Personal computing and printing company HP (NYSE: HPQ) announced better-than-expected revenue in Q1 CY2026, with sales up 9% year on year to $14.41 billion. Its non-GAAP profit of $0.86 per share was 20.3% above analysts’ consensus estimates.

Is now the time to buy HP? Find out by accessing our full research report, it’s free.

HP (HPQ) Q1 CY2026 Highlights:

- Revenue: $14.41 billion vs analyst estimates of $13.91 billion (9% year-on-year growth, 3.6% beat)

- Adjusted EPS: $0.86 vs analyst estimates of $0.72 (20.3% beat)

- Adjusted EBITDA: $988 million vs analyst estimates of $1.12 billion (6.9% margin, 11.7% miss)

- Management lowered its full-year Adjusted EPS guidance to $3 at the midpoint, a 1.6% decrease

- Operating Margin: 4.2%, in line with the same quarter last year

- Free Cash Flow was $756 million, up from -$145 million in the same quarter last year

- Market Capitalization: $22.34 billion

"During the second quarter, we continued executing our future of work strategy through intelligent devices, edge AI, and connected experiences while navigating rising commodity costs,” said Bruce Broussard, Interim CEO, HP Inc.

Company Overview

Born from the legendary Silicon Valley garage startup founded by Bill Hewlett and Dave Packard in 1939, HP (NYSE: HPQ) designs and sells personal computers, printers, and related technology products and services to consumers, businesses, and enterprises worldwide.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $57.42 billion in revenue over the past 12 months, HP is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. To accelerate sales, HP likely needs to optimize its pricing or lean into new offerings and international expansion.

