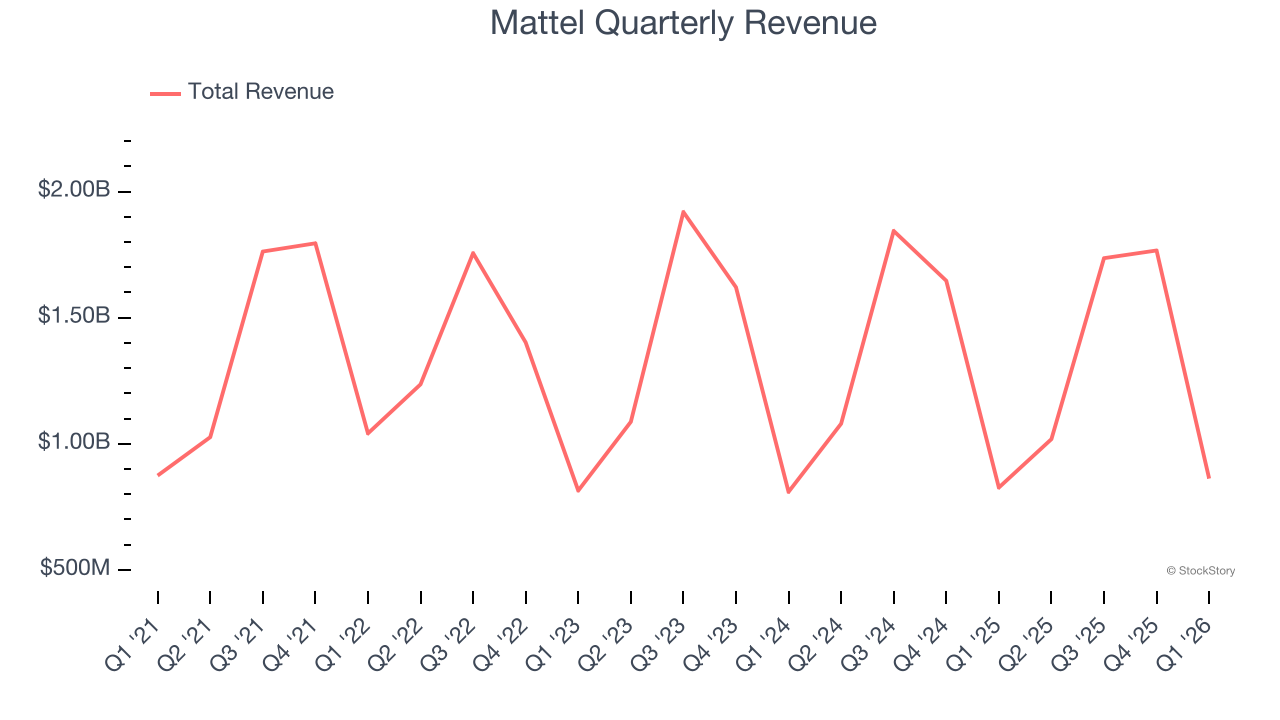

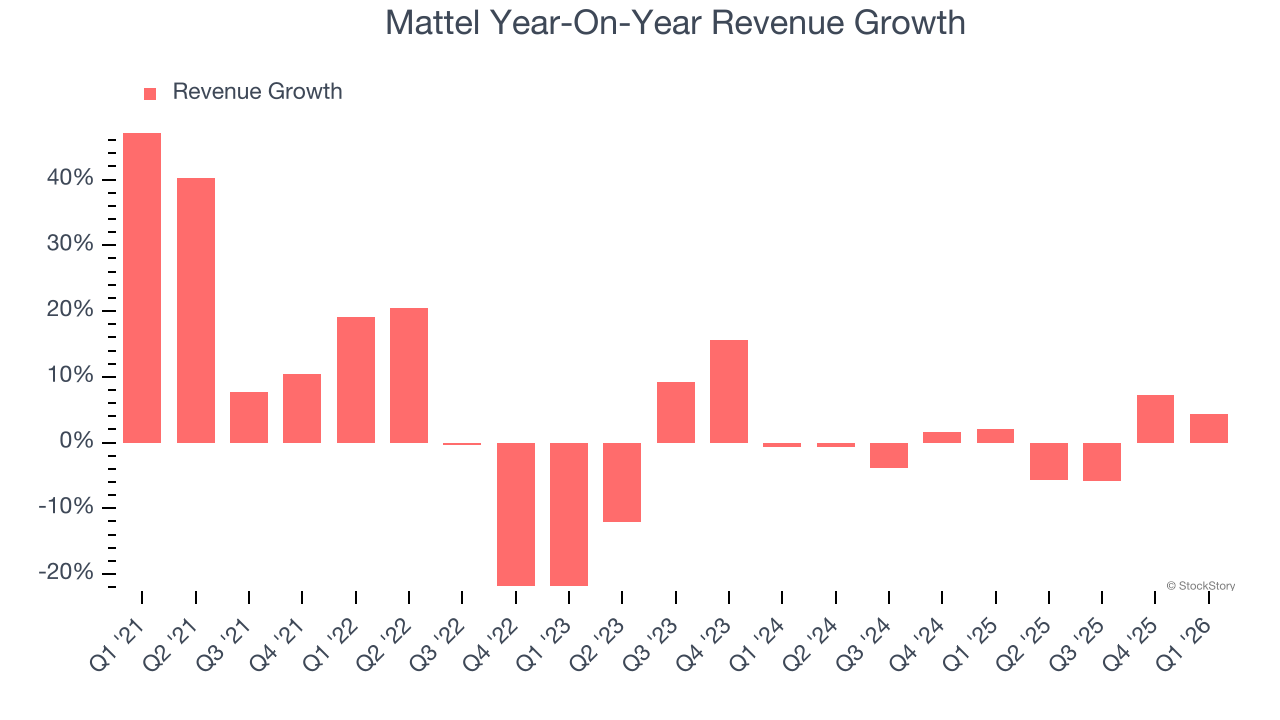

Toy manufacturing and entertainment company (NASDAQ: MAT) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 4.3% year on year to $862.2 million. Its non-GAAP loss of $0.20 per share was in line with analysts’ consensus estimates.

Is now the time to buy Mattel? Find out by accessing our full research report, it’s free.

