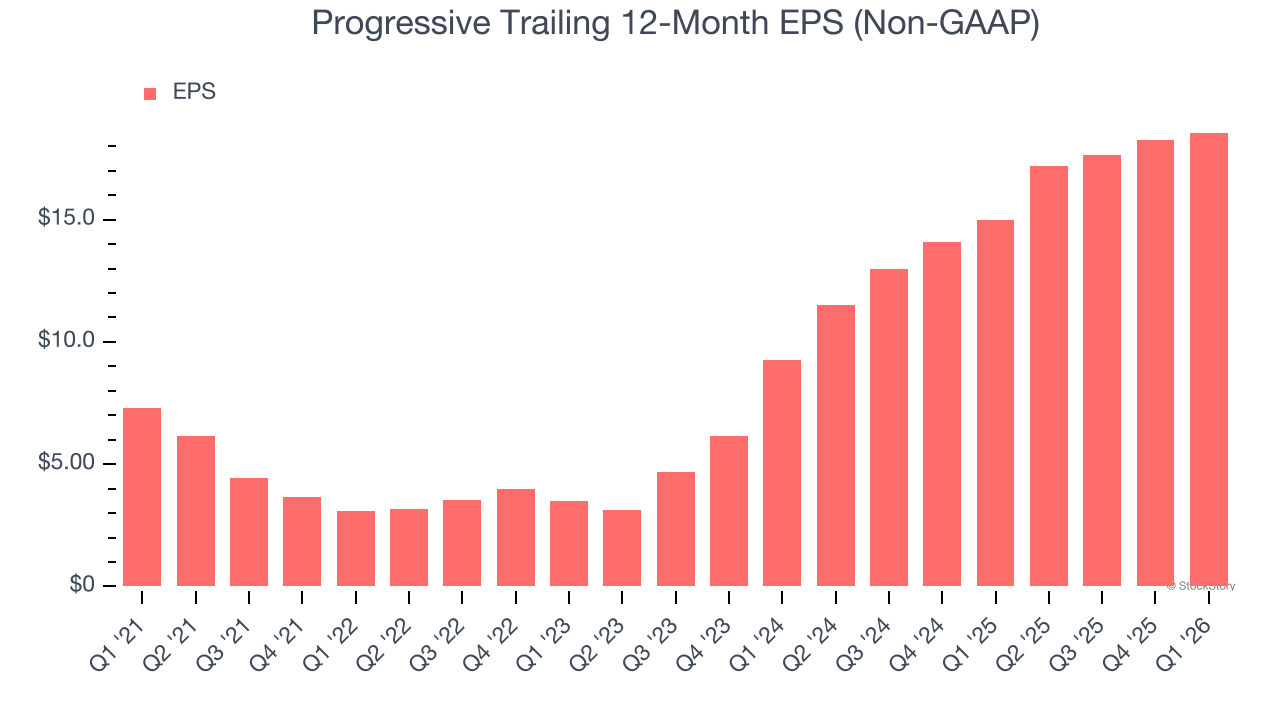

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Progressive’s EPS grew at 20.5% compounded annual growth rate over the last five years, higher than its 14.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

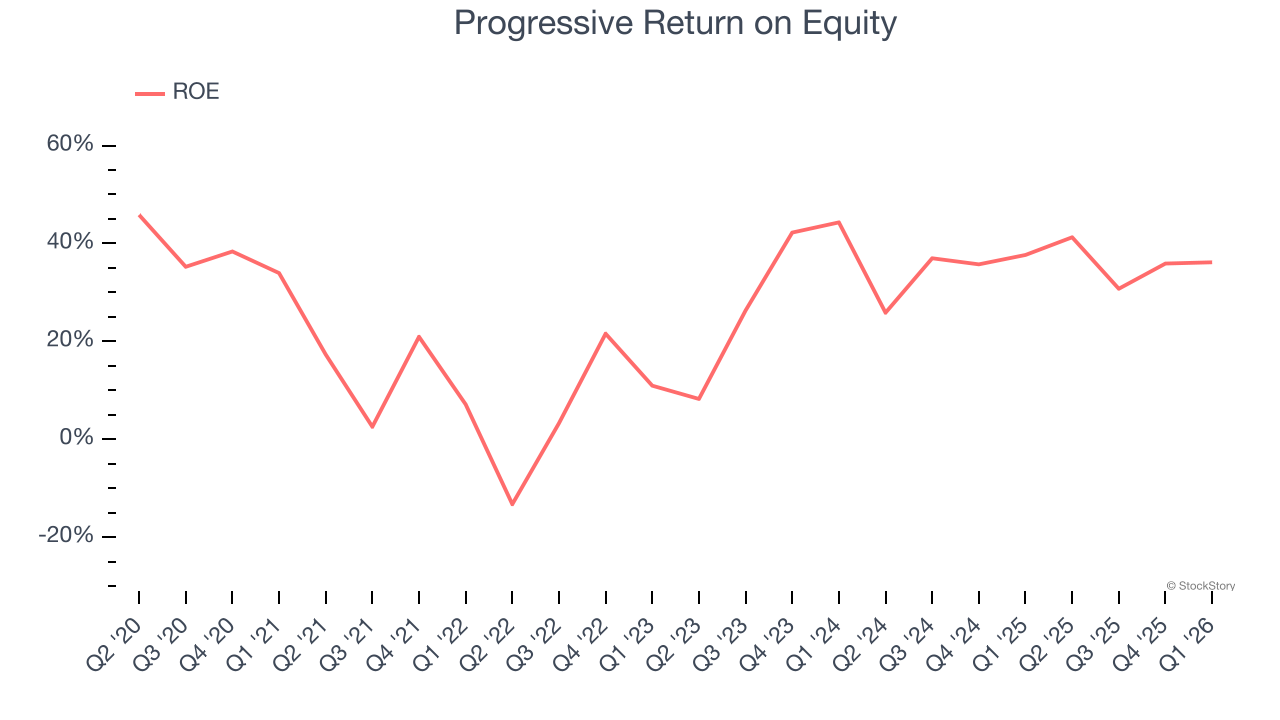

3. Stellar ROE Showcases Lucrative Growth Opportunities

Return on equity (ROE) serves as a comprehensive measure of an insurer's performance, showing how efficiently it converts shareholder capital into profits. Strong ROE performance typically translates to better returns for investors through a combination of earnings retention, share repurchases, and dividend distributions.

Over the last five years, Progressive has averaged an ROE of 23.6%, exceptional for a company operating in a sector where the average shakes out around 12.5% and those putting up 20%+ are greatly admired. This shows Progressive has a strong competitive moat.

Final Judgment

These are just a few reasons why Progressive is a cream-of-the-crop insurance company. With the recent decline, the stock trades at 3.4× forward P/B (or $203.13 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Progressive

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.