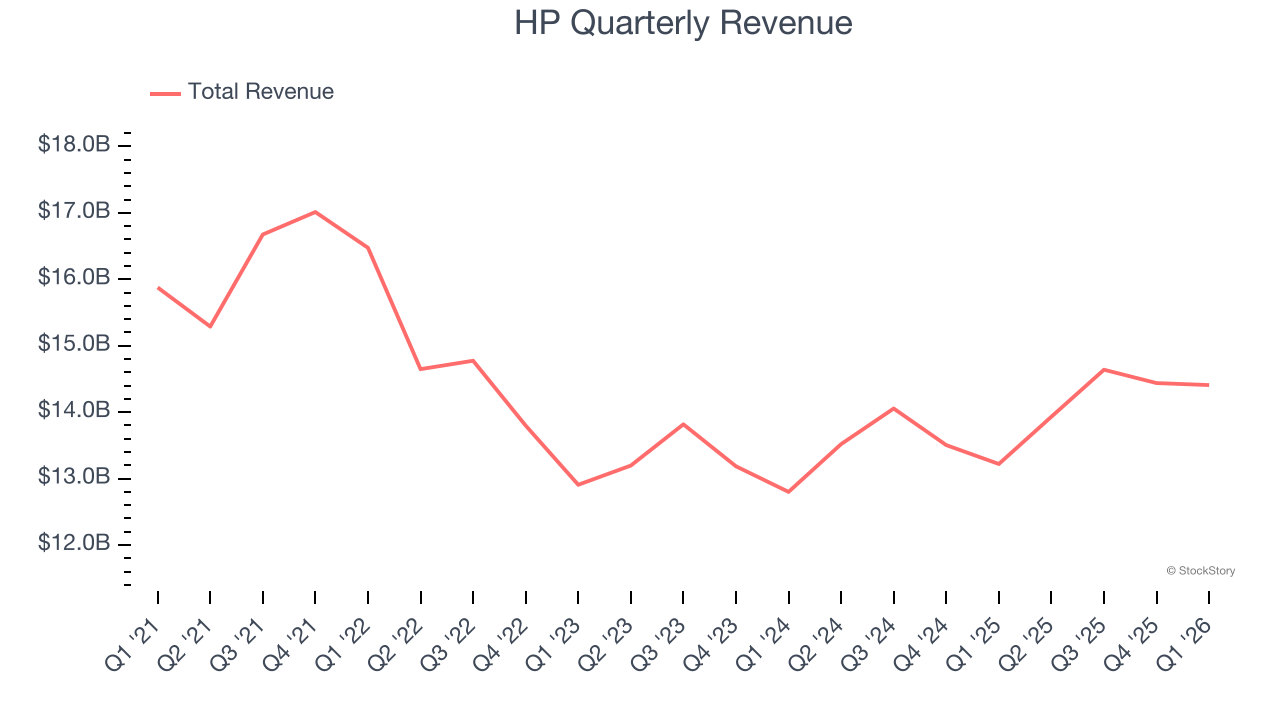

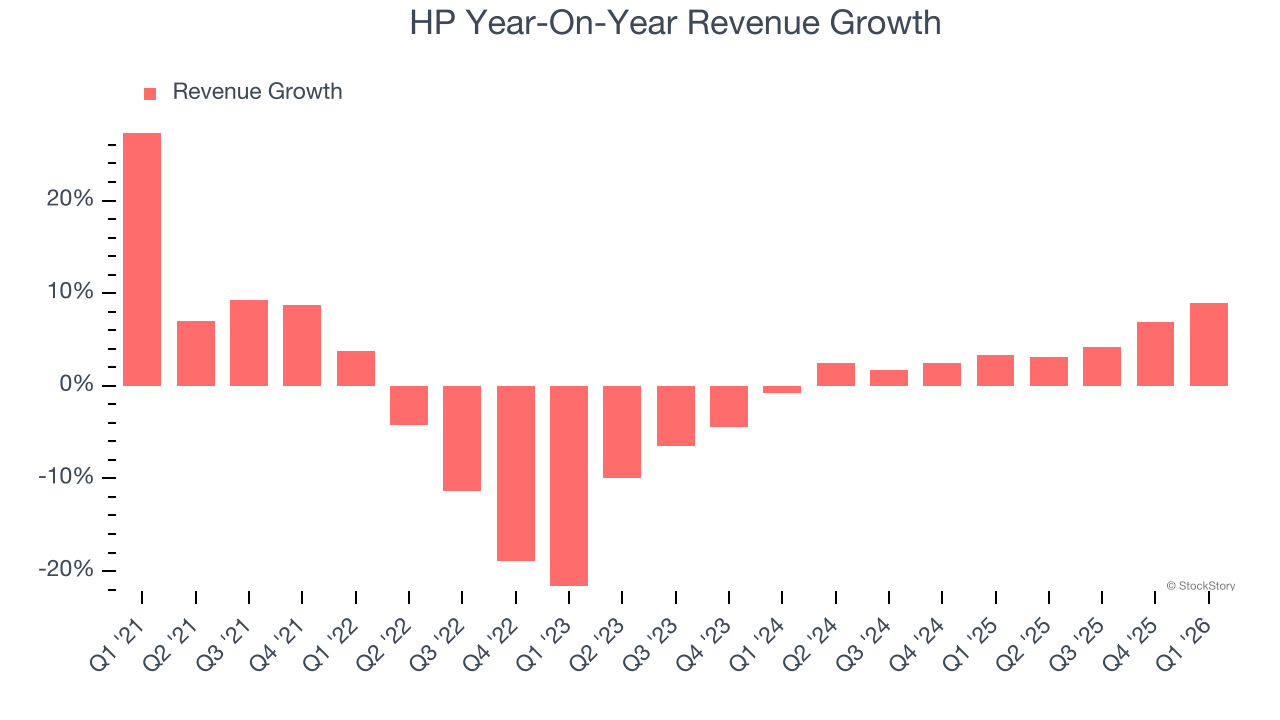

As you can see below, HP’s revenue declined by 1.2% per year over the last five years, a rough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. HP’s annualized revenue growth of 4.1% over the last two years is above its five-year trend, which is encouraging.