Mattel (MAT) Q1 CY2026 Highlights:

- Revenue: $862.2 million vs analyst estimates of $809 million (4.3% year-on-year growth, 6.6% beat)

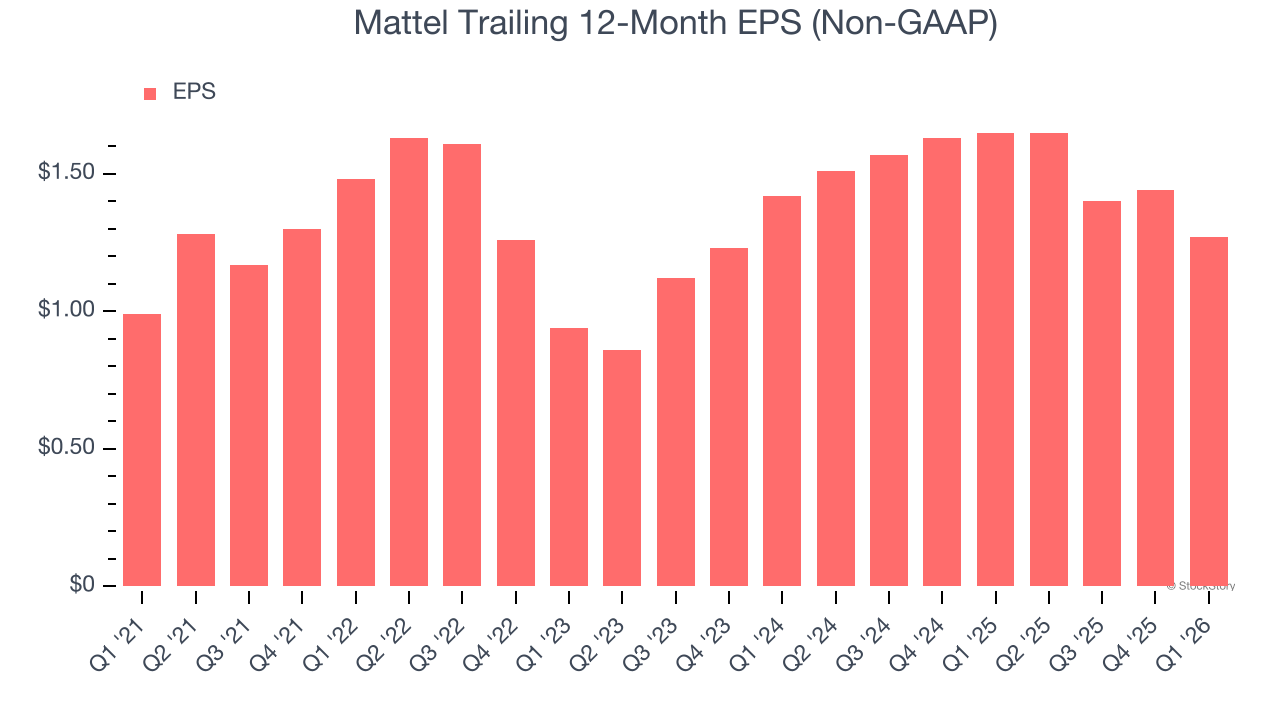

- Adjusted EPS: -$0.20 vs analyst estimates of -$0.21 (in line)

- Management raised its full-year Adjusted EPS guidance to $1.33 at the midpoint, a 7.3% increase

