Over the last six months, Dillard’s shares have sunk to $563.25, producing a disappointing 7.5% loss - a stark contrast to the S&P 500’s 7.1% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Dillard's, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Dillard's Not Exciting?

Even though the stock has become cheaper, we're cautious about Dillard's. Here are three reasons why DDS doesn't excite us and a stock we'd rather own.

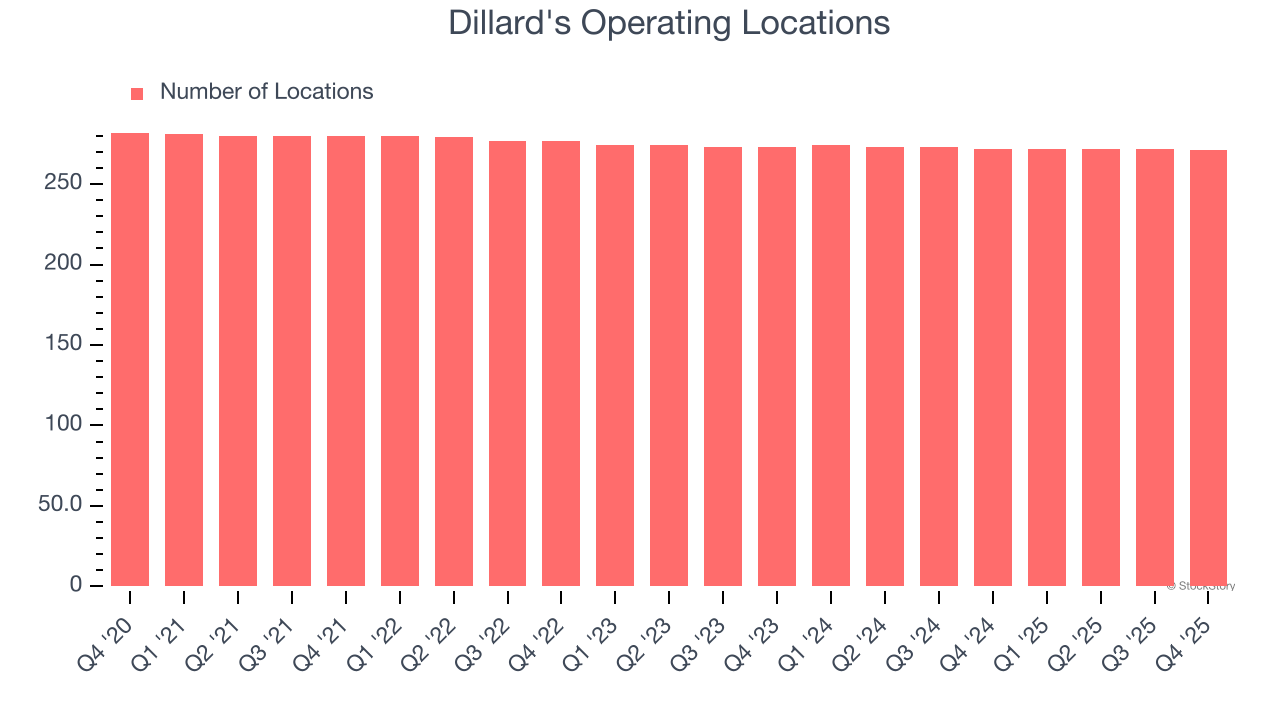

1. Lack of New Stores, a Headwind for Revenue

A retailer’s store count often determines how much revenue it can generate.