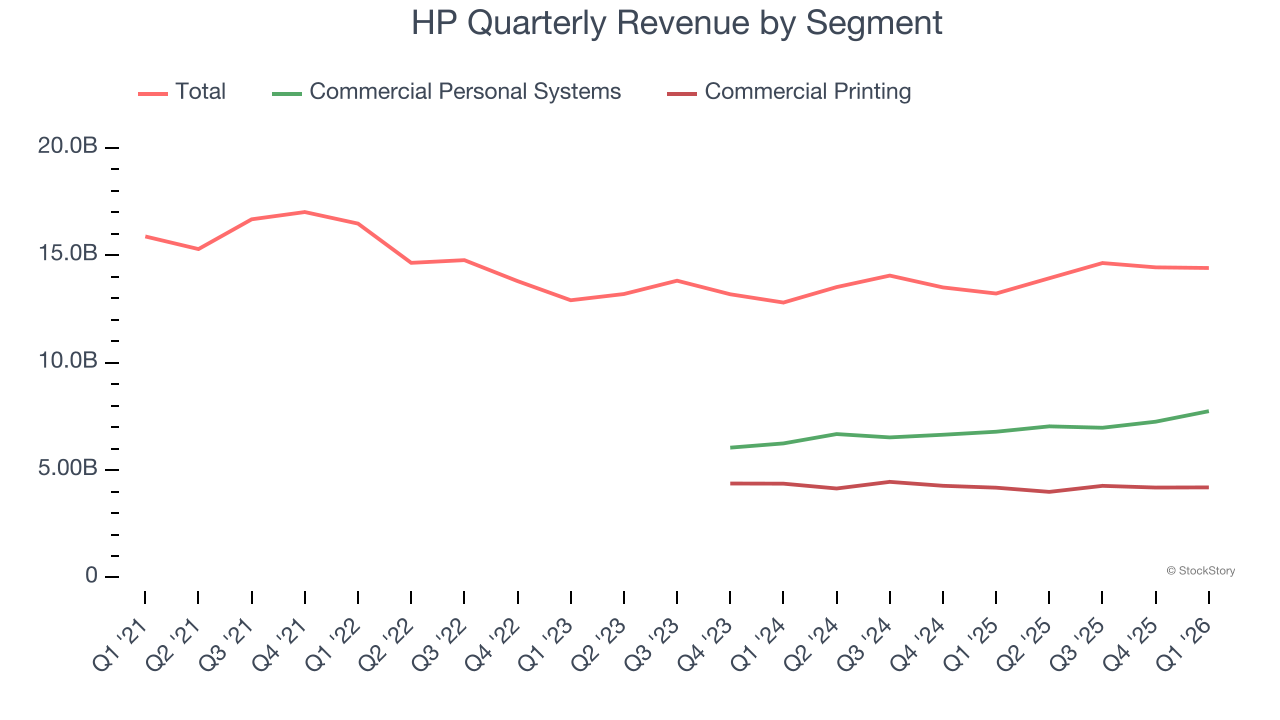

We can better understand the company’s revenue dynamics by analyzing its most important segments, Commercial Personal Systems and Commercial Printing, which are 53.7% and 29.1% of revenue. Over the last two years, HP’s Commercial Personal Systems revenue (desktops, laptops, etc.) averaged 9% year-on-year growth. On the other hand, its Commercial Printing revenue (commercial or industrial printers) averaged 2.7% declines.

This quarter, HP reported year-on-year revenue growth of 9%, and its $14.41 billion of revenue exceeded Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to decline by 2.4% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