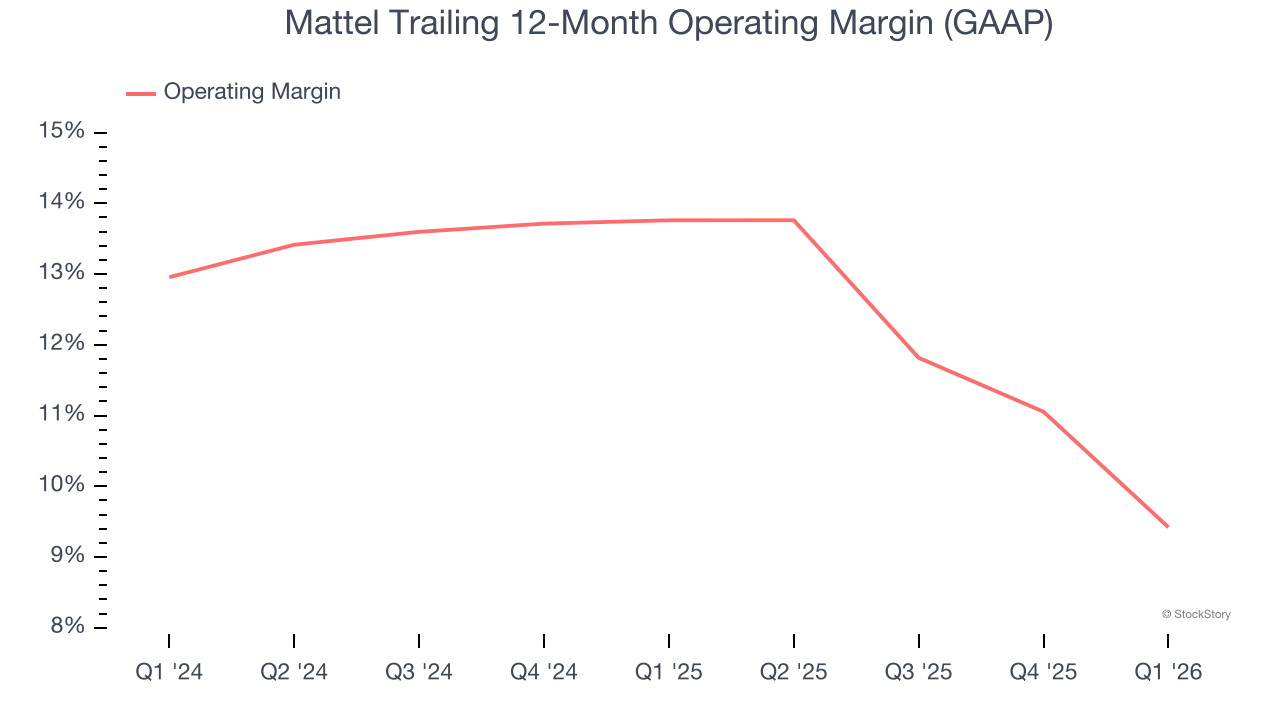

- Operating Margin: -11.9%, down from -2.3% in the same quarter last year

- Free Cash Flow was -$88.1 million compared to -$11.4 million in the same quarter last year

- Market Capitalization: $4.30 billion

Ynon Kreiz, Chairman and CEO of Mattel, said: “We are off to a good start to the year, with Net Sales growth and positive consumer demand for our products in the first quarter. We continued to make progress on our strategy to grow our IP driven play and family entertainment business and are seeing top-line acceleration in the second quarter to date. Our digital strategy is progressing, including the integration of Mattel163 mobile games studio and the upcoming launch of two self-published mobile games, and we look forward to the global theatrical release of the Masters of the Universe movie on June 5th.”

Company Overview

Known for the creation of iconic toys such as Barbie and Hotwheels, Mattel (NASDAQ: MAT) is a global children's entertainment company specializing in the design and production of consumer products.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Mattel’s 2% annualized revenue growth over the last five years was weak. This fell short of our benchmarks and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Mattel’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Mattel reported modest year-on-year revenue growth of 4.3% but beat Wall Street’s estimates by 6.6%.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months. While this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Mattel’s operating margin has shrunk over the last 12 months and averaged 11.6% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q1, Mattel generated an operating margin profit margin of negative 11.9%, down 9.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Mattel’s EPS grew at 5.1% compounded annual growth rate over the last five years. This performance was better than its revenue growth but doesn’t tell us much about its business quality because its operating margin improvement was less than peers.

In Q1, Mattel reported adjusted EPS of negative $0.20, down from negative $0.03 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4.1%. Over the next 12 months, Wall Street expects Mattel’s full-year EPS of $1.27 to stay about the same.

Key Takeaways from Mattel’s Q1 Results

We enjoyed seeing Mattel beat analysts’ revenue expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. Zooming out, we think this was a decent quarter. The stock traded up 1.4% to $15.11 immediately after reporting.

Should you buy the stock or not? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).