Dillard's listed 271 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

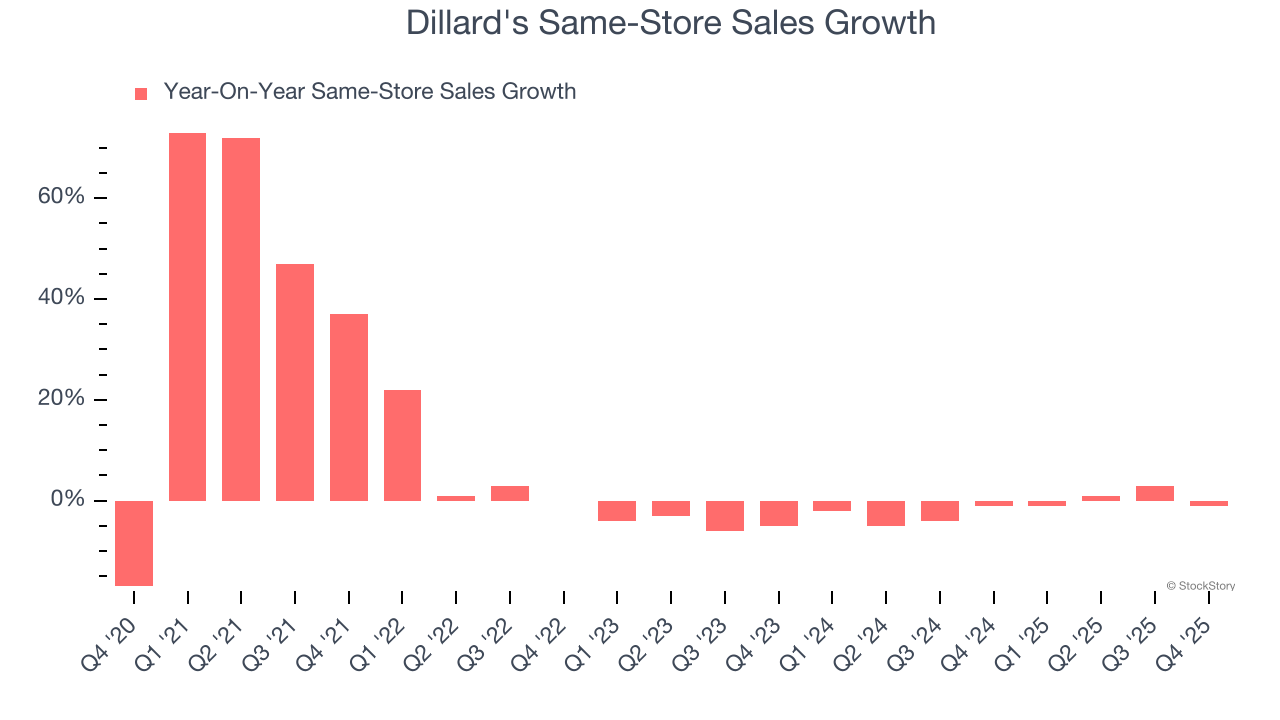

2. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Dillard’s demand has been shrinking over the last two years as its same-store sales have averaged 1.3% annual declines.

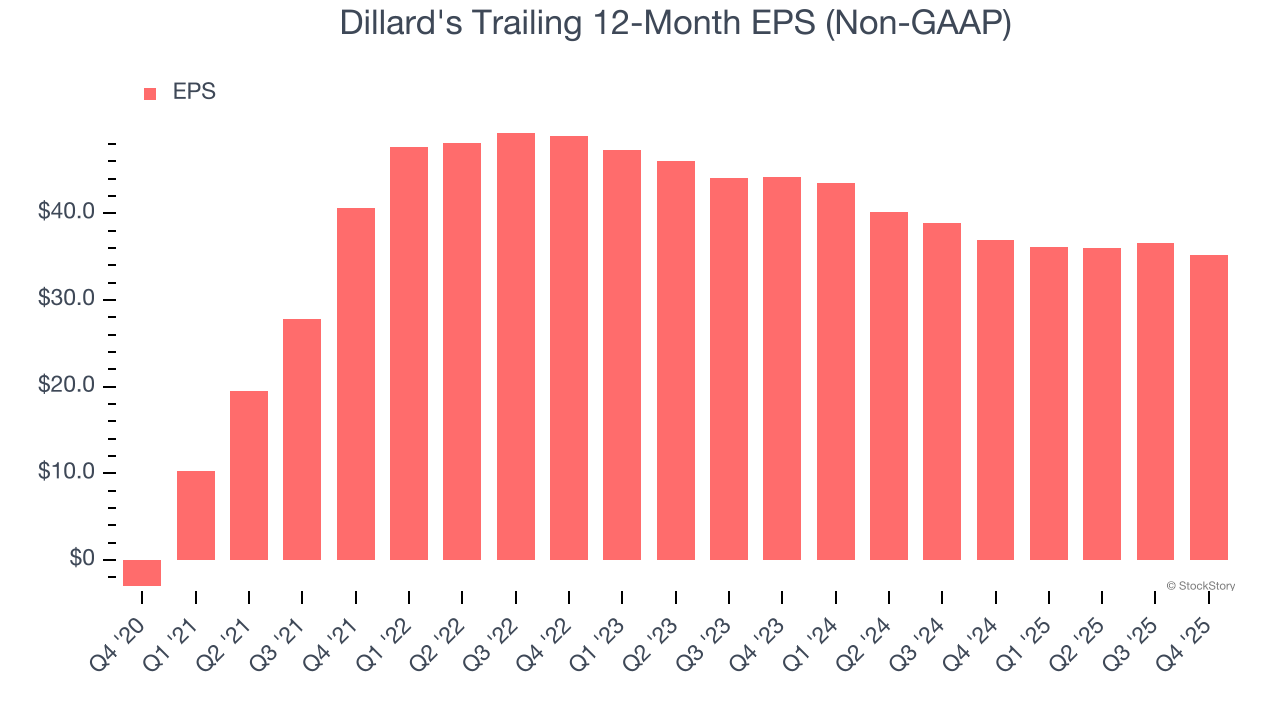

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Dillard's, its EPS declined by 10.4% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

Dillard’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 17.3× forward P/E (or $563.25 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of Dillard's

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.