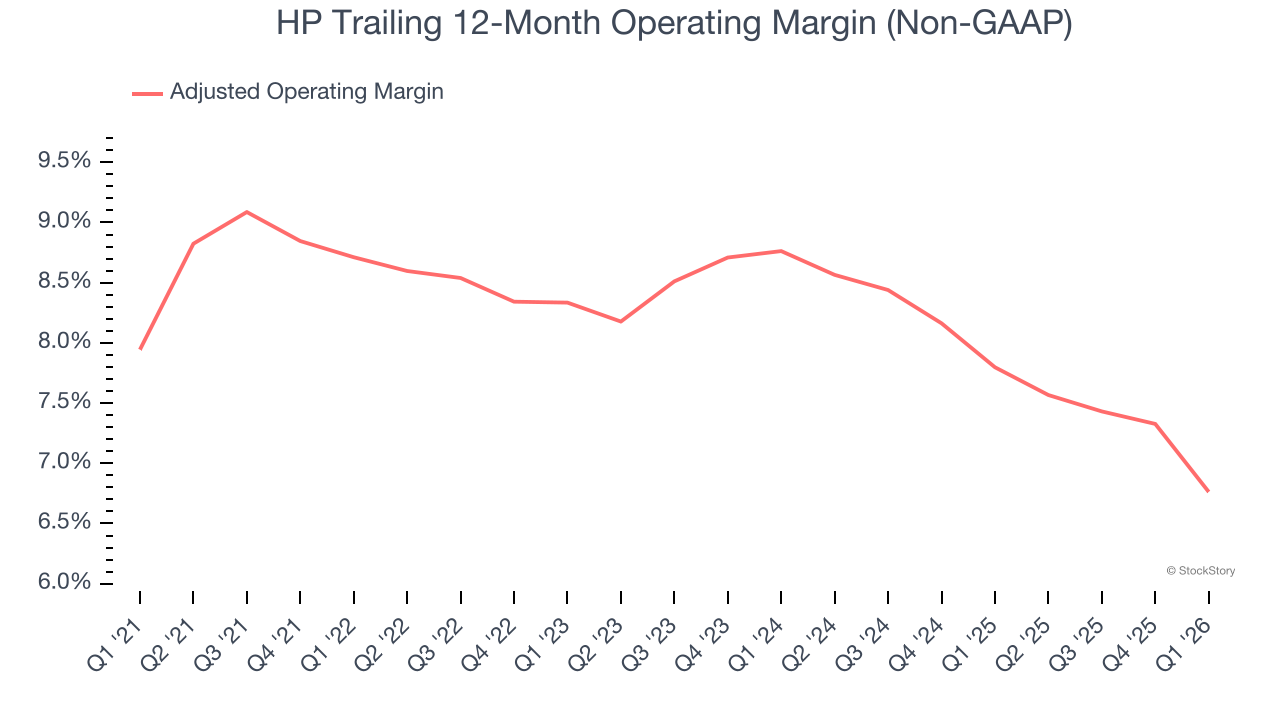

Adjusted Operating Margin

HP was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 8.1% was weak for a business services business.

Analyzing the trend in its profitability, HP’s adjusted operating margin decreased by 1.9 percentage points over the last five years. HP’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q1, HP generated an adjusted operating margin profit margin of 5%, down 2.2 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

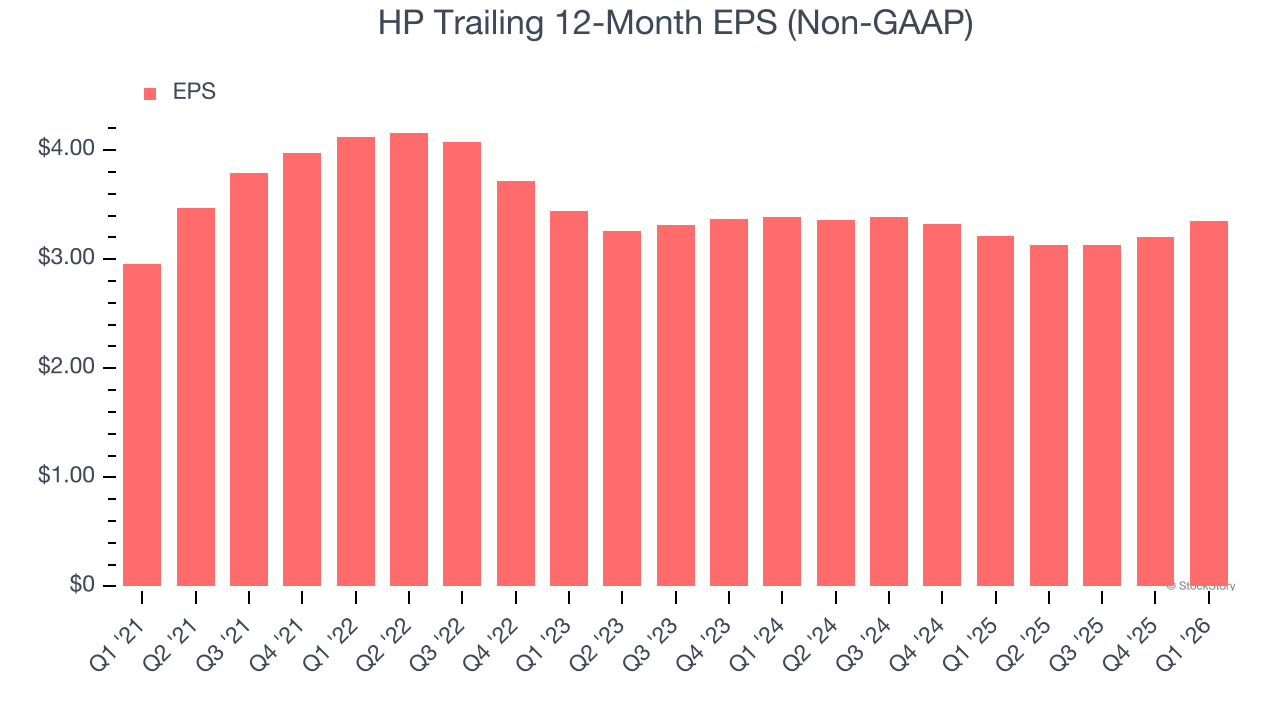

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

HP’s EPS grew at 2.5% compounded annual growth rate over the last five years. This performance was better than its 1.2% annualized revenue declines but doesn’t tell us much about its business quality because its adjusted operating margin didn’t improve.

