Over the past six months, Zeta Global’s stock price fell to $17.03. Shareholders have lost 14% of their capital, which is disappointing considering the S&P 500 has climbed by 7.1%. This might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for ZETA? Find out in our full research report, it’s free.

Why Does Zeta Global Spark Debate?

Powered by an AI engine that processes over one trillion consumer signals monthly, Zeta Global (NYSE: ZETA) operates a data-driven cloud platform that helps companies target, connect, and engage with consumers through personalized marketing across channels like email, social media, and video.

Two Things to Like:

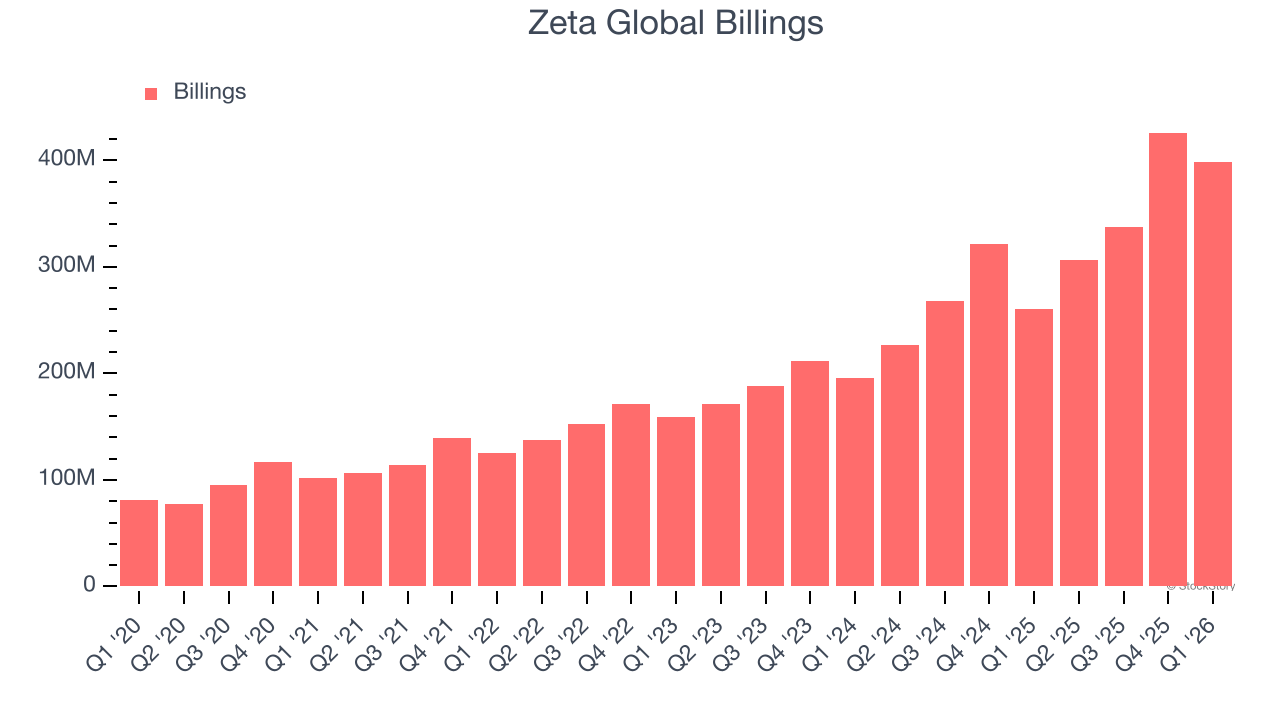

1. Billings Surge, Boosting Cash On Hand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Zeta Global’s billings punched in at $398.3 million in Q1, and over the last four quarters, its year-on-year growth averaged 36.6%. This performance was fantastic, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

2. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Zeta Global’s revenue to rise by 28.8%. While this projection is below its 36.9% annualized growth rate for the past two years, it is eye-popping and suggests the market is forecasting success for its products and services.

One Reason to be Careful:

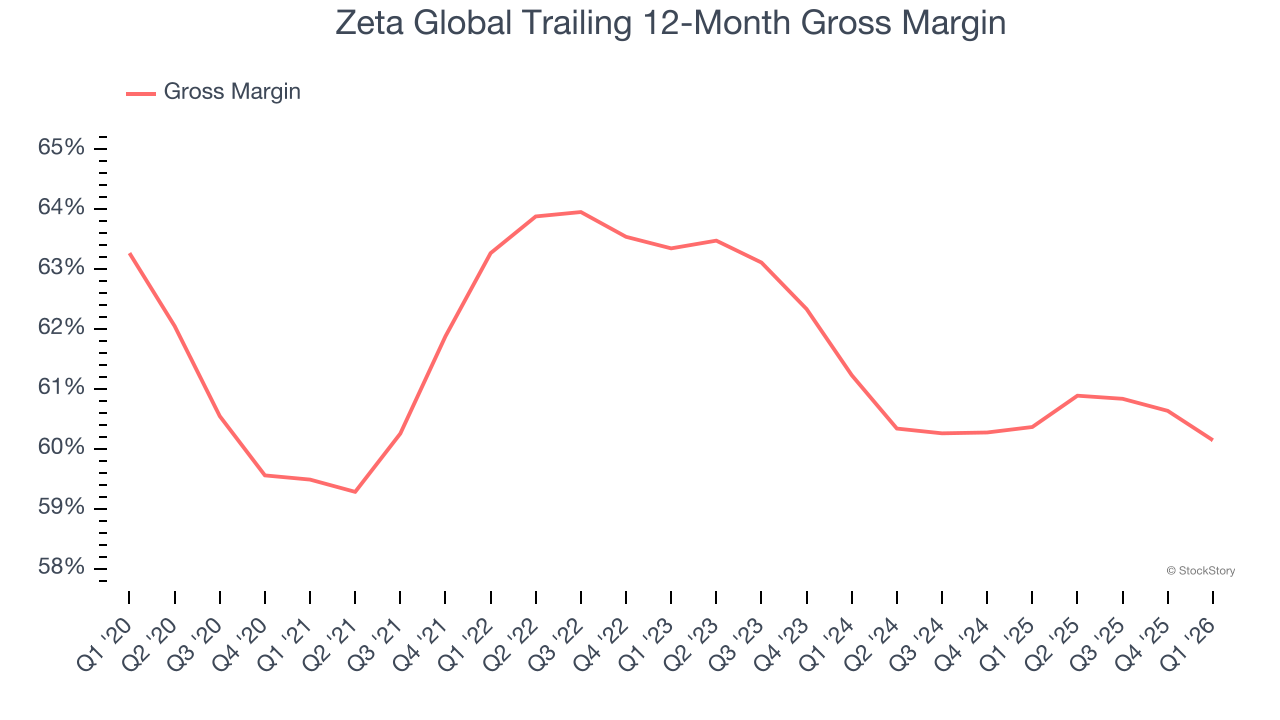

Low Gross Margin Reveals Weak Structural Profitability

For software companies like Zeta Global, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Zeta Global’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 60.1% gross margin over the last year. Said differently, Zeta Global had to pay a chunky $39.86 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Zeta Global has seen gross margins decline by 1.1 percentage points over the last 2 year, which is poor compared to software peers.

Final Judgment

Zeta Global has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 2.2× forward price-to-sales (or $17.03 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.