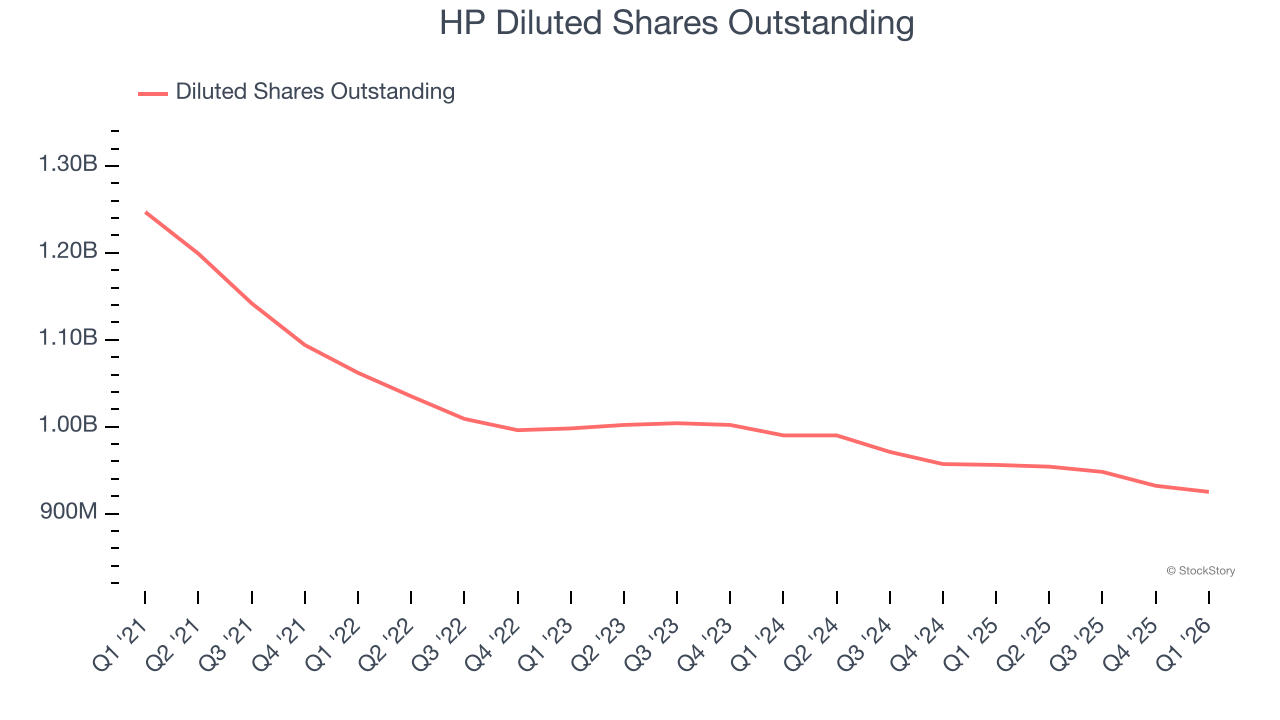

Diving into the nuances of HP’s earnings can give us a better understanding of its performance. A five-year view shows that HP has repurchased its stock, shrinking its share count by 25.8%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For HP, EPS didn’t budge over the last two years, a regression from its five-year trend. We hope it can revert to earnings growth in the coming years.

In Q1, HP reported adjusted EPS of $0.86, up from $0.71 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects HP’s full-year EPS to shrink by 19.2% from $3.35 to $2.71.

Key Takeaways from HP’s Q1 Results

It was good to see HP beat analysts’ EPS expectations this quarter. We were also glad its EPS guidance for next quarter outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 3.8% to $26.54 immediately after reporting.

Sure, HP had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).